CincyDave

Thinks s/he gets paid by the post

Shouldn't this be moved to the Funny Joke thread?

Ha Ha, I suppose you're right

Shouldn't this be moved to the Funny Joke thread?

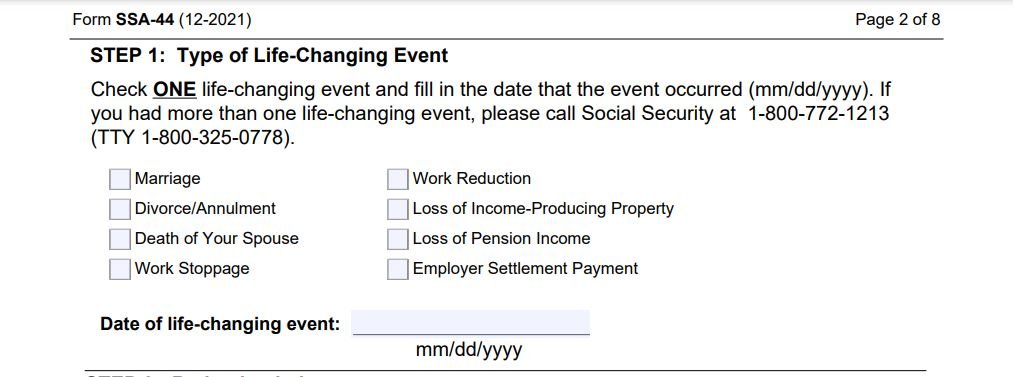

...There are 8 reasons that are acceptable for an appeal...

I'm a volunteer SHIP Medicare counselor and would like to offer a couple of thoughts about IRMAA appeals. My wife and I have helped 7 or 8 beneficiaries file appeals this year and every one was approved. The process is very straight forward and doesn't take much time.

There are 8 reasons that are acceptable for an appeal. It is simply a matter of checking a box on SSA form (SSA-44) that identifies the reason for the appeal accompanied by some form or supporting documentation. Then the applicant estimates the impact on current year income. It is a simple form.

I recommend that the application also include a straight forward and not overly complicated cover letter for the reviewer that clearly states what is happening.

The SSA-44, supporting documentation and cover letter are then mailed to the local SSA office. Turn around in our area is typically a month or two.

There is an excellent 8 minute video on you tube that explains the process. Search for "IRMAA Appeal".

Hi folks,

Turning 65 next year, 2023, and will be filing for Medicare.The wife still has a few years before she's eligible. I have a ton of questions on what "plans" to pick but that will be another post.

This post/thread is for "Income-related monthly adjustment amounts (IRMAAs) which are based on a person’s adjusted gross income and may affect their Medicare premiums. When a person makes more than the allowed income, Medicare adds a charge to the Part B premium, Part D (Medicare prescription drug coverage) premium, or both."

They look at your tax filings from 2 years ago to determine how much to increase your Medicare costs. In 2021 we sold the rental and paid ridiculous taxes both federal and state, at least for us.

So when I sign up for Medicare in 2023 they will look at the tax filings for the 2021 year, which is not our normal income, to determine if I exceed IRMAA's allowed income. I know for that year we do exceed the allowed income and will pay more for Medicare. Ouch

Any ideas on how I can have them look at another years' tax filings?

Can I petition Medicare on how to work for a fairer resolution?

Would they just use my income from the tax filing year?

How would they handle the capital gains on the sale of the rental, split it since the wife won't be filing?

I'm going crazywith all this.

I'm hoping someone on this sight has some insight on this issue.

Your "allowed income" terminology is a bit off.

So it's best to manage your AGI each year after 65 using Roth conversions so you don't get into the next higher IRMAA tier...

Did your friend also have one or more of the listed life changing events in the same year as the Roth conversion? I found someone who successfully appealed because they were also laid off in the year of the Roth conversion.A friend of mine appealed due to a large roth conversion, and despite that not being on the list of life changing events, his appeal was approved. Why not try appealing ? There is nothing to lose. All they can do is say no !

Velly intelesting...A friend of mine appealed due to a large roth conversion, and despite that not being on the list of life changing events, his appeal was approved. Why not try appealing ? There is nothing to lose. All they can do is say no !

I had a similar situation. We sold a rental property in 2020 and so our income was super high that year (plus lots of taxes!). Then, I retired in 2021 and so my income was much lower that year. "Stop Working" is one of the allowable exemptions and so I submitted form SSA-44 and requested they use 2021 instead of 2020. This was approved and they waived the IRMAA costs.

Any ideas on how I can have them look at another years' tax filings?

Can I petition Medicare on how to work for a fairer resolution?

Would they just use my income from the tax filing year?

Hi folks,

Turning 65 next year, 2023, and will be filing for Medicare

This post/thread is for "Income-related monthly adjustment amounts (IRMAAs) which are based on a person’s adjusted gross income and may affect their Medicare premiums. When a person makes more than the allowed income, Medicare adds a charge to the Part B premium, Part D (Medicare prescription drug coverage) premium, or both."

They look at your tax filings from 2 years ago to determine how much to increase your Medicare costs. In 2021 we sold the rental and paid ridiculous taxes both federal and state, at least for us.

So when I sign up for Medicare in 2023 they will look at the tax filings for the 2021 year, which is not our normal income, to determine if I exceed IRMAA's allowed income. I know for that year we do exceed the allowed income and will pay more for Medicare. Ouch

Any ideas on how I can have them look at another years' tax filings?

Can I petition Medicare on how to work for a fairer resolution?

Would they just use my income from the tax filing year?

How would they handle the capital gains on the sale of the rental, split it since the wife won't be filing?

I'm going crazy

I'm hoping someone on this sight has some insight on this issue.

OK. It's well documented that Roth conversions are NOT an accepted basis to avoid IRMAA penalties, clearly not a "life-changing event" - the question has been asked thousands of times. So I'm not going to bother since all our Fed agencies are understaffed and overwhelmed since the pandemic. Just try to talk with anyone at the IRS or TreasuryDirect...Hi Midpack. No, my friend did not have any other life changing events. He filed the appeal using the roth conversion reason and was successful. We are dealing with bureaucrats, so he may have just slipped through the cracks, but it is worth trying as the only downside is a no response.