I kind of buzzed through this, so I think at least a few have reflected my response.

1) Ignoring SORR seems a bit of an ....... issue. (I have no doubt that 90-100% stock portfolios in the vast majority of cases will come out ahead. It is those 2-5 sequences that bother me, as well as remembering 2001-2002.) It's not the highest ending portfolio that I seek but relatively safe high withdrawal.

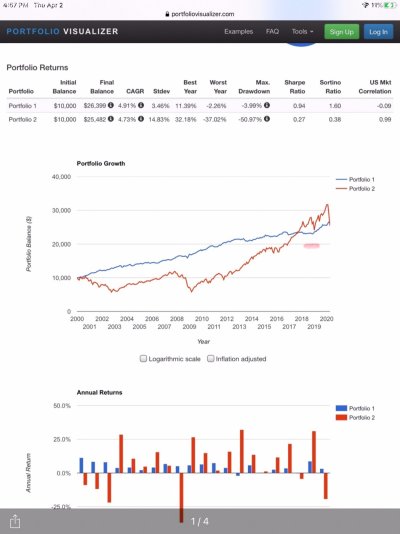

2) Every time the S&P has outperformed, I seem to recall these arguments, based on 5 or even 10 year outpeformance. I also recall that the outperformance tends to last a lot longer than one would think (in terms of relative pricing), but also that the S&P's outperformance can get destroyed quite quickly (looking forward in retrospect, hee!) and may not recover quickly (SORR).

3) Slowly and methodically scraping some gains into US value and international may not be not a completely stupid strategy, historically, emphasis historically. Maybe we are at that unusual golden turn in history where the S&P will always outperform, as many suggest here I seem to recall periods (after 2000) where the S&P did diddley squat, which is not an issue--unless all your funds are S&P or tech/large growth; then it sucks and can suck for quite a while. If you can tolerate sucking for 5-10 years, this may not be a bad thing.

4) This is not to suggest that an 90-100% S&P strategy should be abandoned, just that if you are looking at the last 10 years, you might want to consider a longer timespan if you think the last 7-10 year outperformance will continue ad infinitum.

Do I know when to optimally rebalance to international/value? Nope; I probably do it at the worst times, until in retrospect (like 2006 looking back), it looks pretty good.

Edit: And I think S&P is priced very richly at this point, similar to 2000. Can it continue to shoot up and outperform? Yes?

Can it continue another 5 years? Yes.

Will the pricing adjustment be brutal, if an when it comes? Probably, historically.

So if you are 90-100% S&P/US large growth just be sure you are strapped in and ready for the ride out of the chute, ala 2001, not 2020, although you have to stay on for longer than 8 seconds. Many of those here have withdrawal rates below 2%, so mathematically, this should not be an issue. If you are above 4%, it could be an issue, unless the recovery is sufficiently fast. If you are 15 years into retirement, it won't matter. I like to add these little caveats, because the answer will highly depend on your withdrawal rate, age, and other factors. I'm still 3.5 years from FSR age, which matters to me. If I were withdrawing 1.5-2% like many here, a 90-100% equity/large US growth would sound pretty good.