SecondCor521

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Hi all,

I've been playing around with my RMD / QCD / conversion spreadsheets again. I am trying to figure out in some detail how I want to even out my tax bracket over time.

I am single and 52. I plan to 85; my life expectancy is probably there or a bit more if I'm reasonably lucky.

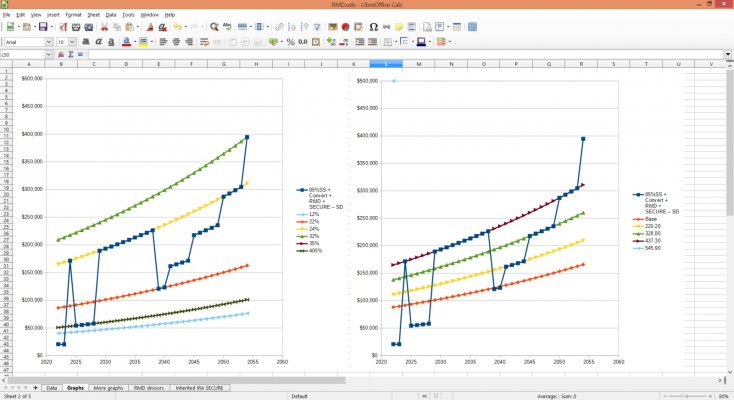

It appears to me that the first three IRMAA breakpoints occur between the 22% and 24% bracket for single filing status.

What I have discovered is that I am in the position where I get to choose whether to convert up to the top of the 22% or 24% bracket over the next several years. There is about a $90K difference between those two points.

Assume for the sake of discussion that I have the money to pay the conversion taxes in my taxable account.

1. I am seeing a seesaw effect where, if I convert to 24% instead of 22% in an earlier year (say 2027 when I'm 58), that whacks down my IRA balance to where I can have more later years in lower IRMAA brackets.

2. I also see a smaller seesaw effect where, if I convert up to the first or second IRMAA breakpoint a year or two earlier in my 70's, then I can avoid the third IRMAA breakpoint when I'm about 85.

I don't think it matters a whole lot, but any input on whether anyone "pays for" a longer period in a lower bracket later with an earlier Roth conversion "big gulp"? I'd appreciate thoughts on the tradeoffs.

The only things that have occurred to me is (a) IRMAA breakpoints don't matter before age 65 or so, (b) whether I have the money available to pay the taxes, (c) doing this seesaw now and converting to 24% early means I'm voluntarily paying more taxes now in an effort to potentially avoid some taxes later, (d) the growth that I'm projecting may not materialize.

So writing that last paragraph makes me think converting to 22% early on and then working my way in stair step fashion up the IRMAA tiers in my 70s and early 80's is the way to go.

I've been playing around with my RMD / QCD / conversion spreadsheets again. I am trying to figure out in some detail how I want to even out my tax bracket over time.

I am single and 52. I plan to 85; my life expectancy is probably there or a bit more if I'm reasonably lucky.

It appears to me that the first three IRMAA breakpoints occur between the 22% and 24% bracket for single filing status.

What I have discovered is that I am in the position where I get to choose whether to convert up to the top of the 22% or 24% bracket over the next several years. There is about a $90K difference between those two points.

Assume for the sake of discussion that I have the money to pay the conversion taxes in my taxable account.

1. I am seeing a seesaw effect where, if I convert to 24% instead of 22% in an earlier year (say 2027 when I'm 58), that whacks down my IRA balance to where I can have more later years in lower IRMAA brackets.

2. I also see a smaller seesaw effect where, if I convert up to the first or second IRMAA breakpoint a year or two earlier in my 70's, then I can avoid the third IRMAA breakpoint when I'm about 85.

I don't think it matters a whole lot, but any input on whether anyone "pays for" a longer period in a lower bracket later with an earlier Roth conversion "big gulp"? I'd appreciate thoughts on the tradeoffs.

The only things that have occurred to me is (a) IRMAA breakpoints don't matter before age 65 or so, (b) whether I have the money available to pay the taxes, (c) doing this seesaw now and converting to 24% early means I'm voluntarily paying more taxes now in an effort to potentially avoid some taxes later, (d) the growth that I'm projecting may not materialize.

So writing that last paragraph makes me think converting to 22% early on and then working my way in stair step fashion up the IRMAA tiers in my 70s and early 80's is the way to go.

")