Chuckanut

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

The current situation with LTC is not acceptable to many of us including me. Premiums are high and may go higher, benefits are more limited, and then there is always the chance the existing health problems may make getting LTC insurance problematic.

We are not poor enough that government programs would step in and pay the costs from the beginning, but we are not rich enough to be able to afford more than a year or two of LTC expenses before it greatly affects the rest of our financial situation.

I am looking for ideas on substitutes for LTC insurance plans.

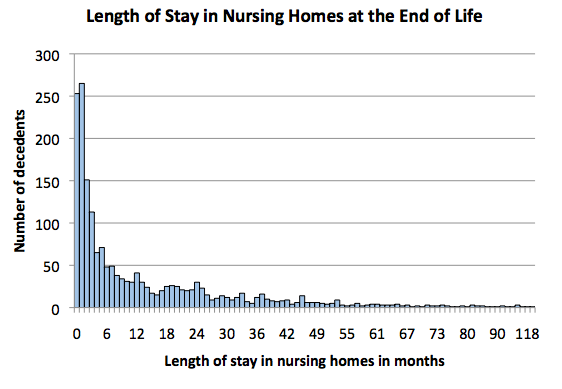

I have read articles recommending buying an ordinary (not the hybrids that include LTC insurance) single premium deferred annuity that starts at 75. (The average age of admittance to LTC is about 79 so there is a four year fudge factor in case one is below average.)

I imagine I have not anticipated various pitfalls in the above plan. The biggest I see is that at today's interest rates a few hundred grand does not buy a lot of income, even 10 years from now.

Any other ideas for reasonable substitutes for LTC insurance in today's market?

We are not poor enough that government programs would step in and pay the costs from the beginning, but we are not rich enough to be able to afford more than a year or two of LTC expenses before it greatly affects the rest of our financial situation.

I am looking for ideas on substitutes for LTC insurance plans.

I have read articles recommending buying an ordinary (not the hybrids that include LTC insurance) single premium deferred annuity that starts at 75. (The average age of admittance to LTC is about 79 so there is a four year fudge factor in case one is below average.)

I imagine I have not anticipated various pitfalls in the above plan. The biggest I see is that at today's interest rates a few hundred grand does not buy a lot of income, even 10 years from now.

Any other ideas for reasonable substitutes for LTC insurance in today's market?

Last edited: