TromboneAl

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Jun 30, 2006

- Messages

- 12,880

When I rebalance, I'm considering consolidating some of our VG funds just to make things simpler.

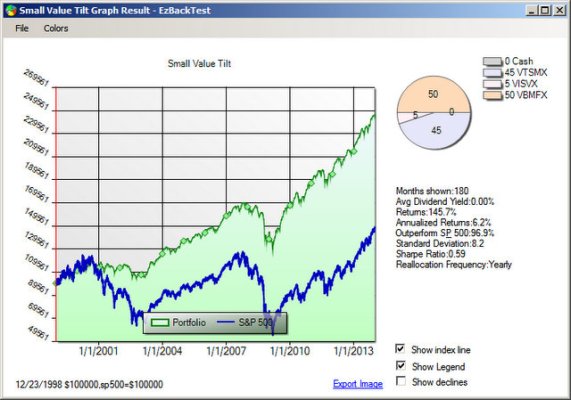

For example, the Vanguard "Portfolio Watch" has nagged me into having two small-cap funds (Small-cap Growth, and Small-cap Value) with a total of about 5% of our net worth in them.

One option would be to eliminate those. The disadvantage is that we'd be less diversified (almost no small-cap). The advantage is that I'd have two less funds to track, download data from, enter tax data from, etc.

We currently have 14 VG funds, partly because we need to segregate funds in my IRA, Lena's IRA, my Roth, Lena's Roth, Taxable account and HSA.

Is it silly to give up the diversification just to save me a little effort?

For example, the Vanguard "Portfolio Watch" has nagged me into having two small-cap funds (Small-cap Growth, and Small-cap Value) with a total of about 5% of our net worth in them.

One option would be to eliminate those. The disadvantage is that we'd be less diversified (almost no small-cap). The advantage is that I'd have two less funds to track, download data from, enter tax data from, etc.

We currently have 14 VG funds, partly because we need to segregate funds in my IRA, Lena's IRA, my Roth, Lena's Roth, Taxable account and HSA.

Is it silly to give up the diversification just to save me a little effort?