EvrClrx311

Full time employment: Posting here.

- Joined

- Feb 8, 2012

- Messages

- 648

I understand that a lot of factors can influence the math (some are addressed below and if any are missing please chime in), but from a strictly cash-flow perspective here was my analysis of when to collect...

I'm only 33 (well turning 34 this week), so long way out for me. I'm just curious to run these numbers as an abstract scenario. I'm sure the rules and game will change significantly in the next three decades, for me...

Exploring three cases:

1) Social Security Is All You Have

Assuming you have absolutely nothing saved and are using the money, need it, as cash flow and it is spent when it is received. I suppose this is the normal. I mean who collects social security and saves/invests it? I suppose the super wealthy or FIRE types... I'll explore that a little lower as a comparison, because it does seem to change the math and answer to when it is best to collect.

Numbers make this easier so I'll use mine:

62 - $1,846

67 - $2,622

70 - $3,252

So obviously collecting at 62 is ideal if you plan to die anytime before a certain age at which the other two catch up. Example... if you waited till 70 and died just before collecting your first check you would have missed out on $177,000 in checks from 62-70 had you instead collected early at 62. So here are the break even points:

If you reached age 79, then collecting at full age (67) would have been better. If you reached 83, then collecting late (70) would have been better.

Hope the formatting of this table works out

=======

2) Social Security Supplements Nest Egg

Now assuming you could save/invest this money... or more realistically, you could take less out of your nest egg because of the funds you'll receive from Social Security. Lets assume for this case that you are receiving a 4% real yield on your retirement savings. Essentially, collection of social security allows you to save the difference (what you collected) at a rate of 4% a year.

Here is how things change:

Now you'd have to reach age 85 before waiting till full age (67) made more sense and you'd have to reach age 89 before waiting till 70 to collect would make more sense.

=======

3) Social Security Is Saved Entirely (Too Wealthy To Care)

If you also consider the case of someone who simply wanted to take their social security checks, invest them in equities, and built more wealth (say for an estate) lets look at a case where someone got a historical 6% real return on their checks and see how that affects things.

You'd have to reach late 90's for collecting after 62 to make more sense.

=======

Personally I have a long way to go to worry about this. My hope is that Social Security is such a small piece of my retirement planning that it doesn't matter much at all by the time I get there. I hope I'm able to avoid this math at that point (being FI) and just take it as a bonus to enjoy life, or spoil my children and future grandchildren.

I'm only 33 (well turning 34 this week), so long way out for me. I'm just curious to run these numbers as an abstract scenario. I'm sure the rules and game will change significantly in the next three decades, for me...

Exploring three cases:

1) Social Security Is All You Have

Assuming you have absolutely nothing saved and are using the money, need it, as cash flow and it is spent when it is received. I suppose this is the normal. I mean who collects social security and saves/invests it? I suppose the super wealthy or FIRE types... I'll explore that a little lower as a comparison, because it does seem to change the math and answer to when it is best to collect.

Numbers make this easier so I'll use mine:

62 - $1,846

67 - $2,622

70 - $3,252

So obviously collecting at 62 is ideal if you plan to die anytime before a certain age at which the other two catch up. Example... if you waited till 70 and died just before collecting your first check you would have missed out on $177,000 in checks from 62-70 had you instead collected early at 62. So here are the break even points:

If you reached age 79, then collecting at full age (67) would have been better. If you reached 83, then collecting late (70) would have been better.

Hope the formatting of this table works out

HTML:

62 67 70

62 $1,846.00 $2,622.00 $3,252.00

63 $22,152.00

64 $44,304.00

65 $66,456.00

66 $88,608.00

67 $110,760.00

68 $132,912.00 $31,464.00

69 $155,064.00 $62,928.00

70 $177,216.00 $94,392.00

71 $199,368.00 $125,856.00 $39,024.00

72 $221,520.00 $157,320.00 $78,048.00

73 $243,672.00 $188,784.00 $117,072.00

74 $265,824.00 $220,248.00 $156,096.00

75 $287,976.00 $251,712.00 $195,120.00

76 $310,128.00 $283,176.00 $234,144.00

77 $332,280.00 $314,640.00 $273,168.00

78 $354,432.00 $346,104.00 $312,192.00

79 $376,584.00 $377,568.00 $351,216.00

80 $398,736.00 $409,032.00 $390,240.00

81 $420,888.00 $440,496.00 $429,264.00

82 $443,040.00 $471,960.00 $468,288.00

83 $465,192.00 $503,424.00 $507,312.00

84 $487,344.00 $534,888.00 $546,336.00

85 $509,496.00 $566,352.00 $585,360.00

86 $531,648.00 $597,816.00 $624,384.00

87 $553,800.00 $629,280.00 $663,408.00

88 $575,952.00 $660,744.00 $702,432.00

89 $598,104.00 $692,208.00 $741,456.00

90 $620,256.00 $723,672.00 $780,480.00

91 $642,408.00 $755,136.00 $819,504.00

92 $664,560.00 $786,600.00 $858,528.00

93 $686,712.00 $818,064.00 $897,552.00

94 $708,864.00 $849,528.00 $936,576.00

95 $731,016.00 $880,992.00 $975,600.00

96 $753,168.00 $912,456.00 $1,014,624.00

97 $775,320.00 $943,920.00 $1,053,648.00

98 $797,472.00 $975,384.00 $1,092,672.00

99 $819,624.00 $1,006,848.00 $1,131,696.00

100 $841,776.00 $1,038,312.00 $1,170,720.00=======

2) Social Security Supplements Nest Egg

Now assuming you could save/invest this money... or more realistically, you could take less out of your nest egg because of the funds you'll receive from Social Security. Lets assume for this case that you are receiving a 4% real yield on your retirement savings. Essentially, collection of social security allows you to save the difference (what you collected) at a rate of 4% a year.

Here is how things change:

Now you'd have to reach age 85 before waiting till full age (67) made more sense and you'd have to reach age 89 before waiting till 70 to collect would make more sense.

HTML:

62 67 70

62 $1,846.00 $2,622.00 $3,252.00

63 $22,595.04

64 $46,093.88

65 $70,532.68

66 $95,949.02

67 $122,382.02

68 $149,872.35 $32,093.28

69 $178,462.28 $65,470.29

70 $208,195.81 $100,182.38

71 $239,118.68 $136,282.96 $39,804.48

72 $271,278.47 $173,827.56 $81,201.14

73 $304,724.65 $212,873.94 $124,253.66

74 $339,508.68 $253,482.18 $169,028.29

75 $375,684.06 $295,714.74 $215,593.90

76 $413,306.47 $339,636.61 $264,022.14

77 $452,433.76 $385,315.36 $314,387.50

78 $493,126.15 $432,821.25 $366,767.48

79 $535,446.24 $482,227.38 $421,242.66

80 $579,459.13 $533,609.76 $477,896.85

81 $625,232.54 $587,047.43 $536,817.20

82 $672,836.88 $642,622.60 $598,094.37

83 $722,345.39 $700,420.79 $661,822.63

84 $773,834.25 $760,530.90 $728,100.01

85 $827,382.66 $823,045.42 $797,028.49

86 $883,073.00 $888,060.51 $868,714.11

87 $940,990.96 $955,676.21 $943,267.16

88 $1,001,225.64 $1,025,996.54 $1,020,802.32

89 $1,063,869.71 $1,099,129.68 $1,101,438.90

90 $1,129,019.54 $1,175,188.15 $1,185,300.93

91 $1,196,775.36 $1,254,288.96 $1,272,517.45

92 $1,267,241.41 $1,336,553.80 $1,363,222.63

93 $1,340,526.11 $1,422,109.23 $1,457,556.01

94 $1,416,742.19 $1,511,086.88 $1,555,662.73

95 $1,496,006.92 $1,603,623.63 $1,657,693.72

96 $1,578,442.24 $1,699,861.86 $1,763,805.95

97 $1,664,174.97 $1,799,949.61 $1,874,162.67

98 $1,753,337.01 $1,904,040.88 $1,988,933.66

99 $1,846,065.53 $2,012,295.79 $2,108,295.48

100 $1,942,503.19 $2,124,880.90 $2,232,431.78=======

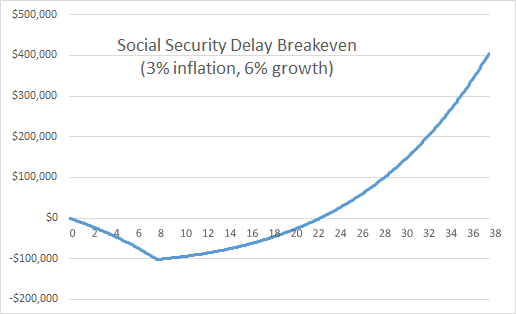

3) Social Security Is Saved Entirely (Too Wealthy To Care)

If you also consider the case of someone who simply wanted to take their social security checks, invest them in equities, and built more wealth (say for an estate) lets look at a case where someone got a historical 6% real return on their checks and see how that affects things.

You'd have to reach late 90's for collecting after 62 to make more sense.

HTML:

62 67 70

62 $1,846.00 $2,622.00 $3,252.00

63 $22,816.56

64 $47,002.11

65 $72,638.80

66 $99,813.69

67 $128,619.07

68 $159,152.77 $32,407.92

69 $191,518.50 $66,760.32

70 $225,826.17 $103,173.85

71 $262,192.30 $141,772.21 $40,194.72

72 $300,740.40 $182,686.46 $82,801.12

73 $341,601.38 $226,055.57 $127,963.91

74 $384,914.03 $272,026.82 $175,836.47

75 $430,825.43 $320,756.35 $226,581.37

76 $479,491.51 $372,409.65 $280,370.98

77 $531,077.56 $427,162.15 $337,387.95

78 $585,758.78 $485,199.80 $397,825.95

79 $643,720.86 $546,719.70 $461,890.23

80 $705,160.68 $611,930.81 $529,798.36

81 $770,286.88 $681,054.58 $601,780.98

82 $839,320.65 $754,325.77 $678,082.56

83 $912,496.45 $831,993.24 $758,962.24

84 $990,062.79 $914,320.75 $844,694.69

85 $1,072,283.12 $1,001,587.92 $935,571.09

86 $1,159,436.67 $1,094,091.11 $1,031,900.08

87 $1,251,819.43 $1,192,144.50 $1,134,008.80

88 $1,349,745.16 $1,296,081.09 $1,242,244.05

89 $1,453,546.42 $1,406,253.87 $1,356,973.41

90 $1,563,575.77 $1,523,037.02 $1,478,586.54

91 $1,680,206.88 $1,646,827.17 $1,607,496.45

92 $1,803,835.85 $1,778,044.72 $1,744,140.96

93 $1,934,882.56 $1,917,135.32 $1,888,984.14

94 $2,073,792.07 $2,064,571.36 $2,042,517.90

95 $2,221,036.16 $2,220,853.56 $2,205,263.70

96 $2,377,114.89 $2,386,512.69 $2,377,774.24

97 $2,542,558.34 $2,562,111.37 $2,560,635.41

98 $2,717,928.40 $2,748,245.98 $2,754,468.26

99 $2,903,820.67 $2,945,548.66 $2,959,931.07

100 $3,100,866.47 $3,154,689.49 $3,177,721.66=======

Personally I have a long way to go to worry about this. My hope is that Social Security is such a small piece of my retirement planning that it doesn't matter much at all by the time I get there. I hope I'm able to avoid this math at that point (being FI) and just take it as a bonus to enjoy life, or spoil my children and future grandchildren.

Last edited:

Not a realistic option with zero savings... unless you work those 8 years...

Not a realistic option with zero savings... unless you work those 8 years...