OldShooter

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

@all4j, I'll address a couple of your points:

So, the short version, IMO is that your questions can't be answered. The good news, though, is that I can't remember variance risk to have been a consideration in any of the research or literature concerned with the random walk that makes index investing the winner.

If you're interested in logic and impartiality I'd be happy to PM you a list of references authored by experts whose bios you can check out in Wikipedia. You will also find many in the Nobel listings as well. Just let me know.

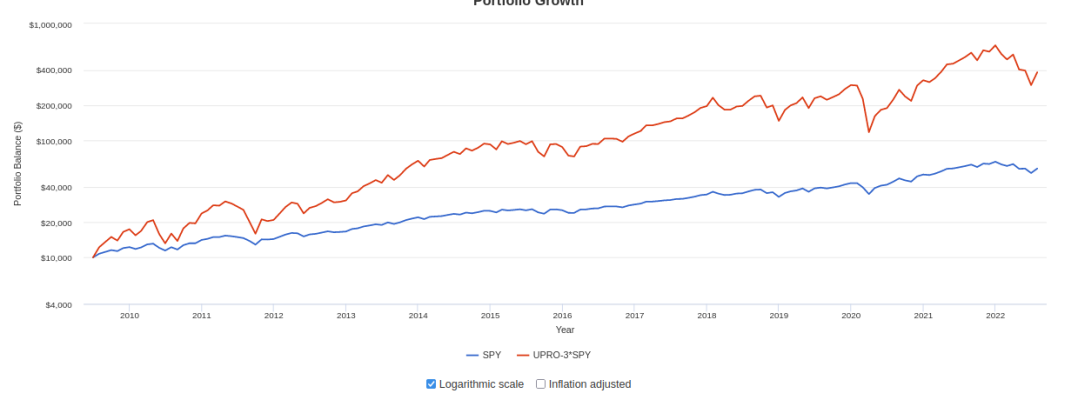

Unfortunately, the word "risk" is almost useless as a quantitative measure when applied to investing. In Markowitz' 1952 paper that was the foundation of Modern Portfolio Theory he very casually said the he was considering standard deviation (aka volatility) to be his measure of risk. With that approach, you can't strip risk from volatility because they are the same. Personally, as a long-term investor I am not concerned by volatility unless SORR raises its ugly head. Risk to me is GE, Enron, JDS Uniphase, Sears Holdings, etc. -- investments that permanently lose value. Further, volatility includes both "up" and "down" variations equally. I'm not sure many of us would consider an upward deviation of our investment to represent risk. For me overall, the concept just doesn't work.... I get a statement showing these results. It shows 4% more than the index fund -- it does not show adjusted returns stripping out risk from volatility. ...

So, the short version, IMO is that your questions can't be answered. The good news, though, is that I can't remember variance risk to have been a consideration in any of the research or literature concerned with the random walk that makes index investing the winner.

I'm not sure who you were painting with that brush, but I was trained as a scientist and engineer and have approached investment from a science mindset. All the technical papers, data, books, and studies I have found point to the random walk explanation that in turns leads one to indexing. I am as greedy as the next guy, however, so if scientifically credible results pointing to a better strtegy appear, I will be happy to jump towards it.... Arguments devolve into rationalizing a point of view, logic & impartiality to the side. ..I

If you're interested in logic and impartiality I'd be happy to PM you a list of references authored by experts whose bios you can check out in Wikipedia. You will also find many in the Nobel listings as well. Just let me know.

")