njhowie

Thinks s/he gets paid by the post

- Joined

- Mar 11, 2012

- Messages

- 3,931

Got it, what's you crystal ball say on likelihood of that being called during term, say 5, 10 or full 14 years out?

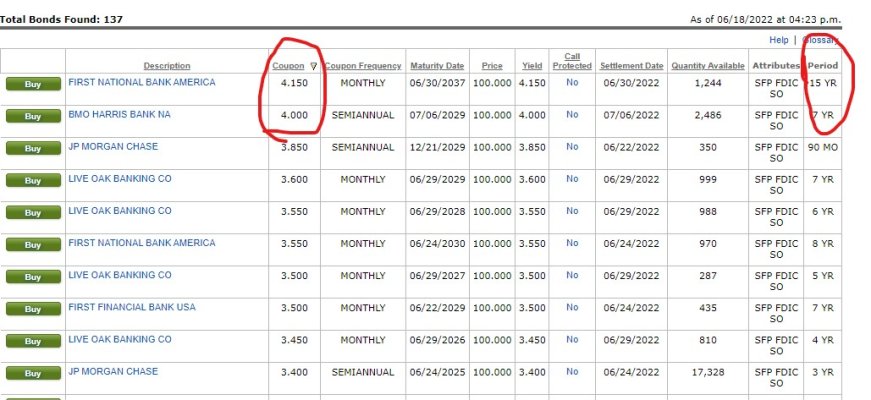

This one is funny...check out the attachment. I saw this pop up on my screen, the adrenaline spiked and I clicked buy, buy, buy quickly. It's only 2 months, but YTM came to 6.7% - so what could be bad?

We'll see if I get a call on it to bust the trade.

Makes sense, also simple something that is so obvious when someone else says it. Worst case it is called in 12 months and you got over 4% for a year to your point making it a great rate for 12 months.

Thanks.

Moody's has studied this over decades. The bottom line is that it pretty much doesn't matter. Stick to A-rated and higher and there is no safety issue.

If you want to go through the latest study, it's here:

https://www.fidelity.com/bin-public...ors-service-data-report-us-municipal-bond.pdf

I am buying some Munis for the first time on TDA, in my tIRA account.

I selected bonds&CDs:Advanced Search, selected "Municipals".

Here are the ratings options with a single "A" on the right hand side:

...

A1/A+

A2/A

A3/A-

...

When you say, "Stick to A-rated or higher", is that any rating at "A2/A" or above, or, any rating at "A3/A-" or above.

I want to make an initial purchase to get the feel of it.

The ratings and advisement in general is to stick to investment grade. This comes from Moody's long and extensive history in tracking and reporting on munis and defaults.

Before making your initial purchase, review the Moody's report, and get comfortable with the safety of what you're purchasing. They provide numerous tables and exhibits detailing what they've seen data-wise historically as far as defaults. Also be aware, in the event of a default where there is non-payment of interest and/or principal, in general the default is ultimately remedied and bondholders are made whole. Sometimes the bondholders will lose, but it is rare, and generally in these instances, there was lots of warning, with ratings downgrades - that is, it was not unexpected.

Here is the latest Moody's report:

https://www.fidelity.com/bin-public...ors-service-data-report-us-municipal-bond.pdf

Exhibit 4 on Page 12 is the one you want to focus on. It doesn't break out A+/A/A-, just A. Look at the row for A rating, and then scan upwards - defaults are almost non-existent. There is also a clear jump/delineation moving from A to Baa. The default rate at Baa is still extremely low at 1% after 10 years, but even that is significantly higher than A or better.

Rates are rising. I won’t lock into a CD over 5 yrs unlessI feel we are topping out. I did buy a 10 yr once, thought long and hard about it and it was 5% in 2011.

Rates are rising. I won’t lock into a CD over 5 yrs unlessI feel we are topping out. I did buy a 10 yr once, thought long and hard about it and it was 5% in 2011.

I use a strategy first approach. With a ladder it doesn’t matter. I can’t guess a top. When short durations mature, I buy long. Rinse and repeat. With that process I have doubled the yield of my ladder since early Spring. Think less, earn more.

What if you were trying to lock in soon a relatively stable 7 to 10 year ladder. Would you wait say 3 to 6 months knowing where rates are going here. Or simpler, at what point do you buy long? At some point doing 3 month over and over will start to go down and we may not see the opportunity again for said 7 to 10 year ladder.?

I don't have the answer really just asking for theoretical purposes. My gut says locking in a 7 to 10 year ladder for 4 to 5% will turn out to be a pretty good move historically speaking?

If you were building the ladder today from a pile of money to last you 10 years and did not have money coming in every 2 months? I am not challenging, genuinely interested.

I have X dollars, my goal is to maximize stability and earn over 3% on said pile for 10 years with idea being relatively equally withdrawal of pile each year to bridge to a date. Not social security but another life event. It's not the whole portfolio. It's a I want this chunk to last 10 years spending equal each year reducing to zero when another chunk comes online.

I use a strategy first approach. With a ladder it doesn’t matter. I can’t guess a top. When short durations mature, I buy long. Rinse and repeat. With that process I have doubled the yield of my ladder since early Spring. Think less, earn more.

I’m not guessing either. My ladder is not uniform. I skip a rung if I don’t find value. So maybe I end up with funds maturing 2, 4, and 5 years out because the 3 yr rates are not attractive and I double up on the 2’s and 4’s. A tax free muni at 4% from my high tax state is a home run all day long. I’m looking for those offers to fill rungs beyond 5 yrs. like the idea of basing it on SS. I just realized I don’t really need the ladder when SS starts which could be 6 months from now.

I have more cashflow than I need to fund my retirement needs. I don’t care about rates. I follow the strategy. It works. Long rates actually dropped this week.

I noticed the same on rates yesterday - they pulled back, again with 10-year treasury looking as if it wants to head for 3.0% over the next few weeks. The yield curve is essentially flat from 2 years out to 30 years. It will likely invert as we head in to recession. Deutsche Bank has come out calling for recession sooner and deeper than others anticipate.

.