I am a Total Return investor, or at least tell myself I am. I float around a 60/40 AA allowing myself +/- 5% leeway before I think about a rebalance and suspect I will stay in this range/approach thru retirement. It took me a while, but I finally made peace with the fact I should look at my bond allocation as a ballast, with less focus on the yield. That said, I still have a small "fight for yield" habit I am trying to kick. Today, my 40% bond allocation is roughly 64% Intermediate Core, 21% Short Term Treasuries, and 15% Preferred Stocks, all in funds/ETFs. Despite all the chatter (external and internal) saying get out of bonds, they have no place to go but down, I have stayed the course. Interestingly, my YTD Total Returns are in the 5% - 7%, 3%+, and 5%+ ranges respectively. This makes me feel good, I guess, but I have to say I really don't fully understand why they have performed like they did this year when interest rates have stayed low and money has been pumping into the stock market. So as we approach year end and I begin to plan for my AA adjustments, maybe you can help me with these questions...

- What is the "right" mix and strategy using short/medium/long term bond funds in this environment, particularly if you are not relying on only yield to fund your retirement?

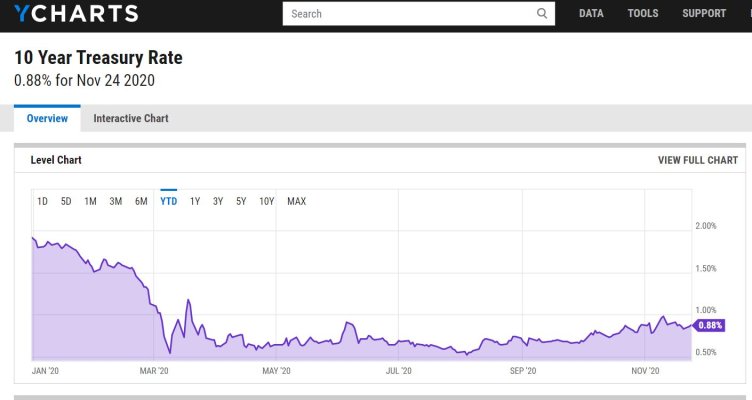

- What events dictate a change in your bond mix such as moving more money into long term bonds/moving more money into short term/staying all in intermediate bonds? What tell signs do you rely on to make any real moves here (Fed strategy, inflation, government policy, momentum of bull/bear markets)?

- Should i give up my Preferred stock habit and go clean?

For the most part, I have subscribed to Bogle's motto "Don't do something, just stand there!"

What say you?

- What is the "right" mix and strategy using short/medium/long term bond funds in this environment, particularly if you are not relying on only yield to fund your retirement?

- What events dictate a change in your bond mix such as moving more money into long term bonds/moving more money into short term/staying all in intermediate bonds? What tell signs do you rely on to make any real moves here (Fed strategy, inflation, government policy, momentum of bull/bear markets)?

- Should i give up my Preferred stock habit and go clean?

For the most part, I have subscribed to Bogle's motto "Don't do something, just stand there!"

What say you?