Midpack

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Not new information and I realize those affected already know far more than I do, but I don't think most people (self-included) have really thought about it beyond a vague concept, about actual financial implications. I know some people think the promises made are guarantees, some may be very unpleasantly surprised. It would seem this will probably impact everyone, not just retirees and not just taxpayers, despite protestations by both. It won't be as simple as cutting current/future benefits, nor as simple as increasing taxes/fees to erase shortfalls IMHO.

I'd rather we just faced up to it, so we could all plan accordingly, but another case of kicking the can down the road it seems...see Illinois.

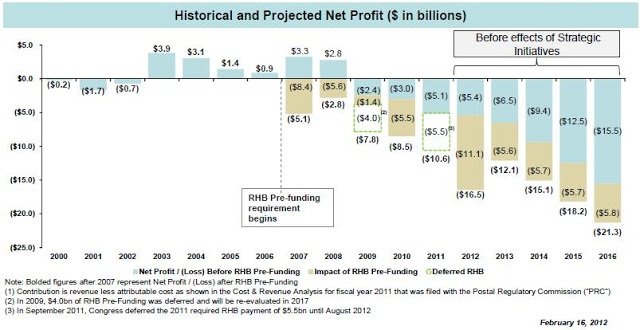

Pandemic of pension woes is plaguing the nation

I'd rather we just faced up to it, so we could all plan accordingly, but another case of kicking the can down the road it seems...see Illinois.

Seventeen states have funded more than 80 percent of their projected pension liability, a level that's generally seen as financially sound. Most of the rest have been scrambling to make up investment losses inflicted by the 2008 market collapse and the shortfalls in sales, property and incomes taxes produced by the Great Recession.

But even as the economy and housing markets have recovered, most states are still falling behind in closing their pension funding gaps. In the last year, 34 states have seen their pension funds stretched further as they've failed to make the full contributions needed to meet the projected cost of retirement promises.

Nine states—Hawaii, Alaska, Kansas, Rhode Island, New Hampshire, Louisiana, Connecticut, Kentucky and Illinois—have now set aside less than 60 percent of what they need. Illinois has saved just 43 cents to cover every dollar of what it needs to pay 350,000 retirees and 500,000 current plan participants who are counting on a pension check.

Pandemic of pension woes is plaguing the nation

")