If you are saying that you are going to do a roth conversion with the part of the RMD you don't need to spend, then I would be very careful. Your RMD must be withdrawn from your tax deferred account. You can use these dollars to pay the tax on a roth conversion, but you can't convert it into a roth. That would be seen as not taking your full RMD or as a new contribution (do you have employment income?) depending upon how you do it.

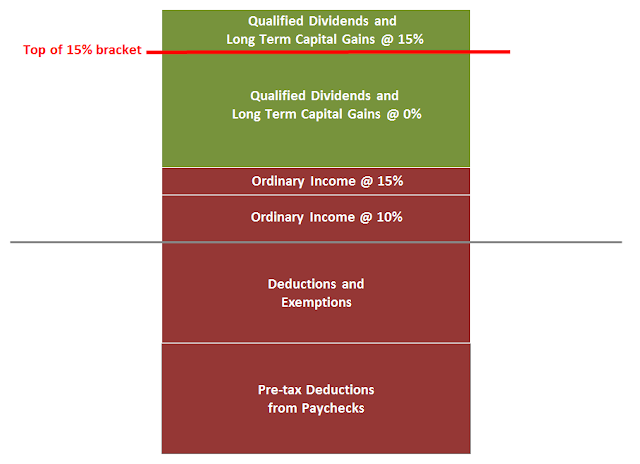

There is so much good information on this site. Remember the most important thing is to understand how these things effect you're situation. In this tread there were two type of tax graphs commonly used here: pb4uski's tax stack which most follows the tax brackets and the effective marginal (S.S.) where you effectively add $1 of ordinary income and see how the tax changes (effectively stick one dollar at the bottom of the pile and seeing the tax change). For stacks you may need to determine how much of things SS are taxable. If you are not looking at adding ordinary income to you taxable income, then the effective marginal rate may not be giving you good feed back.

Independent of these methods, if you focus on optimizing this year, you may create bigger tax problems in the long run. There is likely more more to be saved by determining the right tax diversification, conversion strategy, and withdraw strategy.