Has anyone seen the new rates for June 2024 - May 2025? It may be a stupid question as I do not know if their "AGE 77 STANDARD RATE INCREASE / AGE 81 STANDARD RATE INCREASE" occurs in June for all states. It's June for me and DW.

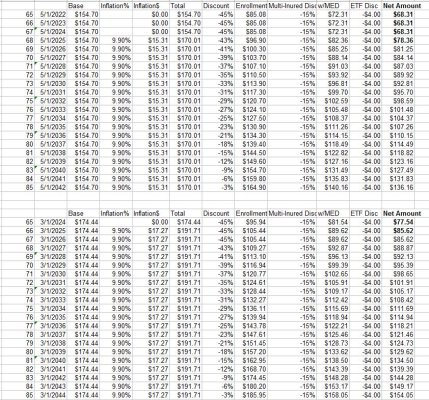

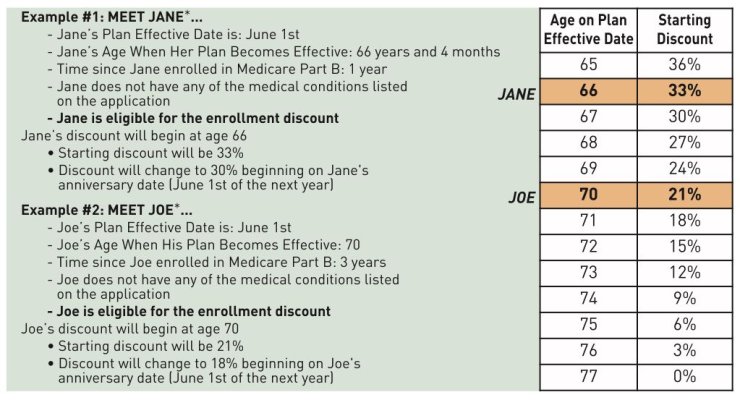

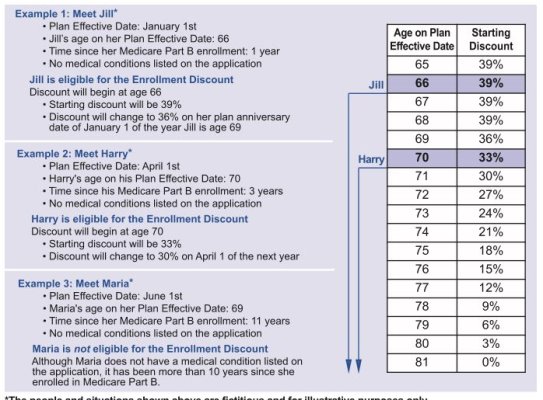

Your discounts are based on these standard rate increases, depending on your age, where you are at in the discount %, and what Standard Rate applies to you.

Your discounts are based on these standard rate increases, depending on your age, where you are at in the discount %, and what Standard Rate applies to you.