"Banana" is my favorite answer to those kinds of questions.

Could you give me your last 4 of the SSN?

"Banana" is my favorite answer to those kinds of questions.

Yeah. I wouldn't call it complicated. I'd call it extremely limited. I guess in the extreme, your will would take over. I suppose that could be complicated depending on your estate. I don't look upon this account as a long term situation, just grabbing some extra interest.

Could you give me your last 4 of the SSN?

Do you really think that's the name of the fruit I use as an answer?

The last four of my SS are "0000".

No. No. No. You never, never, never, give real answers to those questions. Never. That information can be looked up by the bad guys. Always give fake answers.

First manager: bumblebum

3rd grade teacher: bonecrusher

first dog's name: asteroidbx43

Make sure you write down whatever nonsense you use.

Heard back. In a nutshell, they don't add beneficiaries or POD's, but they "have a process in place in a situation where they are notified of the death of an owner."

Could you give me your last 4 of the SSN?

We have a couple 2.25% CDs that mature in August... ugh!

Marcus sent email earlier today - 18-month CD 0.7% APY

https://www.marcus.com/us/en/savings/high-yield-cds/18MCD

We have a couple 2.25% CDs that mature in August... ugh!

I have a brokered CD currently paying 4.125% (step CD that started at 2.25%) that matures in Sept 2024 from HSBC. They had one chance to call it in Sept 2019 when the rate moved up, and they botched it, not giving sufficient notice of the call. So a few days after it was redeemed, they had to reverse it, taking back the cash, giving me back the CDs, and since then they have to pay it out through the 2024 maturity date at 4.125%.

I wrote about it here:

https://www.early-retirement.org/fo...ll-rate-goes-to-4-125-for-5-years-100058.html

I have lots of others between 2.0% and 3.8% with maturities out to 2030. Maybe half are callable, some are well past their call dates. For those past their call dates, I can only imagine that the banks somehow lost track or forgot about them, or the issue was simply too small to justify calling them. My JPM CDs have been called left and right - even those with seemingly low interest rates. However, I still have one that's 3.05% with May 2030 maturity that's been callable since May 2020 - and for some reason they haven't called it. I'm certainly not complaining, but definitely has to be some sort of oversight.

This morning I bought one that popped up on my screen - another HSBC. 2.61% yield to maturity in Sept 2027. It is callable Sept 2022 for YTC of 0.533%. Both the YTC and YTM are favorable compared to new (brokered) CDs with those maturities, so I took it. The coupon is 3.125%, so it is likely to be called. However, it is HSBC and considering the prior botched call (I also have another where the same happened) you never know.

That's really cool. How are you screening for brokered CDs? Is it automated?

Does anyone have experience with MYGAs (Multi Year Guaranteed Annuities)? From my research, there are no fees and minimal risk. I would love to hear from others who use this as a vehicle for cash.

Thanks Audrey and Jazz!

Business Checking Suggestion - If you have a business (including sole proprietorship), Chase has a good/easy offer of $750 bonus: Deposit $10k and hold for 60 days and make 25 transactions (i.e. debit card or others) within 90 days. Bonus deposited within 14 days of meeting criteria. There is a minimum account balance criteria to avoid the service fee of $15/month, but that can be waved for various reasons.

I just opened an account and my time investment was 30 minutes.

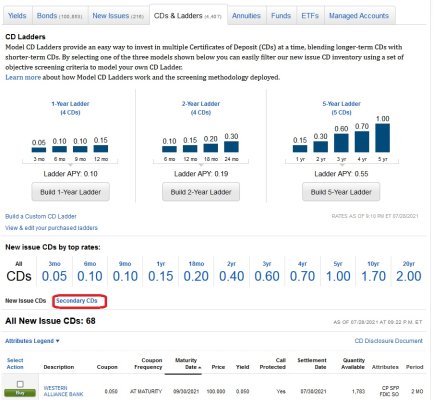

Didnt work for me, must be a memberFor Fidelity, go to the CD page and if you scroll down a little, on the left, next to New Issue CDs will be a link for Secondary CDs. Click on that link, show all the CDs (if there's less than 3000, if more, set the minimum yield to 0). When the list displays, just click on the yield to maturity column to sort from highest to lowest.