Another Reader

Thinks s/he gets paid by the post

- Joined

- Jan 6, 2013

- Messages

- 3,413

It depends .... 2010 was a great year to buy a place

If you had a decent income and could get a mortgage, yes.

It depends .... 2010 was a great year to buy a place

Kids did. Every cloud has a silver liningIf you had a decent income and could get a mortgage, yes.

It was possible when you could buy a house at an affordable price. If I had not bought my first house in San Jose in 1984, I would not be living in the Bay Area today. It takes two good incomes to afford anywhere closer in than Stockton now.

It depends .... 2010 was a great year to buy a place

That's great, if you have enough assets and know exactly when you're going to die.Agree, I've always told my Mom that my ideal would be for her to figure out how to spend her very last penny with her very last breath i.e. not to hold back in any of her enjoyment over any desire to leave an inheritance.

Well said.I read the article but it doesn't seem to apply to me or my kids (or even grandkids starting to invest as they attend college with minimal loans). Just another "the sky is falling" dribble.

It's not easy .... no one said it was. It involves decades (most likely 2) of thinking outside the box and living below your means. It involves covering your bases and building up wealth while minimizing expenses. Investing in more than one stream whether that includes property, stock market, staying in military / government.

Recognizing a fire sale and constantly CONSTANTLY sticking to a plan even when everyone else says the sky is falling

How did he generate the $200K/yr income? By expecting a 10% stock return from a $2M portfolio?

And even though he lives in an expensive location, how does he spend $200K eating tilapia, dining at In N' Out Burger, and driving his car to the ground as he said?

I learned of the Financial Samurai from this forum, and not familiar with his story.

How did he generate the $200K/yr income? By expecting a 10% stock return from a $2M portfolio?

This person should not be giving out financial advice if he's unable to make his situation work without heading back to the workforce.

+1

Income and return should be two different things. My portfolio spits out 12% some good years but that is not my 'spendable' income.

Agreed. I'm not his target audience I'm sure. He's smart, worked in investment banking for many years, he's young, he wants to stay in SF (can't disagree with that in any way.. It's a great city) and he's willing to put up the money to live there.I’m not Financial Samurai’s defender or, actually, even one of his regular readers. But, he is certainly not the poster child of this thread: A Painful Unwinding of the FIRE Movement. A quick read of his blog reveals financial savvy and a thoughtful process of evaluating investments, risk & income, with FIRE as a goal. I’ll be the first to admit that it’s different than us but, that doesn’t make it wrong. In fact, when broken down to its essence, his approach is somewhat mainstream IMO (see below); the primary differences being that it’s with big #s (hey, it’s SF!), a high-ish end lifestyle and, he moves his $$$ around more than I care to.

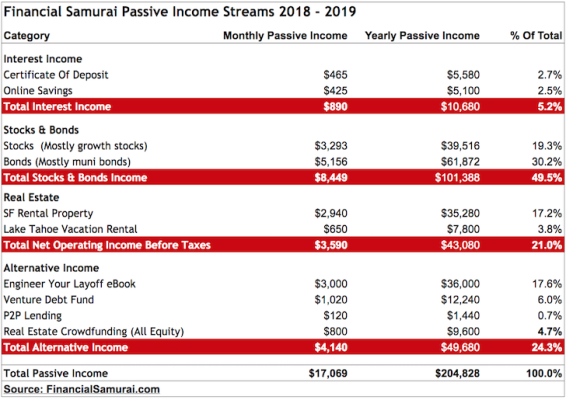

Annual Income (All #s ~): $200k

- Work (blog, consulting, writing, etc.): $50k

- Rentals: $40k (from ~$1.5-$2M in properties)

- Investments: $110k (from ~$1.5M investment portfolio)

Seems to me this dude & his DW are well on their way to their goals. Since he started his blog in 2009 and has carved his path in a long running bull market, it will be interesting to see how or if his life/approach changes in the next big downturn but, he seems well diversified and savvy enough to weather the storm.

I’m not Financial Samurai’s defender or, actually, even one of his regular readers. But, he is certainly not the poster child of this thread: A Painful Unwinding of the FIRE Movement. A quick read of his blog reveals financial savvy and a thoughtful process of evaluating investments, risk & income, with FIRE as a goal. I’ll be the first to admit that it’s different than us but, that doesn’t make it wrong. In fact, when broken down to its essence, his approach is somewhat mainstream IMO (see below); the primary differences being that it’s with big #s (hey, it’s SF!), a high-ish end lifestyle and, he moves his $$$ around more than I care to.

Annual Income (All #s ~): $200k

- Work (blog, consulting, writing, etc.): $50k

- Rentals: $40k (from ~$1.5-$2M in properties)

- Investments: $110k (from ~$1.5M investment portfolio)

Seems to me this dude & his DW are well on their way to their goals. Since he started his blog in 2009 and has carved his path in a long running bull market, it will be interesting to see how or if his life/approach changes in the next big downturn but, he seems well diversified and savvy enough to weather the storm.

ETA: With a bit more perusing, I see that the income above is what he calls “passive income” (see below) and doesn’t include the income from his blog, which he says generates 1.2M views/mo. Using an example from his own website, that could generate ~$75k/mo. So, I’m sure his blog income is a big part of his financial picture. Even if it’s only 10% of that monthly income, it’s $90k/yr. Good work if you can get it.

Doubtful. Otherwise he would not be going back in to the workforce to make up for his DIRE situation. What this is all about is that he is not making ends meet with his situation today. If you roam around his website, you can see that it does not carry any advertising. If he does have over 1M views/month, maybe he should be looking at monetizing it more.

I actually do see one ad (rotating from advertiser to advertiser) on the right of his page, and another one at the bottom of the page. It’s pretty minimal compared to many sites but, seems to be advertising.

I only have one friend that inherited money. I am glad that my mom enjoyed herself and spent her money traveling and doing what she wanted to.

It gets better or worse depending on your sense of humor.

ETA: With a bit more perusing, I see that the income above is what he calls “passive income” (see below) and doesn’t include the income from his blog, which he says generates 1.2M views/mo. Using an example from his own website, that could generate ~$75k/mo. So, I’m sure his blog income is a big part of his financial picture. Even if it’s only 10% of that monthly income, it’s $90k/yr. Good work if you can get it.

Had a buddy who planned on a 12% YoY return. He was very disappointed YoY. I don't know where people get these numbers.

...

I'm a regular reader and know his story. I've commented about him before because I really respect what he's done. No affiliation whatsoever.

His total passive income is likely about the same as mine - near $400K gross. But my capital base took me over 30 years to accumulate to be in a position to generate that. He's done it in 20.

I think he's very smart and has done a tremendous job with his site, along with solid thinking in his real estate investments, the market, and his version of risk-free investments (MM and CDs).

His site is probably one of the most valuable personal finance sites on the net at the moment. Huge readership. He could monetize and check out tomorrow.

I’m not Financial Samurai’s defender or, actually, even one of his regular readers. But, he is certainly not the poster child of this thread: A Painful Unwinding of the FIRE Movement. A quick read of his blog reveals financial savvy and a thoughtful process of evaluating investments, risk & income, with FIRE as a goal. I’ll be the first to admit that it’s different than us but, that doesn’t make it wrong. In fact, when broken down to its essence, his approach is somewhat mainstream IMO (see below); the primary differences being that it’s with big #s (hey, it’s SF!), a high-ish end lifestyle and, he moves his $$$ around more than I care to.

Annual Income (All #s ~): $200k

- Work (blog, consulting, writing, etc.): $50k

- Rentals: $40k (from ~$1.5-$2M in properties)

- Investments: $110k (from ~$1.5M investment portfolio)

Seems to me this dude & his DW are well on their way to their goals. Since he started his blog in 2009 and has carved his path in a long running bull market, it will be interesting to see how or if his life/approach changes in the next big downturn but, he seems well diversified and savvy enough to weather the storm.

It's not that he feels that he has to spend that kind of money... He wants to. That's the lifestyle he wants to keep up, and more power to him [emoji4].Less than 1/3 of households in San Francisco have over $200K in income, and San Francisco is only 47 square miles. Most of the Bay Area metro area is in the surrounding suburbs where the COL of living is lower than SF the city.

Using the $300K numbers, $24K for daycare? Most families are only going to have day care expenses, if they even have any at all, for a relatively short period of time. San Francisco has the lowest percentage of kids of any major city. Many families with kids move out to the suburbs with good public schools and lower costs of living. Our kids went to either city sponsored or church preschools with reasonable prices and we were in baby sitting co-ops or simply traded off nights with friends for date nights out. And if you are FIREd you wouldn't need day care at all. $25K on groceries? Not if you shop at Amazon pantry and Costco, even less at the farmer's markets, outlet and abundant ethnic markets.

Payments on a Volvo SUV? Are Volvos middle class cars? How about paying cash for a slightly used Camry instead? That drops the expenses another $8.4K a year.

$200 for date nights? Sure it is easy to spend that but it is just as easy to spend close to zero with a free library event pass or free / discount event nights at one of the many museums.