target2019

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

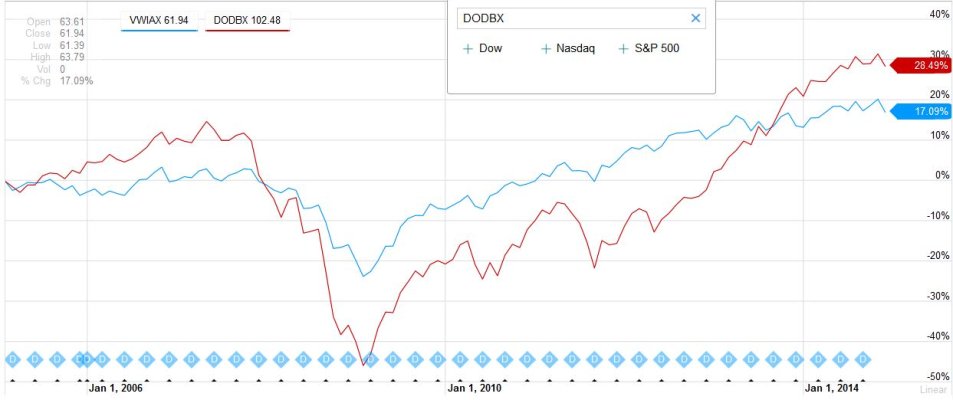

What I find to be interesting is that Wellesley is held in high regard, and it is actively managed. From the prospectus:

The investment seeks to provide long-term growth of income and a high and sustainable level of current income, along with moderate long-term capital appreciation. The fund invests approximately 60% to 65% of its assets in investment-grade corporate, U.S. Treasury, and government agency bonds, as well as mortgage-backed securities. The remaining 35% to 40% of fund assets are invested in common stocks of companies that have a history of above-average dividends or expectations of increasing dividends.

On other pages I found that the stock dividend is something like 3% compared to an S&P500 dividend of 2%. This Vanguard page will get you the complete list of stock holdings. Gives you an idea of how much research they put into the selections.

https://advisors.vanguard.com/VGApp...stments/portfoliodetails?fundId=0527#state=50

I think if you researched a few of the popular dividend ETFs, you'd find commonality with the lists of companies. But the percentages held would be different.

The investment seeks to provide long-term growth of income and a high and sustainable level of current income, along with moderate long-term capital appreciation. The fund invests approximately 60% to 65% of its assets in investment-grade corporate, U.S. Treasury, and government agency bonds, as well as mortgage-backed securities. The remaining 35% to 40% of fund assets are invested in common stocks of companies that have a history of above-average dividends or expectations of increasing dividends.

On other pages I found that the stock dividend is something like 3% compared to an S&P500 dividend of 2%. This Vanguard page will get you the complete list of stock holdings. Gives you an idea of how much research they put into the selections.

https://advisors.vanguard.com/VGApp...stments/portfoliodetails?fundId=0527#state=50

I think if you researched a few of the popular dividend ETFs, you'd find commonality with the lists of companies. But the percentages held would be different.

")