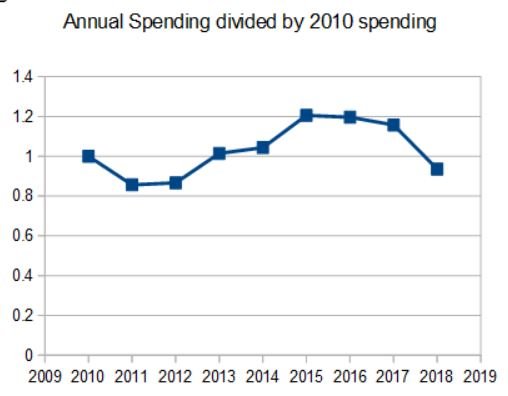

All the wisdom on this forum brings me to the question of portfolio longevity. I can hope for the best in the future, but what about those who survived the 2008 crash, dips in the past (15-20 years) and are doing just fine?

I can guess from a few posters but it would be interesting to see the numbers.

-At any point did you have to curb your spending?

-How did you adjust your portfolio during 2008-2012?

I tire of the hype in financial media about what to do next. Learning from the past is advantageous to the future (personal experiences, not graphs, calculators and tables).

I can guess from a few posters but it would be interesting to see the numbers.

-At any point did you have to curb your spending?

-How did you adjust your portfolio during 2008-2012?

I tire of the hype in financial media about what to do next. Learning from the past is advantageous to the future (personal experiences, not graphs, calculators and tables).

Last edited:

")

during the crash. My AA remained the same until all was recovered but I adjusted to a more conservative allocation afterward. I did buy a vacation condo in early 2014 and it has been a decent investment to this point.

during the crash. My AA remained the same until all was recovered but I adjusted to a more conservative allocation afterward. I did buy a vacation condo in early 2014 and it has been a decent investment to this point.