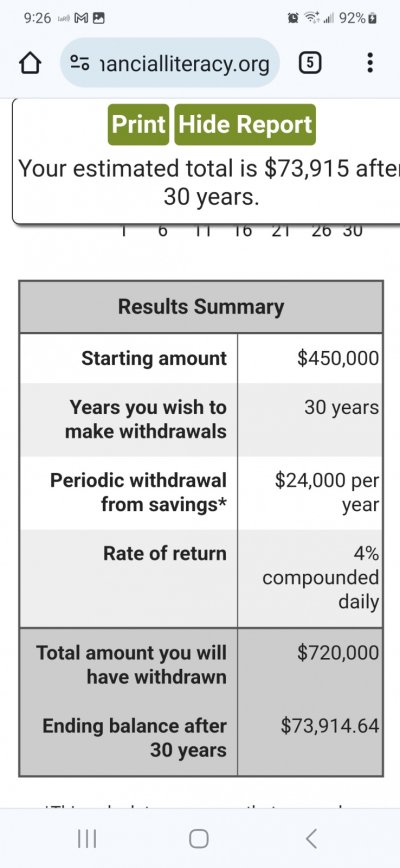

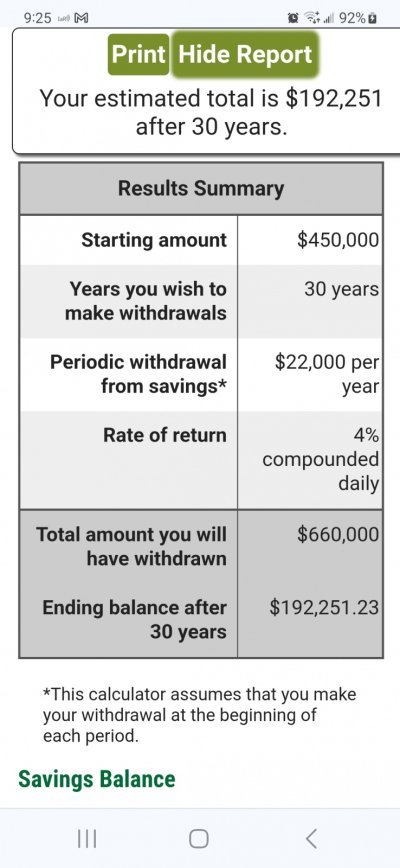

Ok, so is there a withdrawl calculator? One that I can imput an account, it will add the estimated intrest per year, and i will set the withdrawl rate. So it will let me see how many years I can pull from an account untill it goes dry? I can and have been doing long calculations on paper but its a pita, especially over like 30 years. And then changing the withdrawl rate and starting over. Can this be done in Fire Calc? I dont need all the other stuff just curious on one account.

Is there a withdrawal calculator?

- Thread starter Slim11

- Start date