Hi all, first post here but have been working on early retirement for a number of years now.

I'm looking to retire at age 40 in 2026. This gives me 22 years until I can collect my estimated social security check of $1,500/month at age 62. I've been thinking: wouldn't it be nice if I could start collecting at age 40 to reduce sequence of returns risk?

I've been working on building out a treasury/CD ladder for the first 3 years of retirement, but this post https://tipswatch.com/2023/06/26/can-we-build-a-better-tips-etf/ got me thinking: why not build a 22 year TIPS ladder and have a "guaranteed" $1,500/month for life so that my SS kicks in just as my TIPS ladder expires?

Using tipsladder.com I created a 2026-2047 ladder that pays out $18k/year, total cost is $321,853. Supposing this purchase come from a portfolio of $1m, this leaves $678,147 for a 70/30 mix.

My expenses run about $35k/year, so after the $18k reduction from TIPS/SS this is reduced to $17k/year which is covered at a very conservative 2.5% withdrawal rate. Targeting 4% withdrawal rate would mean I could technically pull the plug at $746,853 (25x17,000+321,853)

I'm thinking this is a better option than buying a traditional annuity for 2 reasons:

1. I get inflation adjusted payments

2. I don't rely on a single company not going bankrupt

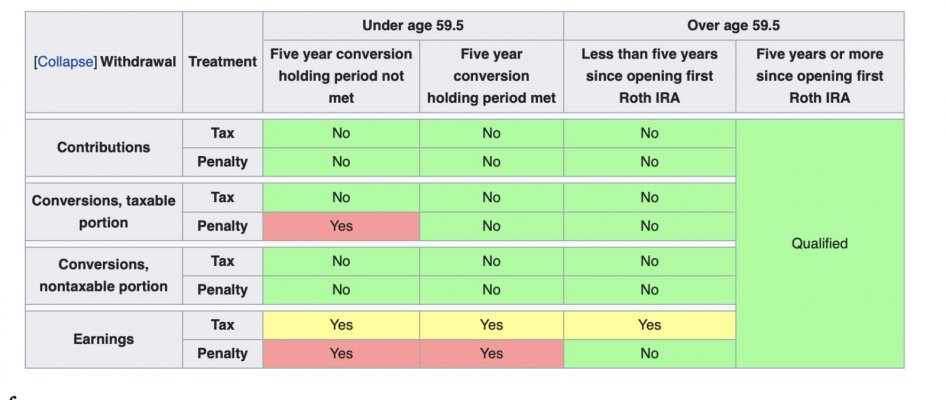

I'm wondering does anyone have thoughts on this strategy or is anyone doing it? The taxation of a TIPS ladder like this is a little fuzzy to me, but presumably it would be best in a tax advantaged account (in my case, it would be in a Roth IRA)

Thanks in advance!

I'm looking to retire at age 40 in 2026. This gives me 22 years until I can collect my estimated social security check of $1,500/month at age 62. I've been thinking: wouldn't it be nice if I could start collecting at age 40 to reduce sequence of returns risk?

I've been working on building out a treasury/CD ladder for the first 3 years of retirement, but this post https://tipswatch.com/2023/06/26/can-we-build-a-better-tips-etf/ got me thinking: why not build a 22 year TIPS ladder and have a "guaranteed" $1,500/month for life so that my SS kicks in just as my TIPS ladder expires?

Using tipsladder.com I created a 2026-2047 ladder that pays out $18k/year, total cost is $321,853. Supposing this purchase come from a portfolio of $1m, this leaves $678,147 for a 70/30 mix.

My expenses run about $35k/year, so after the $18k reduction from TIPS/SS this is reduced to $17k/year which is covered at a very conservative 2.5% withdrawal rate. Targeting 4% withdrawal rate would mean I could technically pull the plug at $746,853 (25x17,000+321,853)

I'm thinking this is a better option than buying a traditional annuity for 2 reasons:

1. I get inflation adjusted payments

2. I don't rely on a single company not going bankrupt

I'm wondering does anyone have thoughts on this strategy or is anyone doing it? The taxation of a TIPS ladder like this is a little fuzzy to me, but presumably it would be best in a tax advantaged account (in my case, it would be in a Roth IRA)

Thanks in advance!