You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Locked in some gains

- Thread starter RobbieB

- Start date

LRDave

Thinks s/he gets paid by the post

You're my spirit animal.... ")

NW-Bound

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Jul 3, 2008

- Messages

- 35,712

Rebalancing from large-cap stocks to Wagyu beef and caviar, I see...

I still keep mine in cash.

I still keep mine in cash.

Last summer, I reallocate my 60/40 IRA portfolio to 100% treasuries when the Dow was about 27,500. There was a lot of recession talk during that time so I became conservative since I am close to age 70. However, when the Dow passed 28,000, I re-allocated my portfolio to 50% treasuries and 50% to VWENX which is a balance fund.

Half of my portfolio of treasuries assumes a crash is coming. The other half assumes the Dow will continue to climb. I intend to stay in this position but I am ready to exchange my VWENX into treasuries if there are more signs of a recession.

I am with Vanguard and the exchange time from VWENX to Treasuries is 2 business days. I may see a loss during those 2 days but not as much as people who decide to ride it out. My worst fear is a crash similar to the Nikkei stock market crash when the Nikkei was 26,582 on April 1991. After 29 years, Japan has yet to recover. Please note that 29+ years is a long time for a buy and hold investor to ride out.

Half of my portfolio of treasuries assumes a crash is coming. The other half assumes the Dow will continue to climb. I intend to stay in this position but I am ready to exchange my VWENX into treasuries if there are more signs of a recession.

I am with Vanguard and the exchange time from VWENX to Treasuries is 2 business days. I may see a loss during those 2 days but not as much as people who decide to ride it out. My worst fear is a crash similar to the Nikkei stock market crash when the Nikkei was 26,582 on April 1991. After 29 years, Japan has yet to recover. Please note that 29+ years is a long time for a buy and hold investor to ride out.

Does anyone know anyone who was fully vested only in the Japanese market at 100% equities for the last 29 years?

The were probably a bunch of Japanese Investors who got burned...but not US Investors.

You missed the point. What happened in Japan "may" happen in the USA. If you believe that situation will NEVER EVER happen in the US stock market, then let me cut and paste for you the causes of the Japanese crash from wikipedia:

The Japanese asset price bubble (バブル景気, baburu keiki, "bubble economy") was an economic bubble in Japan from 1986 to 1991 in which real estate and stock market prices were greatly inflated.[1] In early 1992, this price bubble burst and Japan's economy stagnated. The bubble was characterized by rapid acceleration of asset prices and overheated economic activity, as well as an uncontrolled money supply and credit expansion.[2] More specifically, over-confidence and speculation regarding asset and stock prices were closely associated with excessive monetary easing policy at the time.[3]

By August 1990, the Nikkei stock index had plummeted to half its peak by the time of the fifth monetary tightening by the Bank of Japan (BOJ).[2] By late 1991, asset prices began to fall. Even though asset prices had visibly collapsed by early 1992,[2] the economy's decline continued for more than a decade. This decline resulted in a huge accumulation of non-performing assets loans (NPL), causing difficulties for many financial institutions. The bursting of the Japanese asset price bubble contributed to what many call the Lost Decade.[4] Japan's annual land prices averaged nationwide have finally risen since the asset bubble collapse, though only mildly at 0.1%, a process that has taken 26 years to show up statistically.

Based on the current US Market: Are we in a stock market bubble? Are we in a real estate bubble? Do we have uncontrolled money supply and credit? Do we have excessive monetary easing?

IMO...You do not want the stock market and the real estate market to expand too rapidly or have excessive monetary easing because this creates a classic economic bubble. The Fed is conducting excessive monetary easing to avoid the recession but there may be unintended consequences.

copyright1997reloaded

Thinks s/he gets paid by the post

Last summer, I reallocate my 60/40 IRA portfolio to 100% treasuries when the Dow was about 27,500. There was a lot of recession talk during that time so I became conservative since I am close to age 70. However, when the Dow passed 28,000, I re-allocated my portfolio to 50% treasuries and 50% to VWENX which is a balance fund.

Half of my portfolio of treasuries assumes a crash is coming. The other half assumes the Dow will continue to climb. I intend to stay in this position but I am ready to exchange my VWENX into treasuries if there are more signs of a recession.

I am with Vanguard and the exchange time from VWENX to Treasuries is 2 business days. I may see a loss during those 2 days but not as much as people who decide to ride it out. My worst fear is a crash similar to the Nikkei stock market crash when the Nikkei was 26,582 on April 1991. After 29 years, Japan has yet to recover. Please note that 29+ years is a long time for a buy and hold investor to ride out.

So last summer you were saying we had peaked. Ton's of posts in http://www.early-retirement.org/forums/f44/going-all-cash-in-401k-98649.html about things like the National Debt "IMO the bear market is coming because of the national debt". It doesn't seem like the debt problem has been solved, yet the market moved higher...and higher.

I really don't get the need to do drastic 50% changes. I guess people do it in their tax-deferred accounts because they can without any tax consequences...but what makes one think they can guess THE time and place of the peak.

There's nothing wrong with taking profits, to lock in a gain for funds that are needed for a specific purpose or to reduce equity exposure when the allocation gets out of whack. Heck, I did some of that at the end of the year and might do more as my equity % has been creeping up. I just don't think massive moves on %'s is (in the long run) a prudent way to invest. (But to each their own...each of us has the responsibility to manage our money.)

street

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Nov 30, 2016

- Messages

- 9,535

LOLRebalancing from large-cap stocks to Wagyu beef and caviar, I see...

I still keep mine in cash.

RobbieB good for you. I pulled some out of a CD that matured and will spend it on some things coming up.

Onward

Thinks s/he gets paid by the post

- Joined

- Jul 1, 2009

- Messages

- 1,934

I locked in a bunch of stock gains in 1992, when the Dow was 6,000. Since then I've wanted to re-invest, but I know a crash could come at any time. Whew! Guess I dodged that bullet.

So last summer you were saying we had peaked. Ton's of posts in http://www.early-retirement.org/forums/f44/going-all-cash-in-401k-98649.html about things like the National Debt "IMO the bear market is coming because of the national debt". It doesn't seem like the debt problem has been solved, yet the market moved higher...and higher.

I really don't get the need to do drastic 50% changes. I guess people do it in their tax-deferred accounts because they can without any tax consequences...but what makes one think they can guess THE time and place of the peak.

(But to each their own...each of us has the responsibility to manage our money.)

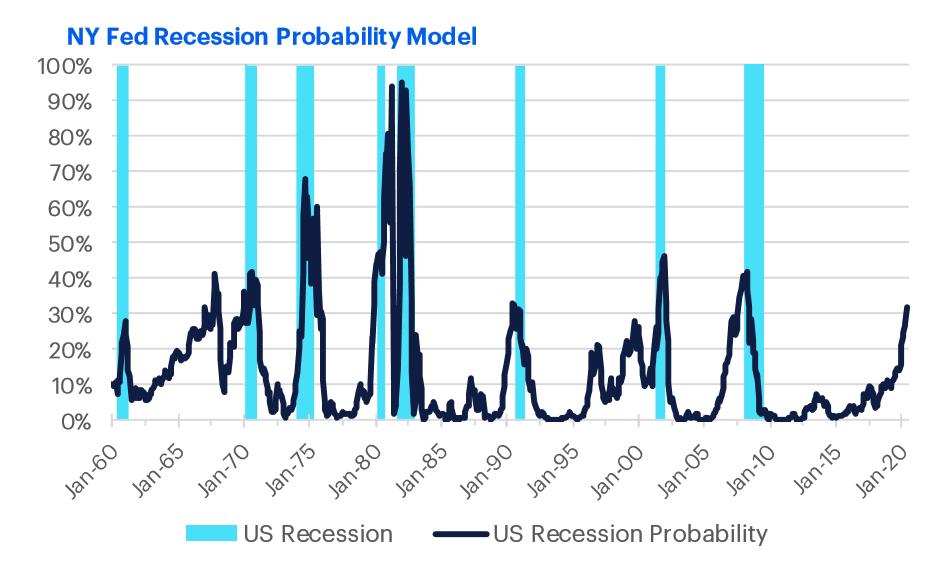

Here is some graphs to justify my decisions to be defensive:

The NY Fed probability model appears to be accurate over the years. The stock market is going up and up is because of the fed's QE and European money coming in due to negative interest rates: +1.5% is better than -1.5%. This is a spread of 3%. What happens if the Fed drops the interest rate and the spread no longer covers the currency risk? Answer: European money will flow out. My opinion of a potential bear market is similar to the experts if you google: Will there be a recession in 2020? If I am wrong, then you should tell the experts and the NY Fed that they are wrong too!

Golden sunsets

Thinks s/he gets paid by the post

- Joined

- Jun 3, 2013

- Messages

- 2,524

I took $100,000 off the table last week, selling in the morning on the rebound to a historical high and before the losses that occurred later in the day. I had rebalanced on 1-2 and 1-3, but due to market gains since I rebalanced, equities had crept up again. So far this is looking like a repeat of January 2018. Futures are off over 400 on the Dow this morning.

I took $100,000 off the table last week, selling in the morning on the rebound to a historical high and before the losses that occurred later in the day. I had rebalanced on 1-2 and 1-3, but due to market gains since I rebalanced, equities had crept up again. So far this is looking like a repeat of January 2018. Futures are off over 400 on the Dow this morning.

Good for you. I am currently 50% treasury bonds and 50% VWENX Wellington Balance fund. I may re-allocate to 75% treasury bonds and 25% VWENX as a precaution.

The cononavirus is a concern of mine because they recently discovered it can be transmitted before the symptoms appear which is during the incubation period. Historically the stock market decline but recovers quickly so there should be no long term impact. On the other hand it may be a black swan event which may trigger the recession but does not directly cause it.

NW-Bound

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Jul 3, 2008

- Messages

- 35,712

If it becomes a black swan event and spreads worldwide, then we will have survival foremost in mind instead of making more money.

copyright1997reloaded

Thinks s/he gets paid by the post

Here is some graphs to justify my decisions to be defensive:

The NY Fed probability model appears to be accurate over the years. The stock market is going up and up is because of the fed's QE and European money coming in due to negative interest rates: +1.5% is better than -1.5%. This is a spread of 3%. What happens if the Fed drops the interest rate and the spread no longer covers the currency risk? Answer: European money will flow out. My opinion of a potential bear market is similar to the experts if you google: Will there be a recession in 2020? If I am wrong, then you should tell the experts and the NY Fed that they are wrong too!

The "experts"? LOL. What were the "experts" predicting in 2016? 2017? 2018? 2019?

Too each their own. As I've stated many times, all bull markets end badly. What you don't know is the when and at what level it tops out. So you can be eventually right....but being early can cost you dearly.

Pick an allocation and use it to trim. If that number is 50% equities, then if your equity allocation goes up, sell. If it goes down buy. But to bounce from 50% invested to 0% to 50% to whatever is just gambling.

harley

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

If I am wrong, then you should tell the experts and the NY Fed that they are wrong too!

Many of us here spend a lot of time telling the experts they are wrong. Or at least pointing out that they're only occasionally right.

The "experts"? LOL. What were the "experts" predicting in 2016? 2017? 2018? 2019?

Too each their own. As I've stated many times, all bull markets end badly. What you don't know is the when and at what level it tops out. So you can be eventually right....but being early can cost you dearly.

Pick an allocation and use it to trim. If that number is 50% equities, then if your equity allocation goes up, sell. If it goes down buy. But to bounce from 50% invested to 0% to 50% to whatever is just gambling.

Since I have already met all my financial goals after buying two houses with 100% cash and I am financially secured with pensions that covers 110% of my working salary, I like to gamble with house money for my personal entertainment.

Many of us here spend a lot of time telling the experts they are wrong. Or at least pointing out that they're only occasionally right.

I am OK with that. This is because it avoid a herd mentality similar to lemming going over the cliff.

However, if you are going to disagree, I suggest supporting your case with some objective data rather than subjective opinions.

I confessed my first graph is subjective based on opinions by experts which some folks laugh at. However, the second graph is more objective since it is based on data complied by the NY Fed which is a government entity.

Unless you believe that the NY Fed developed their prediction model by witchcraft, I tend to consider it credible. This is better than merely saying "the recession ain't gonna happen"

Since I have already met all my financial goals after buying two houses with 100% cash and I am financially secured with pensions that covers 110% of my working salary, I like to gamble with house money for my personal entertainment.

No such thing as house money once it becomes your money.

I'm not saying you shouldn't gamble the money, but whatever you lose is actually your money.

DrRoy

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

I locked in a bunch of stock gains in 1992, when the Dow was 6,000. Since then I've wanted to re-invest, but I know a crash could come at any time. Whew! Guess I dodged that bullet.

Wow. There's a lesson for people. Since I FIRE'd 3 years ago, as the market has risen, I have reduced my AA from 63% equities to 58%, with the most recent adjustment being last December as I was raising 2020 spending $ anyway and needed to rebalance that.

timetraveling

Confused about dryer sheets

- Joined

- Jan 15, 2020

- Messages

- 8

Called my broker and told him to sell 100 grand of equities, 60 in the IRA and 40 from the after tax. Should have the dough early next week.

Not a lot of context provided. Without knowing how much 100 grand is compared to your total portfolio, you aren't saying much.

Similar threads

- Replies

- 15

- Views

- 853

- Replies

- 26

- Views

- 1K

- Replies

- 40

- Views

- 4K

- Replies

- 19

- Views

- 499