You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

How to pick stocks

- Thread starter 4nursebee

- Start date

Research

Lots

Excellent

What kind of returns relative to the SP500?

What is excellent in your opinion?

OldShooter

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Almost 50 years of statistical and academic research says that stock picking doesn't work, but you can read all kinds of boasting about winning trades on the internet. The thing to understand is that losers don't post.How do you pick stocks to invest in?

How much work do you do before investing and while investing?

How are your returns using your methods?

Thanks

Read Charles Ellis' "Winning the Loser's Game" or Burton Malkiel's "A Random Walk Down Wall Street."

Also think about this: If there is someone who actually can pick winning stocks consistently, he/she is on a tropical island sipping a drink from a glass garnished with an orchid. He/she is not hanging around the internet giving secrets away for free and is not working for some mutual fund, wearing a suit and commuting to work in a building where the windows don't even open. He/she is also not writing click bait for the internet or hustling to sell an investment advisory letter. These are sure ways to identify losers.

Dash man

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

What kind of returns relative to the SP500?

What is excellent in your opinion?

The point of my brief answers is there are no short cuts that you’ll find on this thread. Many on this forum are great at saving and investing in low cost mutual funds and setting up asset allocations based on their goals and needs. They are great at planning and budgeting, and most importantly, living below their means. People here can help you with these things.

However, investing in individual stocks is an entirely different ballgame. I have an MBA, experience in business, and read many books, articles, blogs and learned a lot from my own mistakes.

I don’t listen to stock tips. I read financial statements, annual reports, only invest in profitable companies that provide services or products that I understand. I diversify the kinds of stocks I have, and expand that diversification with a few ETFs. I monitor my stocks and am not afraid to sell if the fundamentals of a company are going downhill. I’m not afraid of a market crash and hold on. I may increase my holdings if the companies are still strong.

It’s a lot of work.

Oz investor

Full time employment: Posting here.

https://www.investopedia.com/terms/s/sp500.asp

the S&P 500 is a slow moving target ( companies MIGHT change in the index ) but not a stationary target ,

whereas a portfolio of say 10 stocks might survive a lifetime

you need a LOT of research but also some fore-thought

for instance i don't expect to live more than another 10 years so i will invest in ( some ) coal companies , and should get dividends from those miners for the rest of my life , you might be looking up to 40 years ahead so might be trying to guess future trends ( beyond Apple and GE )

my focus is on robust income ( dividends in good markets and bad ) with a lesser focus on growing the $value on assets ( since i plan to resist withdrawing cash except in extreme situations )

BUT i will selectively continue to dividend reinvest to help resist inflation ( which i think will return in the next few years

i don't rely exclusively in my stock-picking ability , i also use ( index ) ETFs as an 'insurance policy ' ( against bad stock selection ) along with LICs and REITs where the manager is ( more ) skilled in sectors and investment styles , that i am not good at ( and probably won't have time to gain the required experience )

this clip might prove helpful

https://d.tube/#!/v/themoneygps/ied70r38

mow does my portfolio perform ?

it provides an adequate income ( with a little extra to reinvest )

i don't bother with other metrics , i would rather use that time to research ( and think ) new strategies and opportunities ( 'performance ' is important to fund managers , having the bills under control is important to me )

the S&P 500 is a slow moving target ( companies MIGHT change in the index ) but not a stationary target ,

whereas a portfolio of say 10 stocks might survive a lifetime

you need a LOT of research but also some fore-thought

for instance i don't expect to live more than another 10 years so i will invest in ( some ) coal companies , and should get dividends from those miners for the rest of my life , you might be looking up to 40 years ahead so might be trying to guess future trends ( beyond Apple and GE )

my focus is on robust income ( dividends in good markets and bad ) with a lesser focus on growing the $value on assets ( since i plan to resist withdrawing cash except in extreme situations )

BUT i will selectively continue to dividend reinvest to help resist inflation ( which i think will return in the next few years

i don't rely exclusively in my stock-picking ability , i also use ( index ) ETFs as an 'insurance policy ' ( against bad stock selection ) along with LICs and REITs where the manager is ( more ) skilled in sectors and investment styles , that i am not good at ( and probably won't have time to gain the required experience )

this clip might prove helpful

https://d.tube/#!/v/themoneygps/ied70r38

mow does my portfolio perform ?

it provides an adequate income ( with a little extra to reinvest )

i don't bother with other metrics , i would rather use that time to research ( and think ) new strategies and opportunities ( 'performance ' is important to fund managers , having the bills under control is important to me )

target2019

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

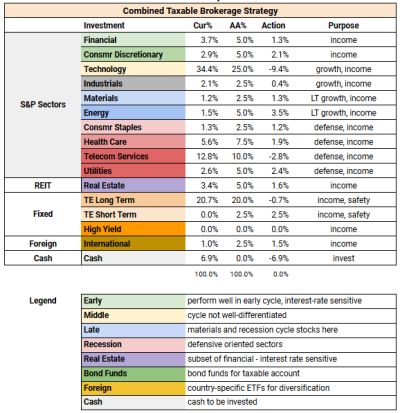

For a general investing framework, I use the chart below to guide me to specific companies to add or subtract from portfolio. I tend to evaluate what is in the bin already, like VZ, and decide if I am overweight/underweight in the sector. Then I consider the economic cycle. This is a work-in-progress, in that stock gifts, inherited, and some purchased are being combined into a family portfolio that we will pass on eventually. I don't short anything, but do cut the losers in a year or two. GE and HCP are good examples of how little I know.How do you pick stocks to invest in?

I would call it an advanced hobby. I enjoy reading about finance and business, and consider myself a decent amateur. I don't attend to these things each day, just approach it, look, and try to learn about what I avoided most of my life.How much work do you do before investing and while investing?

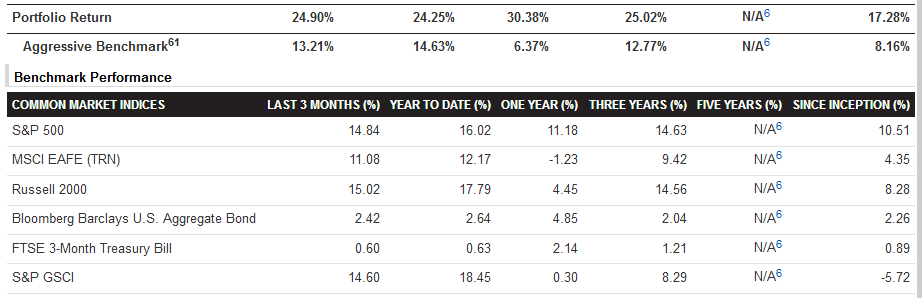

The second chart below shows performance in one-half of the brokerages total. The other half was recently inherited, it is up, but there is no performance to report that would be meaningful.How are your returns using your methods?

As you can see, we have been lucky. I don't consider this to be a result of my investing skills. Just eccentric luck and good guesses.

Attachments

W2R

Moderator Emeritus

I don't buy individual stocks. Instead I prefer to buy broad mutual funds at vanguard dot com, such as the Vanguard Total Stock Market Index Fund, and their Total Bond Market Index Fund.

travelover

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Mar 31, 2007

- Messages

- 14,328

What OldShooter said. Pick an allocation, (60% stocks / 40% bonds works for me) invest in a total stock index fund and a total bond index fund and then go do something fun. Re-balance yearly, if you want to.

Last edited:

I have bought individual stocks, with some real winners, and some real losers. I found that it was generally not worth the effort, I could do about the same with a low cost fund.

What does work for me is holding/trading discounted closed end funds with a portion of my portfolio. Currently long on DNI and RIF, both because of their current discounts. IRL is cureently part of my international holding. Will repurchase CET when it returns to its historical discount, it is usually part of my "core" holding, though I don't have any right now. Toying with buying PEO if its discount widens.

What does work for me is holding/trading discounted closed end funds with a portion of my portfolio. Currently long on DNI and RIF, both because of their current discounts. IRL is cureently part of my international holding. Will repurchase CET when it returns to its historical discount, it is usually part of my "core" holding, though I don't have any right now. Toying with buying PEO if its discount widens.

Oz investor

Full time employment: Posting here.

there was definitely some luck ( + some inheritance ) involved with me

for a start i wandered into investing in 2011 , however there will probably be a significant downturn within the next 2 years , so you might be late but even luckier ( especially if you have some wisdom as your investment partner )

unless you dabble with leverage ( margin loans ) you can only lose 100% of your cash ( and your confidence ) but a winning stock can return your investment many times over given time ,

so losing SOMETIMES is not so bad as long as you win your share as well

( but don't forget to seriously consider taking some profit or rescue that investment cash , from time to time .. some stocks are all excitement and no profit )

for a start i wandered into investing in 2011 , however there will probably be a significant downturn within the next 2 years , so you might be late but even luckier ( especially if you have some wisdom as your investment partner )

unless you dabble with leverage ( margin loans ) you can only lose 100% of your cash ( and your confidence ) but a winning stock can return your investment many times over given time ,

so losing SOMETIMES is not so bad as long as you win your share as well

( but don't forget to seriously consider taking some profit or rescue that investment cash , from time to time .. some stocks are all excitement and no profit )

There are tons of people who successfully picked stocks, they just did it through their employer via stock options.

But really anyone else could have done it. Pretty much anyone buying Amazon and holding it has trounced the market return over the past 15 years.

I guess the secret isn't so much how to pick stocks, but rather how to pick the one good stock that you can just run with.

But really anyone else could have done it. Pretty much anyone buying Amazon and holding it has trounced the market return over the past 15 years.

I guess the secret isn't so much how to pick stocks, but rather how to pick the one good stock that you can just run with.

OldShooter

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Right. And Will Rogers gave us the recipe for stock picking: "If it don't go up, don't buy it."There are tons of people who successfully picked stocks, they just did it through their employer via stock options.

But really anyone else could have done it. Pretty much anyone buying Amazon and holding it has trounced the market return over the past 15 years.

I guess the secret isn't so much how to pick stocks, but rather how to pick the one good stock that you can just run with.

Odd coincidence: When this post popped into my email I was looking at the abstract of Michael Jensen's PhD thesis published over 50 years ago in 1967. He says:

"The evidence on mutual fund performance indicates not only that these 115 mutual funds were on average not able to predict security prices well enough [over 10 years, 1945 to 1964] to outperform a buy-the-market-and-hold policy, but also that there is very little evidence that any individual fund was able to do significantly better than that which we expected from mere random chance. It is also important to note that these conclusions hold even when we measure the fund returns gross of management expenses (that is assume their bookkeeping, research, and other expenses except brokerage commissions were obtained free). Thus on average the funds apparently were not quite successful enough in their trading activities to recoup even their brokerage expenses."

Re stock options, that is not always a winning strategy either. Enron, for example. Same-o, probably, with Sears Holdings and GE. I was personally successful at this, though, when working for megacorp. We could save by payroll deduction and every fall they would sell us shares at a 15% discount, which I immediately sold.

copyright1997reloaded

Thinks s/he gets paid by the post

Long long ago, I bought my first stock long before doing mutual fund investing. This was back in the bad old days when the typical fee was over $100 on 100 shares of something, and where there was no on-line sources to look up stock information. The 'best' publications at the time where the S&P stock sheets and Value-Line ratings. My technique then is similar to now - look for companies where long term trends will act as a tailwind; financially conservative; and who can further develop a 'moat' around their business (whether that be technological, legal/patent, or even a philosophy that helps to distinguish them from their competitors).

By tailwind, I mean companies in areas where technological or demographic changes can help them over a long period of time. When I started investing (in 1978), I worked for a high-tech firm, can could see that with every crank of the technology wheel would bring new applications that would now be possible that weren't possible before. Thus, companies that were making this change possible would benefit. An example of demographic changes is the aging of America - this in conjunction with technology would mean systemic improvements in medical devices and uses of those devices.

In terms of conservative finances this means to not get caught up in growth through leverage. Leverage can be a wonderful thing on the upside, but to me introduces too much risk. The winners are those who have cash to pick up the over-levered when the cycle turns down (as most recently happened in 2008/2009).

By moat, this means not only that the company in question is in an industry with barriers to entry, but perhaps more importantly fosters customer relationships and values those relationships.

Unlike OldShooter, I think it is possible for the individual investor to outperform the market but agree when it comes to actively managed mutual funds (in that it is extremely difficult for them to do so for a prolonged period of time). More importantly, but investing in individual securities, you can better time capital gains realization.

Having said that, if you are new to investing, the vast majority of your investments should be in passively managed index funds. If you want to venture past this, it should only be with a small amount of money (at first), and you must be prepared to spend time analyzing possible investments.

Oh, one other thing. I've had my share of losers. With each investment, you should have a reason you are buying it, and a reason you are buying it now. That is, an investment thesis. Regardless of whether it goes up, down, or sideways, you need to be prepared to look at the investment and ask if you would buy it today based on your thesis. If the answer is no, get rid of it (regardless of whether you have a profit or loss on the holding).

Some of the winners using the above over the years: Stryker (first purchased in 1980), UpJohn, Linear Technology (1992), Marriott (1990), Apple (2000), Baxter (1989), Edwards Life Sciences (BAX Spin off), Honeywell (2003), ABT/ABBV(2010), MSFT. As you can see, many of these are very long term holdings. My basis on Apple is $1.40, on Baxter $5.92, Edwards $2.02, ADI (which bought LLTC) $0.13, ...

On the other hand, I've missed some good things because I will not pay up for super-sized growth. This means I've missed things like NFLX (not quite true as I owned it not long after it went public - ugh), Facebook (also not true as I owned and sold it as I thought it was too expensive), and missed MSFT in the 80's. (Big ugh). But, I recognize this is an outcome of my approach.

FWIW...

By tailwind, I mean companies in areas where technological or demographic changes can help them over a long period of time. When I started investing (in 1978), I worked for a high-tech firm, can could see that with every crank of the technology wheel would bring new applications that would now be possible that weren't possible before. Thus, companies that were making this change possible would benefit. An example of demographic changes is the aging of America - this in conjunction with technology would mean systemic improvements in medical devices and uses of those devices.

In terms of conservative finances this means to not get caught up in growth through leverage. Leverage can be a wonderful thing on the upside, but to me introduces too much risk. The winners are those who have cash to pick up the over-levered when the cycle turns down (as most recently happened in 2008/2009).

By moat, this means not only that the company in question is in an industry with barriers to entry, but perhaps more importantly fosters customer relationships and values those relationships.

Unlike OldShooter, I think it is possible for the individual investor to outperform the market but agree when it comes to actively managed mutual funds (in that it is extremely difficult for them to do so for a prolonged period of time). More importantly, but investing in individual securities, you can better time capital gains realization.

Having said that, if you are new to investing, the vast majority of your investments should be in passively managed index funds. If you want to venture past this, it should only be with a small amount of money (at first), and you must be prepared to spend time analyzing possible investments.

Oh, one other thing. I've had my share of losers. With each investment, you should have a reason you are buying it, and a reason you are buying it now. That is, an investment thesis. Regardless of whether it goes up, down, or sideways, you need to be prepared to look at the investment and ask if you would buy it today based on your thesis. If the answer is no, get rid of it (regardless of whether you have a profit or loss on the holding).

Some of the winners using the above over the years: Stryker (first purchased in 1980), UpJohn, Linear Technology (1992), Marriott (1990), Apple (2000), Baxter (1989), Edwards Life Sciences (BAX Spin off), Honeywell (2003), ABT/ABBV(2010), MSFT. As you can see, many of these are very long term holdings. My basis on Apple is $1.40, on Baxter $5.92, Edwards $2.02, ADI (which bought LLTC) $0.13, ...

On the other hand, I've missed some good things because I will not pay up for super-sized growth. This means I've missed things like NFLX (not quite true as I owned it not long after it went public - ugh), Facebook (also not true as I owned and sold it as I thought it was too expensive), and missed MSFT in the 80's. (Big ugh). But, I recognize this is an outcome of my approach.

FWIW...

copyright1997reloaded

Thinks s/he gets paid by the post

Another (shorter) post about how I invest:

1) I believe you need to give investments "time". Most of my purchases are not for a quick trade (I do sometimes do this, but that is another topic). Rather, I am looking for something that will work out over years and as you can see from my holdings decades. This means that you need to be prepared for significant downturns in Mr. Market's appraisal of your holding, and be prepared to turn out negative news flow. Each of the securities I mentioned in the prior post have had time frames where their valuation significantly declined. Let's take Apple as an example. I bought it in 2000 primarily on these factors: It was cash rich. At the time, the stock was $19/share and they had $13 in cash. Many people were predicting the demise of Apple (sound familiar?) as Microsoft was taking share against the Mac. I felt that their products still had loyal supporters, that they were financially able to stay afloat even if they lost money, and with Steve Jobs return a couple years earlier could reinvent themselves. In addition I believed that they still understood consumers in terms of making technology easier to use.

Since then Apple has had periods of time repeatedly where the news flow was negative. Steve Jobs taking a medical leave. Steve Jobs death. Slowing this, slowing that. Even this year the stock went from $132 to the low 140's on slowing iPhone sales. But has my *fundamental* investment thesis changed (which is not a specific product thesis). No.

The second thing I would say is that there are times when Mr Market provides opportunity. In 2008/2009, all of the financial institutions were getting hammered. It was the end of the system, don't ya know. I worked in NYC in the financial district in the midst of it. While times were bad, I could see that when times get bad the strong can prevail at the cost of the weak. An example of this is JP Morgan Chase. Just a few years earlier they were worried about WaMu (Washington Mutual) opening funky new retail branches in NYC and taking market share from them. Yet Washington Mutual became insolvent in the financial crisis due to their aggressive mortgage underwriting, and in September 2008 their was essentially a bank run on it by depositors to the tune of $16.7 billion in withdraws in a 9 day period. The FDIC stepped in and eventually it was sold to JPM for $1.9 billion WITHOUT having to pick up WaMu's core banking business w/o the unsecured debt etc. (Disclosure: I own some JPM.)

While you are not JPM, you can also take advantage of severe downturns that take just about every stock down, regardless of how they will do in the long run. The strong will take advantage of the downturn. You can find high quality at a discount, but need to be prepared to buy when the news flow is extremely negative (and others are selling).

1) I believe you need to give investments "time". Most of my purchases are not for a quick trade (I do sometimes do this, but that is another topic). Rather, I am looking for something that will work out over years and as you can see from my holdings decades. This means that you need to be prepared for significant downturns in Mr. Market's appraisal of your holding, and be prepared to turn out negative news flow. Each of the securities I mentioned in the prior post have had time frames where their valuation significantly declined. Let's take Apple as an example. I bought it in 2000 primarily on these factors: It was cash rich. At the time, the stock was $19/share and they had $13 in cash. Many people were predicting the demise of Apple (sound familiar?) as Microsoft was taking share against the Mac. I felt that their products still had loyal supporters, that they were financially able to stay afloat even if they lost money, and with Steve Jobs return a couple years earlier could reinvent themselves. In addition I believed that they still understood consumers in terms of making technology easier to use.

Since then Apple has had periods of time repeatedly where the news flow was negative. Steve Jobs taking a medical leave. Steve Jobs death. Slowing this, slowing that. Even this year the stock went from $132 to the low 140's on slowing iPhone sales. But has my *fundamental* investment thesis changed (which is not a specific product thesis). No.

The second thing I would say is that there are times when Mr Market provides opportunity. In 2008/2009, all of the financial institutions were getting hammered. It was the end of the system, don't ya know. I worked in NYC in the financial district in the midst of it. While times were bad, I could see that when times get bad the strong can prevail at the cost of the weak. An example of this is JP Morgan Chase. Just a few years earlier they were worried about WaMu (Washington Mutual) opening funky new retail branches in NYC and taking market share from them. Yet Washington Mutual became insolvent in the financial crisis due to their aggressive mortgage underwriting, and in September 2008 their was essentially a bank run on it by depositors to the tune of $16.7 billion in withdraws in a 9 day period. The FDIC stepped in and eventually it was sold to JPM for $1.9 billion WITHOUT having to pick up WaMu's core banking business w/o the unsecured debt etc. (Disclosure: I own some JPM.)

While you are not JPM, you can also take advantage of severe downturns that take just about every stock down, regardless of how they will do in the long run. The strong will take advantage of the downturn. You can find high quality at a discount, but need to be prepared to buy when the news flow is extremely negative (and others are selling).

target2019

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Lots of Wisdom in your post. Most are thinking short, but I believe you need to evaluate each year, and go forward. Might have to cut a few companies who are "lost".While you are not JPM, you can also take advantage of severe downturns that take just about every stock down, regardless of how they will do in the long run. The strong will take advantage of the downturn. You can find high quality at a discount, but need to be prepared to buy when the news flow is extremely negative (and others are selling).

OldShooter

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

... Unlike OldShooter, I think it is possible for the individual investor to outperform the market ...

") Well, I'll plead innocent on that one.

Well, I'll plead innocent on that one.What I have said and what I believe is that all stock picking is a loser's game and the average result is inevitably less than the overall market performance. There are always funds and always individuals who outperform, just as there are always people who take more away from the casino than they brought.

All the data I am aware of, beginning 50 years ago (see post #14, above) supports this conclusion. I am as greedy as the next guy, so if there is statistical data out there that indicates a better strategy I'll be happy to change my opinion and jump on it. Here is a 6-minute discussion of the subject: https://famafrench.dimensional.com/videos/identifying-superior-managers.aspx

So is outperformance due to skill or just luck? Listen carefully to Dr. French.

Well, this sort of begs the question: "Why would we expect an individual to do better than professional fund managers and their legions of PhD quants.?"... but agree when it comes to actively managed mutual funds (in that it is extremely difficult for them to do so for a prolonged period of time). ...

I could argue either side of this. One one hand, individuals have a huge advantage due to their nimbleness. They can move in an out of their tiny positions without having any significant effect on the market. Any meaningful change in a position held by fund, OTOH, is almost certain to move the market in an unfavorable way due both to front-running and simply to microeconomics. Indivuals can also take meaningful positions (for them) in companies too small for funds to buy.

Individuals also have a cost advantage -- no salaries to pay, no offices to rent.

On the other hand, professionals have access to information with depth and speed that individuals simply cannot match. Both camps talk about seeking market inefficiencies, but in an inefficient market (Econ 101) he who has the most information wins.

But can there be significant market inefficiencies? With about 3600 stocks in the US market being chased by about 10,000 mutual funds, you have to believe that every stock is under several microscopes -- this is the recipe for an efficient market where future moves will be determined by future, currently unknown, events. So ... randomly.

Finally, there is the problem of what Nassim Taleb calls "silent evidence.*" Individual traders like @copyright1997reloaded post their wins and we can be happy for them. But the losers by and large do not post ---the silent evidence.

So bottom line, I am happy and not surprised that @copyright1997reloaded has been winning lately, but will point out that there is no way to determine whether this is due to skill or to luck. It's simply an anecdote and the plural of "anecdote" is not "data."

*More than two thousand years ago, the Roman orator, belletrist, thinker, Stoic, manipulator-politician, and (usually) virtuous gentleman, Marcus Tullius Cicero, presented the following story. One Diagoras, a nonbeliever in the gods, was shown painted tablets bearing the portraits of some worshippers who prayed, then survived a subsequent shipwreck. The implication was that praying protects you from drowning. Diagoras asked, “Where were the pictures of those who prayed, then drowned?”

The drowned worshippers, being dead, would have a lot of trouble advertising their experiences from the bottom of the sea. This can fool the casual observer into believing in miracles.

The drowned worshippers, being dead, would have a lot of trouble advertising their experiences from the bottom of the sea. This can fool the casual observer into believing in miracles.

SumDay

Thinks s/he gets paid by the post

- Joined

- Aug 9, 2012

- Messages

- 1,862

The point of my brief answers is there are no short cuts that you’ll find on this thread. Many on this forum are great at saving and investing in low cost mutual funds and setting up asset allocations based on their goals and needs. They are great at planning and budgeting, and most importantly, living below their means. People here can help you with these things.

Exactly. I learned so much here about asset allocation, rebalancing, etc., and it's kind of second nature for me (not that I'm as wise as most here, but I'm learning). I made it to retirement without owning any individual stocks. I can't imagine climbing that learning curve for picking individual stocks. I'm retired and that isn't even on the list of top 100 things I want to do with all my newfound free time.

That said, I hope you make a bazillion bucks. Seriously.

copyright1997reloaded

Thinks s/he gets paid by the post

What I have said and what I believe is that all stock picking is a loser's game and the average result is inevitably less than the overall market performance. There are always funds and always individuals who outperform, just as there are always people who take more away from the casino than they brought.

I would agree that the typical or average investor will under-perform passive index investing for a variety of reasons. Economic research has shown that people quite frequently show emotional response which can result in non-optimal outcomes. Many are trend following, and will dump securities at the worst possible time and buy securities near the peak. This is the essence of the madness of crowds. This is just one reason why the average result suffers. Another factor is the lack of fundamental analysis. Many investors have no ability to analyze a balance sheet for risk or even to understand something as basic as a P/E ratio. For the vast majority of people who I meet who ask me for advice, I simply tell them to stick with low-cost passively managed index funds.

OK, I listened to it. Again, I am not suggesting the use of actively managed mutual funds, which to me are to be avoided for the reasons discussed in the video. In addition, because they need to chase money, they are frequently obsessed with short term results (which by the way is an advantage I have in my picks, i.e. to find companies being sold off because of mutual fund quarterly or year end reporting).All the data I am aware of, beginning 50 years ago (see post #14, above) supports this conclusion. I am as greedy as the next guy, so if there is statistical data out there that indicates a better strategy I'll be happy to change my opinion and jump on it. Here is a 6-minute discussion of the subject: https://famafrench.dimensional.com/videos/identifying-superior-managers.aspx

So is outperformance due to skill or just luck? Listen carefully to Dr. French.

You mention some of the reasons. My individual purchases or sales don't move the market or the security in any significant fashion. I have no salary to pay, or advertising to do. More importantly, I don't need to worry about quarterly results and whether I will get a bonus as a result of outperforming that quarter.Well, this sort of begs the question: "Why would we expect an individual to do better than professional fund managers and their legions of PhD quants.?"

I could argue either side of this. One one hand, individuals have a huge advantage due to their nimbleness. They can move in an out of their tiny positions without having any significant effect on the market. Any meaningful change in a position held by fund, OTOH, is almost certain to move the market in an unfavorable way due both to front-running and simply to microeconomics. Indivuals can also take meaningful positions (for them) in companies too small for funds to buy.

Individuals also have a cost advantage -- no salaries to pay, no offices to rent.

On the other hand, professionals have access to information with depth and speed that individuals simply cannot match. Both camps talk about seeking market inefficiencies, but in an inefficient market (Econ 101) he who has the most information wins.

But can there be significant market inefficiencies? With about 3600 stocks in the US market being chased by about 10,000 mutual funds, you have to believe that every stock is under several microscopes -- this is the recipe for an efficient market where future moves will be determined by future, currently unknown, events. So ... randomly.

You've mentioned the 10K mutual funds and 3600 stocks before, and I've seen it discussed in other places as to why it makes stock picking impossible. But according to Zack's, a Multex study showed that of 8911 companies traded in the USA, there was Analyst coverage of only 3100 of these. Yes, I know Analyst coverage and Mutual Fund holding isn't the same thing - but I believe the same phenomenon occurs with actively managed funds as Analysts - trend following and a tendency to bunch into the same crowded investments.

Finally, there is the problem of what Nassim Taleb calls "silent evidence.*" Individual traders like @copyright1997reloaded post their wins and we can be happy for them. But the losers by and large do not post ---the silent evidence.

So bottom line, I am happy and not surprised that @copyright1997reloaded has been winning lately, but will point out that there is no way to determine whether this is due to skill or to luck. It's simply an anecdote and the plural of "anecdote" is not "data."*More than two thousand years ago, the Roman orator, belletrist, thinker, Stoic, manipulator-politician, and (usually) virtuous gentleman, Marcus Tullius Cicero, presented the following story. One Diagoras, a nonbeliever in the gods, was shown painted tablets bearing the portraits of some worshippers who prayed, then survived a subsequent shipwreck. The implication was that praying protects you from drowning. Diagoras asked, “Where were the pictures of those who prayed, then drowned?”

The drowned worshippers, being dead, would have a lot of trouble advertising their experiences from the bottom of the sea. This can fool the casual observer into believing in miracles.

Can't agree more. You (or the OP) have no idea of whether I am just lucky. Even I would be the first to state that I have about 50% of my net worth in passively managed index funds. I'm also not sitting on an Island with my endless wealth (although I'm pretty happy about where I am wealth wise). While I do stock picking, I am also financially conservative, run with a high cash position, and believe strongly in hedging ones bets.

But here we are on the stocking picking portion of the site, where us lucky or stupid or whatever individuals hang out and where for some strange reason you also like to hang out.

(Not being nasty here, just trying to get you to smile.) The OP asked about how to go about stock picking. Your answer is "don't". My answer is more like "It's hard, It takes effort, most people are unable to do so or unwilling to do what is required...but if you really, really want to then here are some of the things to think about".OldShooter

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Yes. That's also an advantage you have. Another one is that you don't have investors buying and selling all the time, which sometimes creates a "winner's curse" where a successful manager is buried in funds he can't invest as effectively as he could with a smaller portfolio last year. That's one theory to explain the abysmal manager persistence that S&P repeatedly reports.... More importantly, I don't need to worry about quarterly results and whether I will get a bonus as a result of outperforming that quarter. ...

The Sharpe paper states that actively managed funds are doomed to underperform to the extent of their costs, yet their underperformance is much worse than that. Some is hidden costs like market-moving trades but some is certainly due to the quarterly competitions and consequent portfolio window-dressing.

Maybe. My guess is that the missing 500 may be too small for a fund to invest in. Another: If I am a fund manager why would I be telling anyone what I am looking at? I think the "analyst coverage" number has more to do with brokerage house analysts but I have no facts to support this theory.... You've mentioned the 10K mutual funds and 3600 stocks before, and I've seen it discussed in other places as to why it makes stock picking impossible. But according to Zack's, a Multex study showed that of 8911 companies traded in the USA, there was Analyst coverage of only 3100 of these. Yes, I know Analyst coverage and Mutual Fund holding isn't the same thing - but I believe the same phenomenon occurs with actively managed funds as Analysts - trend following and a tendency to bunch into the same crowded investments. ...

... But here we are on the stocking picking portion of the site, where us lucky or stupid or whatever individuals hang out and where for some strange reason you also like to hang out.

Actually my bookmark is to "New Posts." Had you not told me, I would have needed to check to see where this thread lived.Running_Man

Thinks s/he gets paid by the post

- Joined

- Sep 25, 2006

- Messages

- 2,844

How to select stocks:

I pick stocks that by design are all dividend payers, from diversified industry groups and conservative by nature. The desire is to select stocks that should average to multiyear holdings. The basic rules for inclusion as a stock pick are (this is originally screening:

1) Must be rated in the top 25% of all Value Line stocks for Financial Strength and Safety – Goal is to have 67% picks with a Safety Rating of 1

2) Must have a sustained history of paying a dividend with a reliable record of dividend growth

3) Price Stability must be in the top 65% of all companies

4) Earnings Predictability must be in the top 65% of all companies

5) Should be in the top 45% of Value Lines Growth persistence

6) Timeliness of 3 or higher with a strong preference to stocks rated 1 or 2.

The advantage of the first selection screening process is you end with a selection of well financed companies, that are paying and can afford to increase the dividend and have a business model that does not have a large amount of variability in it's earnings.

Selling occurs :

1) Value Line reduces the Financial Strength at all or if Safety falls below 2. A cut in Safety ranking is a strong reason to sell a stock in and of itself but is not automatic.

2) Timeliness rating falls to 4 or lower.

3) Dividend is cut or expected increase unexpectedly does not occur.

4) Stock price has increased so much that the dividend yield is too low relative to other candidates. My general rule is for all dividend yields to exceed 1.5 percent and I would probably sell if yield fell below 1 percent due to a rising stock price and replace with a higher yielding selection. The end result of this strategy is an ever increasing much faster than inflation dividends received in a portfolio. I never allow taxes to affect any purchase or selling decision.

There are other subjective guidelines I follow to further decide whether a candidate is worthy of inclusion. The reason for most of the rules is to obtain a dividend stock that no matter what the market is doing will be bringing a dividend home that will grow in excess of inflation. All of the criteria are by using only the Value Line Survey, for myself I always check further by reading the most recent Edgar filings and trying to listen to management on a earnings call to see if their plans sound reasonable before investing any money.

In general, what ends up in the portfolio are stocks growing dividend 8-15% per year.

The advantage to using the Value Line Financial Strength and Safety Ratings are these are generated by Value Line and not under pressure by companies to raise or lower their ratings. A company that is eventually downgraded by S&P or Moody's for their bond rating will long before that occurs have a downgrade in Value line under Financial Strength or Safety, usually by quite a long time.

The idea is not to select the hottest stocks, but to select the safest growing companies and dividends the stock market has to offer.

For can simulate this for free using the Value Line Website and just select from the Dow Jones as a fun exercise. A perfect stock under the guidelines is Home Depot

https://research.valueline.com/api/report?documentID=2185-VL_20190322_VLIS_hd_X_01-6FLIP44R0H39V8P29EOIS8AJ9K

Likewise Cisco Systems:

https://research.valueline.com/api/report?documentID=2185-VL_20190315_VLIS_CSCO_692_01-1117BK1HOKGORNGMCUNMK0QKOA

Johnson & Johnson, though you would have to evaluate your personal Talc on this stock:

https://research.valueline.com/api/report?documentID=2185-VL_20190215_VLIS_JNJ_1564_01-3Q2CAID9N3B99UJ6GK41OBRA8I

What you have with a mix of these three companies would be stocks yielding around 2.8% a full percentage point ahead of the S&P500 and growing over 10 percent per year (expected doubling of dividends in 7 years. I would suggest one never invest more than 2 percent of a portfolio in any one individual stock.

A fine paying company like Verizon does NOT make the grade because of it's poor growth performance:

https://research.valueline.com/api/report?documentID=2185-VL_20190315_VLIS_VZ_3918_01-653O8GLVP4U1P70CRNG6UBI731 This is the same issue with Procter & Gamble and Walmart. Goldman Sachs & Apple don't meet criteria because of Timeliness of greater than 3 . Pfizer does not cut the grade because of the dividend cut in 2012. Visa a great company does not make the grade because of the low dividend % .

I pick stocks that by design are all dividend payers, from diversified industry groups and conservative by nature. The desire is to select stocks that should average to multiyear holdings. The basic rules for inclusion as a stock pick are (this is originally screening:

1) Must be rated in the top 25% of all Value Line stocks for Financial Strength and Safety – Goal is to have 67% picks with a Safety Rating of 1

2) Must have a sustained history of paying a dividend with a reliable record of dividend growth

3) Price Stability must be in the top 65% of all companies

4) Earnings Predictability must be in the top 65% of all companies

5) Should be in the top 45% of Value Lines Growth persistence

6) Timeliness of 3 or higher with a strong preference to stocks rated 1 or 2.

The advantage of the first selection screening process is you end with a selection of well financed companies, that are paying and can afford to increase the dividend and have a business model that does not have a large amount of variability in it's earnings.

Selling occurs :

1) Value Line reduces the Financial Strength at all or if Safety falls below 2. A cut in Safety ranking is a strong reason to sell a stock in and of itself but is not automatic.

2) Timeliness rating falls to 4 or lower.

3) Dividend is cut or expected increase unexpectedly does not occur.

4) Stock price has increased so much that the dividend yield is too low relative to other candidates. My general rule is for all dividend yields to exceed 1.5 percent and I would probably sell if yield fell below 1 percent due to a rising stock price and replace with a higher yielding selection. The end result of this strategy is an ever increasing much faster than inflation dividends received in a portfolio. I never allow taxes to affect any purchase or selling decision.

There are other subjective guidelines I follow to further decide whether a candidate is worthy of inclusion. The reason for most of the rules is to obtain a dividend stock that no matter what the market is doing will be bringing a dividend home that will grow in excess of inflation. All of the criteria are by using only the Value Line Survey, for myself I always check further by reading the most recent Edgar filings and trying to listen to management on a earnings call to see if their plans sound reasonable before investing any money.

In general, what ends up in the portfolio are stocks growing dividend 8-15% per year.

The advantage to using the Value Line Financial Strength and Safety Ratings are these are generated by Value Line and not under pressure by companies to raise or lower their ratings. A company that is eventually downgraded by S&P or Moody's for their bond rating will long before that occurs have a downgrade in Value line under Financial Strength or Safety, usually by quite a long time.

The idea is not to select the hottest stocks, but to select the safest growing companies and dividends the stock market has to offer.

For can simulate this for free using the Value Line Website and just select from the Dow Jones as a fun exercise. A perfect stock under the guidelines is Home Depot

https://research.valueline.com/api/report?documentID=2185-VL_20190322_VLIS_hd_X_01-6FLIP44R0H39V8P29EOIS8AJ9K

Likewise Cisco Systems:

https://research.valueline.com/api/report?documentID=2185-VL_20190315_VLIS_CSCO_692_01-1117BK1HOKGORNGMCUNMK0QKOA

Johnson & Johnson, though you would have to evaluate your personal Talc on this stock:

https://research.valueline.com/api/report?documentID=2185-VL_20190215_VLIS_JNJ_1564_01-3Q2CAID9N3B99UJ6GK41OBRA8I

What you have with a mix of these three companies would be stocks yielding around 2.8% a full percentage point ahead of the S&P500 and growing over 10 percent per year (expected doubling of dividends in 7 years. I would suggest one never invest more than 2 percent of a portfolio in any one individual stock.

A fine paying company like Verizon does NOT make the grade because of it's poor growth performance:

https://research.valueline.com/api/report?documentID=2185-VL_20190315_VLIS_VZ_3918_01-653O8GLVP4U1P70CRNG6UBI731 This is the same issue with Procter & Gamble and Walmart. Goldman Sachs & Apple don't meet criteria because of Timeliness of greater than 3 . Pfizer does not cut the grade because of the dividend cut in 2012. Visa a great company does not make the grade because of the low dividend % .

Last edited:

target2019

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Running_Man

Thinks s/he gets paid by the post

- Joined

- Sep 25, 2006

- Messages

- 2,844

Yea good job the North Americal Rockwell Coporation is now Rockwell Automation!

copyright1997reloaded

Thinks s/he gets paid by the post

Trivia of the day: I have a friend who worked for Value-Line (long ago) who introduced me to investing.

Similar threads

- Replies

- 24

- Views

- 2K

- Replies

- 51

- Views

- 5K

- Replies

- 70

- Views

- 5K

- Replies

- 19

- Views

- 536