Golden sunsets

Thinks s/he gets paid by the post

- Joined

- Jun 3, 2013

- Messages

- 2,524

OK made me look. PRR for the year to date without cash is 2.15%. Including cash it is 1.93%. I'll take it.

54/41/5

54/41/5

Last edited:

| Categories | ETF/Fund | Current % | Desired % | |||

| Fixed Income Allocation | 25.49% | 26.00% | ||||

| Total Bond Market | BND, AGG | 19.63% | 13.00% | |||

| TSP G Fun | TSP G Fund | 5.46% | 13.00% | |||

| Cash | CASH | 0.40% | 0.00% | |||

| Total Stock Allocation | 74.51% | 74.00% | ||||

| International Stock Allocation | 33.63% | 32.89% | ||||

| Emerging Market | VWO | 11.34% | 10.97% | |||

| Regional - Pacific | VPL | 11.26% | 10.97% | |||

| Regional - Europe | VGK | 11.03% | 10.97% | |||

| United States Stock Allocation | 40.89% | 41.11% | ||||

| United States REIT | VNQ | 8.14% | 8.22% | |||

| United States Small Cap Value | VBR | 10.91% | 10.96% | |||

| United States Large Cap Blend | VV | 11.00% | 10.96% | |||

| United States Large Cap Value | VTV | 10.84% | 10.96% | |||

In a stroke of luck - I thought S&P index was oversold and had quadrupled our international exposure at year end, which is up over 4%.

That's pretty. I say so because it looks a bit like mineFor comparison sake here is my allocation.

Up 2.80% as of today h a 65/30/5 mix.

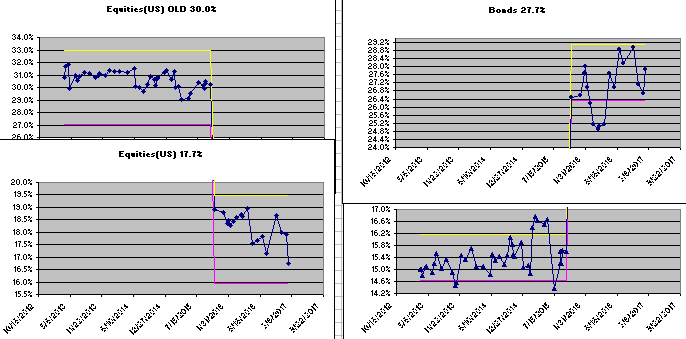

What was that CAPE signal?Yeah, it was in late 2015 when I lightened-up on US equities due to the CAPE signal. This year, it must be that some of those things dragging my return down for a while are finally getting a little love.

Hey, even mine tooUp 2.1% YTD as of Friday. Hard to believe!

(I was so lagging behind at the end of last month). What a difference a week can make!I tried to find the answer in the previous year threads, butthey are so long.

You only include interest and returns when figuring out the percentage, not money you're adding into the pot right? That makes the most sense to me.