ProGolferWannabe

Recycles dryer sheets

- Joined

- Jan 14, 2012

- Messages

- 141

Hi...was hoping I could get some thoughts on which pension option folks here would think would be the best choice for my wife when she retires early next year. She is is in good health, and when she retires she will be 58, so she will, hopefully, live a good long while.

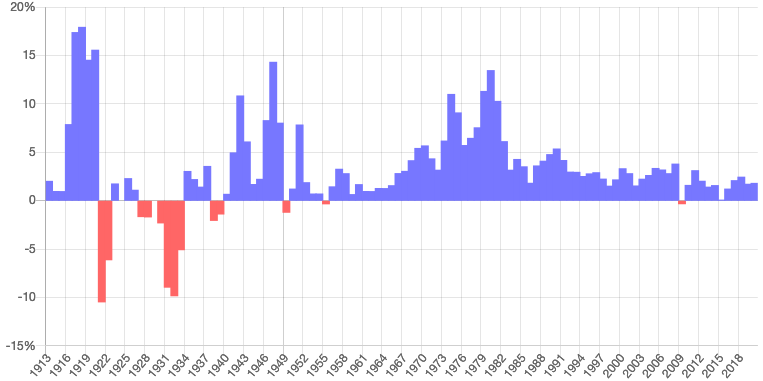

Option 1: She receives a fixed monthly amount until the January after her 62nd birthday, when the amount is fully adjusted by annual increase in the CPI-W. The amount cannot ever decrease if there were any deflation.

Option 2: She receives $193 more per month than option 1....$2318 more per year. That amount is also fixed until the January after her 62nd birthday, but the COLA adjustment works as follows:

If the CPI-W increase is between 0% and 2%, her pension is increases by the full CPI.

If the CPI-W increase is between 2% and 3%, her pension is increased by 2%. (Ex: CPI increases by 2.9%, she gets a 2% increase in her pension; CPI increases by 2.1% she gets a 2% increase in her pension.)

If the CPI-W increases by more than 3%, her pension is increased by the CPI-W minus 1%. (Ex 4.2% inflation translates into a 3.2% increase in pension.)

In Option 2, like Option 1, her pension can never be decreased if there is deflation.

Obviously, the more inflation we have, the better Option 2 is over an extended period of time. I guess the reduced initial pension for Option 2 is effectively the cost of insurance for fully protecting the real purchasing power of my wife's pension over her lifetime. We are pretty risk adverse, so like the idea of that protection, but we are wondering if the insurance is "fairly" priced.

Any perspective would be appreciated. Thanks.

Option 1: She receives a fixed monthly amount until the January after her 62nd birthday, when the amount is fully adjusted by annual increase in the CPI-W. The amount cannot ever decrease if there were any deflation.

Option 2: She receives $193 more per month than option 1....$2318 more per year. That amount is also fixed until the January after her 62nd birthday, but the COLA adjustment works as follows:

If the CPI-W increase is between 0% and 2%, her pension is increases by the full CPI.

If the CPI-W increase is between 2% and 3%, her pension is increased by 2%. (Ex: CPI increases by 2.9%, she gets a 2% increase in her pension; CPI increases by 2.1% she gets a 2% increase in her pension.)

If the CPI-W increases by more than 3%, her pension is increased by the CPI-W minus 1%. (Ex 4.2% inflation translates into a 3.2% increase in pension.)

In Option 2, like Option 1, her pension can never be decreased if there is deflation.

Obviously, the more inflation we have, the better Option 2 is over an extended period of time. I guess the reduced initial pension for Option 2 is effectively the cost of insurance for fully protecting the real purchasing power of my wife's pension over her lifetime. We are pretty risk adverse, so like the idea of that protection, but we are wondering if the insurance is "fairly" priced.

Any perspective would be appreciated. Thanks.