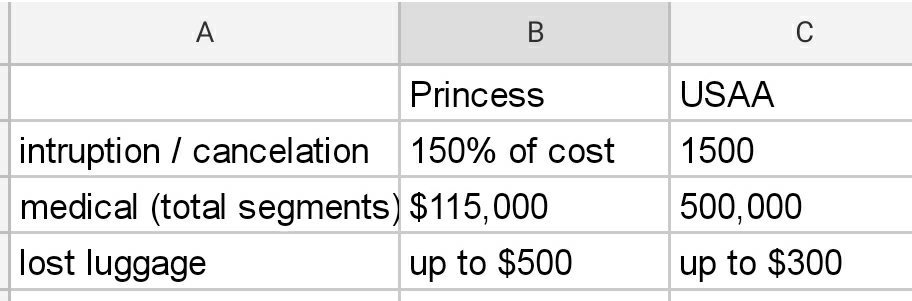

Also consider the maximum loss payable and the trip duration for the credit card insurance. We got Chase Sapphire cards mainly because of the travel insurance benefit, but it only covers trips up to 60 days and no more than $10K. That’s great for shorter trips but did not help us for our recent Australia trip.

For credit card travel insurance, you must book your travel with the card.

So airline tickets, cruises, train tickets, whatever the main transportation cost is to get you to your destination.

I'm not sure if it covers hotels or rental cars booked with other cards though but the verbiage is coverage for unused portions of the trip if for instance your trip is delayed or interrupted or canceled before it starts.

That's assuming you can't get refunds. I suppose you will have to document that you are unable to obtain refunds. AFAIK, there isn't a requirement to book only refundable hotel rates.

But there are also strict daily limits on the travel delay portion of the coverage.

I believe that goes for all travel insurance, whether from credit cards or a separate policy.

Also when you go to sites like insuremytrip.com or squaremouth.com, you have to enter the dates of the trip, where you're going to and the cost of the trip.

If you put in the full amount, you're asking for cancellation coverage and the premiums will run into hundreds for a trip.

I usually enter zero because I'm mostly interested in health care coverage (primary or secondary), medical evacuation and some trip delay or interruption. Adding rental car coverage also makes the premiums go up so I use Chase Saphire Preferred to pay for the car rental, to get primary coverage.

That results in policies which start around $40-50 for a 2-3 week trip.

I haven't looked into those annual policies but they seem to be similar policies to the ones I get per trip but they're a couple hundred and won't cover a lot of cancellation costs.

I looked into CFAR (Cancel for Any Reason) policies and they will be more because you have to specify the amount of the trip (and they cover up to 80-90% I believe, maybe less). But you have to book a CFAR policy right away, like right after your first charge, which for me typically is the flight fare. If you wait a couple of weeks or more, CFAR is no longer available for the trip.