Too much low coupon debt was issued since the end of 2020. You have to be crazy to buy 20-30 year corporate bonds with coupons in the 2-3% range. The treasuries and muni bonds issued during that period were even worse. Despite the discounts from par, those bonds are not investable. When the yield curve normalizes, those bonds will get clobbered once again. I would wait for higher coupon long duration bonds to be issued. Investing in the 1-5 year duration has been the smart play thus far and laddering though the year, if you are interested in cash flow and risk management. By laddering since June, I may have caught the peak rates with those 6.25-6.75% 5 year high grade corporates or 5 year 5% non-callable CD or I may not have. But I know that even the lowest yielding note that I bought this year carries a far higher coupon that what was available last year. Those who are holding out for higher yielding CDs are free to do so. This is what makes a market. They are certainly better off sitting in cash at 3.8% and rising than holding onto a bond fund that will continue to pay substandard yields and depreciate over time. We have had these fixed income market corrections in 2013, 2015, 2016, 2018, 2020 and now 2022 so why torture yourself with long durations unless you have reasonable coupons that can protect you on the downside. The frequency of these correction which is more than likely to continue, is the primary reason why I will shrink my ladder down from the current 8 years to 5 years. At one point my ladder extended out to 15 years with corporate notes. It makes no sense to do that while long term coupons remain low. This is also the reason why I don't hold investment grade preferred stocks that are perpetual. They go through repeated cycles of 20-30% or more drops as the funds dump them every time there is a rate hick up. Here is the reality of today's fixed income market:

1- Cash in a money market fund yields more than 90% of bond funds regardless of duration.

2- 1-5 year duration CDs, treasuries, corporates yield more than cash.

4- A 10 or 30 year treasury now yields less than cash in a money market.

3- The Fed will continue to raise rates into 2023 and hold into 2024

So when the Fed does start cutting rates, those long term yields will start to rise as the yield curve normalizes.

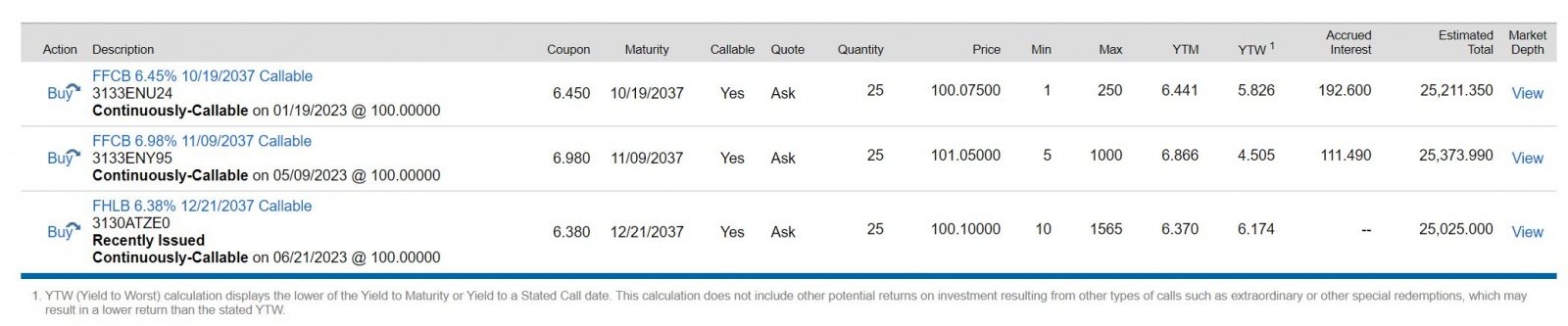

I bet you have a few sitting out there right now.

I bet you have a few sitting out there right now.