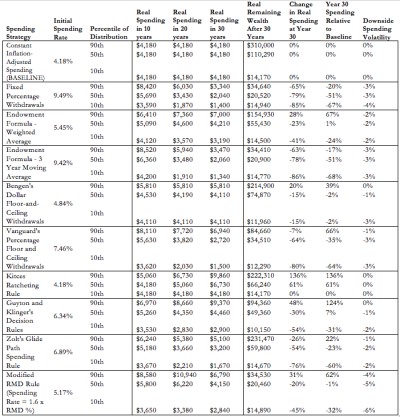

In my view the Trinity and Firecalc approach is useless for extreme potential horizons. The title is kind of grandiose "Ultimate?" too.

Why? Because once you go beyond 50 or years or so some things happen:

- You have to live from capital returns, not capital buffers

- Historical sample sizes become too small

- Start and end valuation multiples matter less

- The odds of other events start dominating, from revolutions to sudden sickness, tax changes etc ..

The best guess for equities comes from going back to the source of your capital returns: world economic growth and typical real earnings yield. It represents future growth + current payoffs.

The first has been pretty rock solid at 3% real, the second one at 3% or so (5% - 2% inflation), bouncing around quite a bit.

What you are doing when planning for an expected return is making assumptions about those two numbers. It's the same approach that Bogle uses btw.

Personally I'm aiming for 2% growth [lower population growth] and 2.5% current real yield, so 4.5% as a rough sketch.

Funnily enough this approaches the Trinity results, so I guess I'm sort of contradicting myself here

")

Let's just say it's the right result with the wrong approach

In addition I'd argue that going above 75% equities is not wise at all. For a few theoretical percentage points success increase one gives up the opportunity to move to a higher equity percentage and buy low when stuff hits the fan (or floor). In addition you'll pay an emotional toll in the form of higher volatility.

Long story short: 3% or even 5%, and financial worry should not be #1. You can't get more precision out of the fuzzy future anyway.

and group hug and be happy!

and group hug and be happy!