RetireeRobert

Thinks s/he gets paid by the post

Yes, a downturn is coming soon. Fed will get its hands off the stuck interest rates and will let them (maybe nudge them) to rise.

When most of the people on this forum believe that stocks will go up in the long run, why do they have bonds in the portfolio. Wouldn’t it make sense to have cash for emergency purposes and invest everything else in stocks for the long ride?

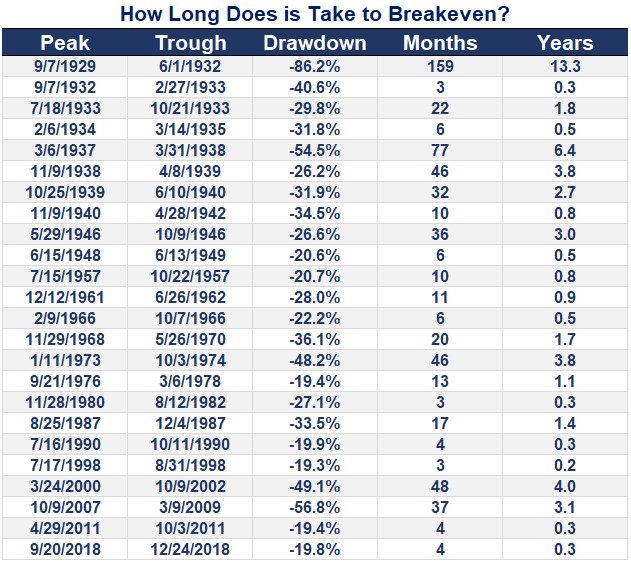

Personal finance is personal. If you live through a few periods where your portfolio balance drops 30-50%, evaporating all those little spending plans you fantasized about, and while the financial press hits the panic button daily to sell breathless articles about all the reasons stock prices are never coming back, well, unless you are an emotion-free Dr. Spock, you may come to appreciate owning some bonds. In those times, the Fed has cut interest rates and bond prices are rising, making it comforting to own some bonds.

...

When most of the people on this forum believe that stocks will go up in the long run, why do they have bonds in the portfolio. Wouldn’t it make sense to have cash for emergency purposes and invest everything else in stocks for the long ride?

When most of the people on this forum believe that stocks will go up in the long run, why do they have bonds in the portfolio. Wouldn’t it make sense to have cash for emergency purposes and invest everything else in stocks for the long ride?

Well said.

My personal opinion (shared by many pretty good investors) is that we are in a different rate climate after 40 years of rate declines. So one should not expect the boost to the portfolio like in the past 40 years from bonds should we get an extended market decline (recession induced). Still bonds might hold up better then stocks in a recession although the 1970's saw bonds and stocks doing poorly. So I hold bonds but shorter duration and some inflation protected too with decent real rates.

I agree about 40 year bond rate declines. Heck, there’s a book out saying we’re at 3,000 year interest rate lows or something. I guess the way I mentally address it is three-fold:

1) We are also in an historically-low inflationary period, so bonds and other investments don’t have to work as hard to create real returns.

As of August we have 12 month inflation running around 4.9%. Who knows if that will continue. The Fed says it will not.

2) Should inflation spike for longer than an ephemeral period, I trust the Fed will raise rates to cool things down. My bond index fund will eventually reflect those higher rate bonds. The average bond duration in my Vanguard index fund is about 8 years, so the lower yielding ones will be cleaned out in due time, to be replaced by….whatever bond rates the markets and Fed provide over those subsequent 8 years.

Probably such higher duration bonds will do OK over the long term. I don't have confidence over the next year or two. But that is me.

3) Our bond portfolio is 1/3 international bond index, so that all of our eggs aren’t subject to domestic markets alone. I know that is controversial among many here, but a) I sleep better with less home country bias, and 2) It’s approximately the allocation that Vanguard gives its target date and Life Strategy funds, so critics would have to persuade me how they are smarter than Vanguard. So far, none have.

I'm not trying to be smarter then VG but I'm just not comfortable with international bonds. It seems that whenever there is a flight to quality it tends to favor US Treasuries.

Including food and energy, officials expect inflation to run at 4.2% this year, up from 3.4% in June. The subsequent two years are expected to fall back to 2.2%, little changed from the June outlook.