audreyh1

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

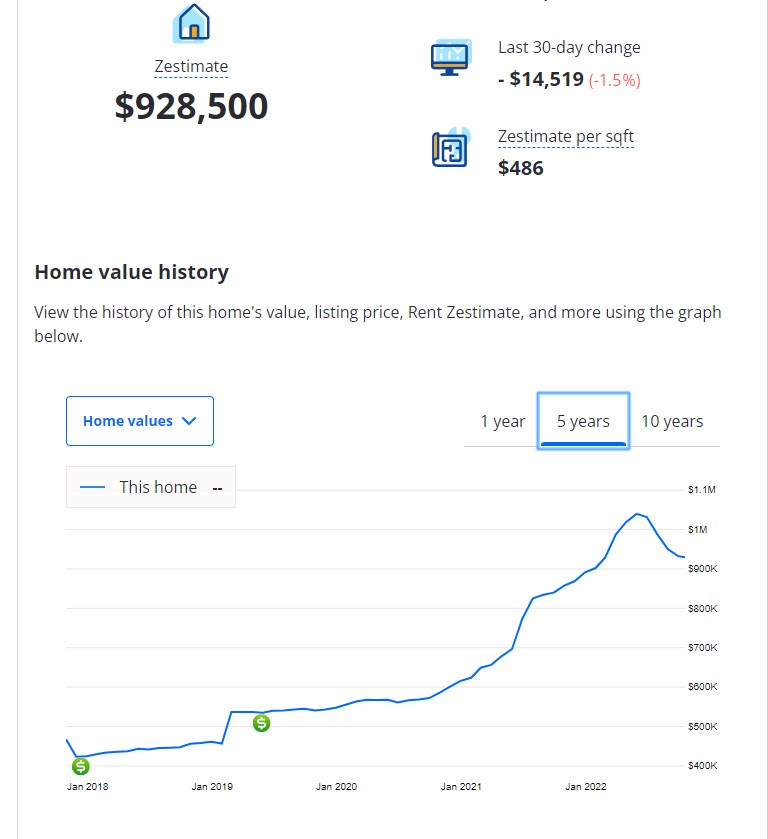

Well if no new inventory is becoming available, wouldn’t that support prices?

Well if no new inventory is becoming available, wouldn’t that support prices?

I just recently learned that "most" mortgages in Canada are 5-year variable rate, and that all mortgages are limited to 5 years (i.e. have to be renewed).

Also that in Canada, it has one of the highest real estate as a percentage of GDP figures.

As the Canadian central bank (BOC) raises rates, some of these mortgages (variable) no longer reflect any principal payment (due to increased interest cost) and thus have to have a higher payment amount.

The above, along with the huge run up in prices in Canada over the last n years, sounds like a big-time issue coming down the road (ala USA ARMs of 2008).

Are there any Canadian folks on here that can comment on this?

Wait to buy until mid 2023..I've been looking for a house in the Greater Atlanta area for almost 3 months and the gauging is reversing big time. I saw a property early this week, that I might pay MAYBE $300-310K based on the condition. It was bought by Opendoor in early June for $332K and they made no improvements that I could see. They listed it for $385K in July. When I saw it this week, it was down to $363K. Today, it dropped another $9K. I'm in a good position in this higher interest rate market because after I take out a loan, I'll probably be paying it off in early 2024 when a few CDs mature. I would consider paying cash but so far, it looks like there is still no advantage for me to do that.

There is so much misinformation out there right now, the biggest one is that we have a long term supply shortage.My friend, a RE broker said this morning at coffee he has convinced his listing owners to drop prices if they want to sell. And he said no new inventory is becoming available.

We are setting records for active permits. The foreclosure moratorium is over and these will start appearing on the market.I don’t know what “no new inventory” meant in the previous comment, but I assume they were referring to new construction. I can only speak to my area. My DH works at a bank in the construction loan department. Builders were cranking out homes as fast as the could and selling them even faster. Sales have slowed significantly and builders aren’t building like they were.

There is so much misinformation out there right now, the biggest one is that we have a long term supply shortage.

No mortgage interest write offs in Canada either. From what I remember all mortgages I had when I was there were 5 years fixed, amortized over 30 years.

What this meant was when you take out a mortgage, you pay the 30 year rate at the time for a fixed period of 5 years. Then after 5 years it was readjusted to the 30 year rate for that time for the next 5 year period.

In our local market, I don't see that the bubble has burst, but it sure looks to be sleeping.

We saw a 10% spike between Jan-June, if people in our area just price it back to Jan and call the spike a fluke which it was, the houses are selling just fine.

Opendoor will bankrupt itself as even with a cooling market they again overpaid, priced up, sat on a property for over 3 months and then took a low ball offer which I think was $65k under what they bought it for. I have no idea how they get their market valuations but its so extremely flawed.

We have 8 existing homes for sale currently in our subdivision, 5 with offers, 2 overpriced by about $25k, and 1 that just reduced to the appropriate price and will hopefully get an offer this week.

They have 22 homes left to sell in our subdivision, they have all been spec homes, the big difference is that the ones at the height were upgraded to the hilt causing insane prices, the new ones are only modestly upgraded making it appear like the prices are dramatically reduced, but most of it is like not having the 3rd floor finished so reducing sq footage by 800-1000 sq ft, substituting out the quartz, hardwood floors, etc. Plus with vendor financing at 4.875% fixed 30 year rates being offered they have been able to keep people interested.

New construction, the builders that are mid project are building insanely fast to complete the homes they have. The builders that are starting projects have not built but switched to just doing all the infrastructure for the entire property first, clearing, grading, streets, etc. Most would start building the minute the first section is cleared but that isn't happening now. It makes sense as infrastructure will greatly increase the value of the property even without homes and if we ever hit a 2008, I've seen builders buy other properties like that and take over. Actually the home I bought in 2006 had 3 builders before that subdivision completed, the first 2 bankrupting.

). But it doesn't seem like houses are selling as fast as they were last year, there aren't many on the market, and asking prices are only a little higher or about the same.

). But it doesn't seem like houses are selling as fast as they were last year, there aren't many on the market, and asking prices are only a little higher or about the same.