jasonfreedom

Dryer sheet aficionado

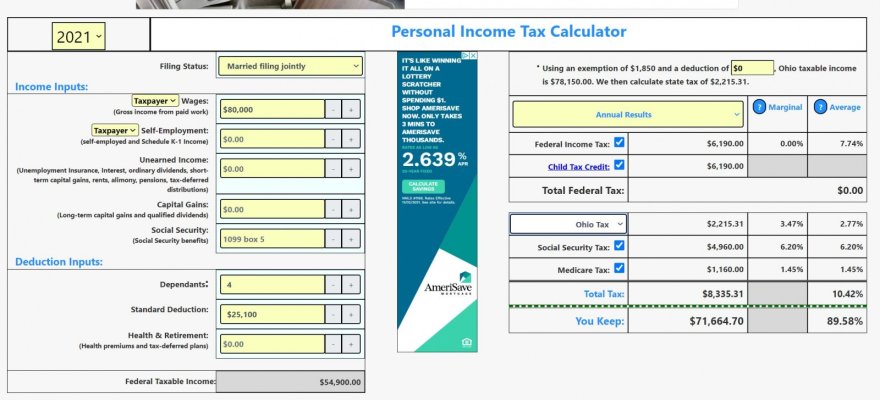

If you have 4 children, you probably don't have a whole lot of time to research investing. ")

The safest, least time required, time-honored investment is an S&P 500 index fund, with low cost basis. Vanguard and Fidelity are my favorites.

If you DO have time to research investments, pick one vehicle and learn everything about it. Right now I am interested in crypto - a controversial choice. Real Estate is a popular option. Stay away from day-trading, forex, commodities, and anything uber speculative. You're not likely to beat professional money managers, or the S&P 500, in trading stocks - unless you apprenticed under Ben Graham or somebody. But that leads me to...

Find a mentor. I cannot stress this enough. I have a crypto mentor, a kid who is MUCH younger than me. I don't pay him, but I've earned his attention because of how seriously I take his advice (and also I give him findings from my own research). VERY IMPORTANT - a real mentor will not charge you money. Any "wealth coach" who charges $200 per hour is a fraud. A real mentor is already a multi-millionaire and will help you because he/she wants to, not because they need another client.

Lastly, it's a marathon not a sprint. You're unlikely to go from 0-$10 Million in 6 months. Even the cockiest crypto kid I ever met (not my mentor), took 3 years to accumulate $5 million. And he got lucky. Can you see sticking with this avocation for at least 10 years. If not...you'll hate it.

My personal favorite investing mindset book is The Millionaire Next Door.

But others here probably have better advice than me.

The safest, least time required, time-honored investment is an S&P 500 index fund, with low cost basis. Vanguard and Fidelity are my favorites.

If you DO have time to research investments, pick one vehicle and learn everything about it. Right now I am interested in crypto - a controversial choice. Real Estate is a popular option. Stay away from day-trading, forex, commodities, and anything uber speculative. You're not likely to beat professional money managers, or the S&P 500, in trading stocks - unless you apprenticed under Ben Graham or somebody. But that leads me to...

Find a mentor. I cannot stress this enough. I have a crypto mentor, a kid who is MUCH younger than me.

I don't pay him, but I've earned his attention because of how seriously I take his advice (and also I give him findings from my own research). VERY IMPORTANT - a real mentor will not charge you money. Any "wealth coach" who charges $200 per hour is a fraud. A real mentor is already a multi-millionaire and will help you because he/she wants to, not because they need another client.Lastly, it's a marathon not a sprint. You're unlikely to go from 0-$10 Million in 6 months. Even the cockiest crypto kid I ever met (not my mentor), took 3 years to accumulate $5 million. And he got lucky. Can you see sticking with this avocation for at least 10 years. If not...you'll hate it.

My personal favorite investing mindset book is The Millionaire Next Door.

But others here probably have better advice than me.