Looks good. How did you calculate the nominal yield is over 8% ?

YTM of 3.32% + expected inflation of 5%. The latter is my estimate.

Looks good. How did you calculate the nominal yield is over 8% ?

BTW, for the month of Nov, the unadjusted month-over-month CPI is -0.1%, annualized to -1.2%. So the nominal yield is only 2.12% during Jan 2023 (Nov 2022 CPI data is used in calculating the inflation adjustment for Jan 2023). Oh well ...YTM of 3.32% + expected inflation of 5%. The latter is my estimate.

This has been a very enlightening thread, thanks OP for starting it.

How do you all keep track of the maturities, interest rates, etc of your various rungs and ladders?

We are pretty rigorous: a single 5x8 ruled sheet from a notepad under my desk blotter. It has columns for purchase date, duration (13, 26 week), maturity date, amount of bill, what we paid, and interest rate.

In Quicken in the investing center we record the purchase and cost in the appropriate account, with cusip, and I enter the interest earned at maturity with cusip using the maturity date, so a future transaction.

I suspect there are much better ways to do this..

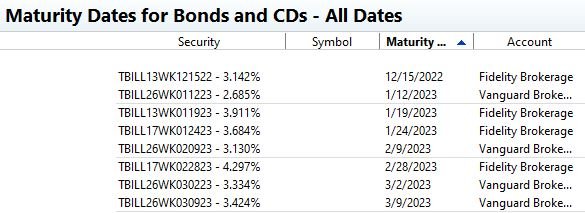

If you enter the "Maturity" and "Callable" information on the bond/treasury/CD, it really helps with standard quicken reports. Here's one I use which I find very useful. I also name all my Tbills and Notes using a name with their effective interest rate - it helps see the situation at a glance.

If you enter the "Maturity" and "Callable" information on the bond/treasury/CD, it really helps with standard quicken reports. Here's one I use which I find very useful. I also name all my Tbills and Notes using a name with their effective interest rate - it helps see the situation at a glance.

Just bought some TIPS (9128284H0) maturing on 4/15/2023 with YTM 3.32%. With expected inflation at ~5% for the next 4 months, the nominal yield is over 8%. Thought that's extremely good as a short term bond with virtually no risk.

YTM of 3.32% + expected inflation of 5%. The latter is my estimate.

We don't have anything between portfolio value and investment transactions. No Maturity and Callable for bond and CD spot jumping out at me. All a cunning plan to get us away from our quill-and eye-shade era 2006 non-subscription Quicken version.

Quicken user for 25+ years and never looked/saw this report. Vanguard has something similar in bond/cd tools.

thanks. david

")

That issue is showing on Fidelity as 3.567% YTM now. I don't know the intricacies of how TIPS work or if Fidelity ignores or includes the expected inflation adjustment. It just seems that 8% is too good to be true, so there's probably something amiss.

I had a rung on my Treasury ladder at Fido mature on 12/13/22. I went in to reinvest the funds in a 12/23 rung, but there were no available secondary market Treasuries at amounts less than $100,000 and some minimums were much higher. Is this normal? I bought the ladder(12 rungs, one per month) in October and had numerous options to choose from in 25k per rung amounts.

I tried to sell a t-bill maturing soon and had the same issue. Called the bond desk and they said that is normal for such short dated t-bills, I had to wait it out. It was nearly 250K but no market.

I had a rung on my Treasury ladder at Fido mature on 12/13/22. I went in to reinvest the funds in a 12/23 rung, but there were no available secondary market Treasuries at amounts less than $100,000 and some minimums were much higher. Is this normal? I bought the ladder(12 rungs, one per month) in October and had numerous options to choose from in 25k per rung amounts.

That issue is showing on Fidelity as 3.567% YTM now. I don't know the intricacies of how TIPS work or if Fidelity ignores or includes the expected inflation adjustment. It just seems that 8% is too good to be true, so there's probably something amiss.

Any TIPS people want to chime in?

Yes, VG and Fidelity have similar reports, automated. But what if you have both? I'm currently in the midst of getting away from VG so I have a bit of both. This report really helps.

And calmloki, it is fine if you want to stay with old Quicken. I hold no judgements. DYI with paper still works. Seriously. I honestly don't mind paying for Quicken. I also don't buy a car every 2 years. So that money saved goes to the subscription, and, uh, eating.

Here's a look at the short end of my TBill ladder, to give you an idea of what the report shows. Shares and value are truncated as that is private (they are to the right, not shown here). I hope someone out there finds this helpful. I'm really trying to help. If not, then bah humbug.

In general, TIPS real yields go up when people expect deflation, so with short term rates higher, that indicate general concerns about short term deflation. TIPS' principals adjust downward with deflation, so if you buy a 6 month TIPS on the secondary market with accumulated inflation, the principal might adjust downward prior to maturity and be redeemed for less than what you paid. Deflation on the principal will cut into that 3.567% real yield. Shorter terms TIPS on the secondary market are a bit of a gamble right now with a possible recession looming and the Fed's interest rate hikes kicking into gear. .

Quicken user for 25+ years and never looked/saw this report.

thanks. david

This has been a very enlightening thread, thanks OP for starting it.

How do you all keep track of the maturities, interest rates, etc of your various rungs and ladders?

But wouldn't inflation have to be negative and not just lower in order for a downward principal adjustment? I'm skeptical well ever get that low but I guess it is possible.

Has it ever happened? If so, when?

I had a rung on my Treasury ladder at Fido mature on 12/13/22. I went in to reinvest the funds in a 12/23 rung, but there were no available secondary market Treasuries at amounts less than $100,000 and some minimums were much higher. Is this normal? I bought the ladder(12 rungs, one per month) in October and had numerous options to choose from in 25k per rung amounts.

Thanks. Sorry, I didn't want to debate quicken versions.And you are being of help - caused me to go a-searching in our 2006 Quicken for something similar, and not finding it. What year Quicken are you using? Takes effort to change what is already set up, but we manually enter all our stock and bank transactions rather than having Quicken download them - don't even think our version will or it could screw up many years of history if it did. So we keep on maybe doing more work than necessary. For real though, many thanks - if we don't see the possibilities then we never change.

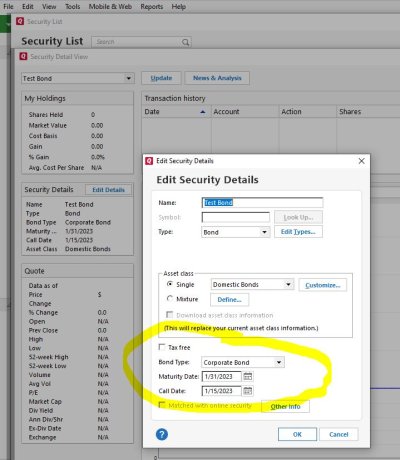

I ran the Quicken report @JoeWras mentioned, and lo and behold it worked! What's odd is that in the CD/Bond "edit" screen I don't see a place to enter the maturity date. It's included in the Security Name (along with the interest rate) that was downloaded from Fidelity. So Quicken must be deriving the date from that or some other datum provided in the background by Fidelity.

Ages ago when I last input a CD bought at my credit union I entered it manually. IIR Quicken had me create a new asset account for it. But maybe that was because I just had basic Quicken, not premium.

Lots of Quicken investing features I need to learn how to use

Bond inventory for CDs/Ts/GSEs is getting sucked up faster than a plate of spaghetti. The whales are taking the low coupons hoping for capital appreciation as rates drop. Retail is taking all the higher coupons before rates drop.

Hmm. I thought the max available and min in parentheses was the parameters I had to deal with. You are saying I can put in a higher bid on the depth of book page?Did you click the "depth of book" icon? The quotes shown on the main page are the lowest price/highest yield available for that particular issue. If you click "depth of book" you should see there are various lower minimum quantities available. The lower minimums are slightly higher price/lower yield. I've never seen a treasury that did not have a minimum of one bond available. I see a treasury that matures 12/15/23 with a minimum of one bond that yields 4.524. The best yield is 4.526 for a minimum of 500K