Like others have said, if you're reducing your equity exposure (changing AA) because you're at or near FI without the intent of increasing your equity exposure again 'when the market drops,' that's not unusual and it's not market timing per se. If you plan from the outset to increase your equity exposure later, you're in the realm of market timing. Or if you're planning on exiting equities altogether, you're market timing.

But it's your money - your future.

As for 'when to shift to a lower risk portfolio' there can be many reasons aside from market timing. It's not a stepwise, all or nothing proposition IMO. It's always made sense to me to optimize the risk I take, from another recent thread.

"Play around with FIRECALC" using the default 75:25 (or whatever you like) and "find the lowest portfolio amount that yields" whatever % you're comfortable with (ie, 95% works for me). If your portfolio is larger than that (hopefully), put the balance of your portfolio "someplace safe." 'You've won the game, why keep playing (with all your money)?' That's basically how I arrived at my AA and I will review where I stand every year or so, but not often.

For example, if you're comfortable with 75:25 and your portfolio is 1.5 times the amount for FI (just to make the example math easy) call it $1.5M, you've won the game you might consider putting the excess in safer investments. For the first $1MM that provides your SWR, you'd put $750K in equity & $250K in fixed income (75:25). The additional $500K isn't needed to support your SWR, so if you're really conservative you could put that all in fixed income. So you're overall AA would be 50:50 - $750 in equity, and $750K in fixed income.

My target AA is in my signature, and that won't change just because the market is reaching new highs (BTW, hopefully there will always be new highs, inevitably laced with periodic corrections). Had I sold off every time my portfolio hit a high in the past 30 years, I probably wouldn't be FIRE today. I may never exit equities altogether, keeping a 20-30% exposure in my 80's or thereabouts may be the best bet. My Dad is all cash, but he's 91 years old. YMMV

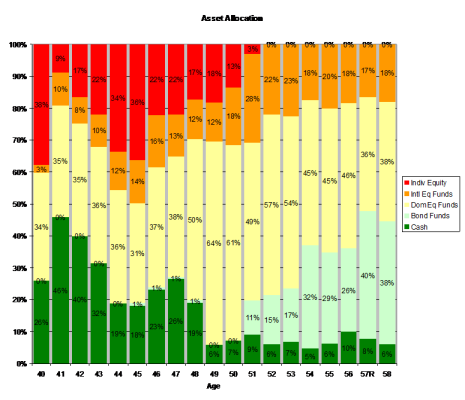

FWIW, here is how my asset allocation has progressed, you can see I've become more conservative as the nest egg has grown. Best of luck...