- Joined

- Nov 17, 2015

- Messages

- 13,980

3 years. Average recovery from a crash of most kinds, sleep-at-night, etc. Not really worried about leaving growth on the table for that amount. Also helps us manage when to take cap gains for the ACA.

Curious how you are getting 2.47% yield on cash. Are you talking CD's?

(3) Just to feel safe and secure - that you can sleep at night.

Retired 15 years ago at 48. Had a couple months expenses in cash, same as today, with all the rest in equities. As I have lived off the dividends, I saw no need for a cash cushion yielding almost nothing. No problems so far.

The other day a watched a video of a woman worth about 1.3M(100% stocks) with 25k in cash. I do not think that is enough cash how about you?

The other day a watched a video of a woman worth about 1.3M(100% stocks) with 25k in cash. I do not think that is enough cash how about you?

But does it make her nervous? If she didn't lose sleep over it during March 2020 she's at a good AA for her.That little would make me nervous.

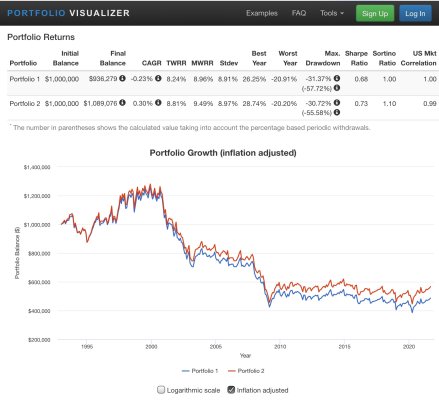

I thought about doing that. The only thing is in a bear that dividend payment might be a 50% loss on the money at times. With 100% stocks it can take about five years to recover from a bear. So for five years you might be pulling at a loss.

I am not quite sure what you mean that a dividend payment might be a 50% loss. The earnings and dividend flow increases each year (historically about 9% ave for me) regardless of what the stock price does (in my case -43% in 2008-2009, -53% in early 2020). Since this dividend flow is in excess of my spending, I just buy more stock with what is left over, meaning I benefit more when stock prices go down. This is why I find volatility exciting instead of terrifying.

I am still vulnerable to dividend cuts if a company runs into trouble, but the 3 I have been hit by (GGP, GE, KMI) were more than compensated for those years by increases by the rest of my portfolio.

I thought about doing that. The only thing is in a bear that dividend payment might be a 50% loss on the money at times. With 100% stocks it can take about five years to recover from a bear. So for five years you might be pulling at a loss.

Let say you put 100k in the s&p 500. A bear comes and it goes down 50%. The dividend of .6k is payed out. You are losing about .6k because if you left it in the market it would have time to go back up to 1.2k