ventoux

Dryer sheet aficionado

Thanks, Freedom.

Today I see a 5 year TIP at auction paying 1.831 (indicative yield). So do you consider this a good deal or do you think it's better to wait for 10 year ones ?

The Bank of America 6% 2027 note is now on Fidelity.

Bond CUSIP 06048WZ29

Description BK OF AMERICA CORP SER N MTN 6.00000% 10/20/2027

Schwab has it. Hard to pass up. Wish I knew the chances of default but I guess that's true for everyone..When is the last time a bank of this size defaulted?

The Bank of America 6% 2027 note is now on Fidelity.

Bond CUSIP 06048WZ29

Description BK OF AMERICA CORP SER N MTN 6.00000% 10/20/2027

Would take this BOA bond instead of the 6% CITIGROUP bond (CUSIP 17330RH65)?

Freedom; Do you expect municipals to sell off in the same way as corporates in the last weeks of this year?

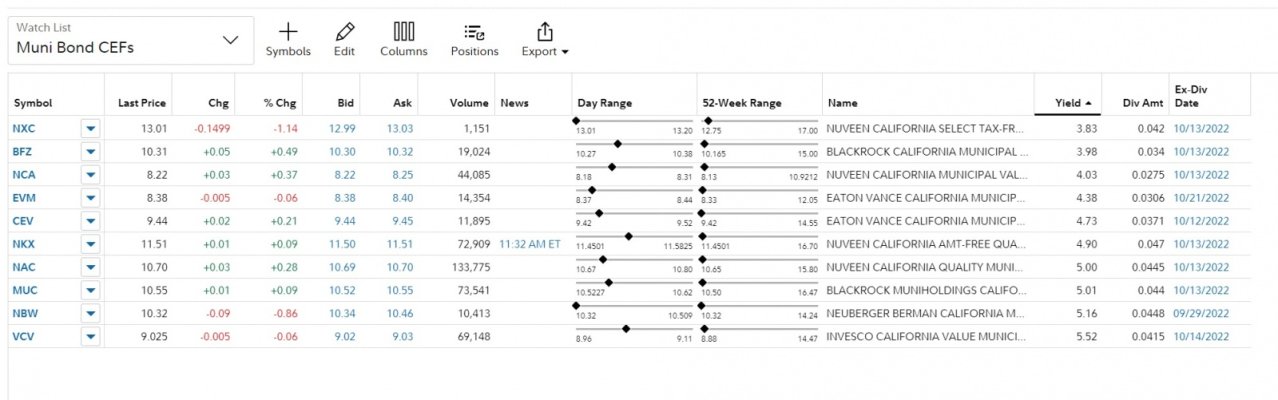

I expect Muni CEFs to sell off and some individual issues as well. Any security with low coupons or distributions will get slaughtered first during tax loss selling season. They higher coupons will then follow as they get dragged down by the soaring yields of the low coupon securities. When the carnage is over, the higher coupon securities bounce back the fasted as funds and investors buy the highest coupon securities first.

Here are some CEFs that I'm tracking. The leveraged muni CEFs are now yielding 5.5% and the unleveraged are at 3.8%. Those yields will go much higher as investors start taking their losses. Look at the 52 week range of these CEFs to appreciate the losses investors are facing.

Thanks for your response. Our individual bonds and dry powder to be allocated to bonds are all at Fido. So if I am looking for good yielding individual Munis during this sell off period, watching the municipal bond screener on Fido daily would be the best approach? In looking at it today, most Munis are selling at over par, so not enticing. Do you expect opportunities at or below par, in the coming weeks?

Looking at the fido screener, I didn't notice if there was a field showing if the issue is tax exempt. Is that info available by indivual issue at Fido, and if not, what website do you use to determine tax status?I'm assuming that you are referring to tax free muni bonds. Most people who buy tax free Muni's buy at or slightly above par to avoid a taxable gains at maturity. Fido's screen is probably the best among brokerage firms for muni bonds.

Looking at the fido screener, I didn't notice if there was a field showing if the issue is tax exempt. Is that info available by indivual issue at Fido, and if not, what website do you use to determine tax status?

Sent from my SM-T510 using Early Retirement Forum mobile app

One more question Freedom. Looking forward to the day when interest rates drop, from where they are now, or will be soon, do you sell some of your individual bonds ( any type), or hold them to maturity and then redeploy. I'm always stymied by the big gains I see in our bonds, because if I sell them, I have to find a replacement which is going to yield less. So I miss all of these gains. I suppose it's the flip side of holding bonds that have losses , but if held to maturity mature at par. Just wondering how you view your portfolio.

Sent from my SM-T510 using Early Retirement Forum mobile app

One more question Freedom. Looking forward to the day when interest rates drop, from where they are now, or will be soon, do you sell some of your individual bonds ( any type), or hold them to maturity and then redeploy. I'm always stymied by the big gains I see in our bonds, because if I sell them, I have to find a replacement which is going to yield less. So I miss all of these gains. I suppose it's the flip side of holding bonds that have losses , but if held to maturity mature at par. Just wondering how you view your portfolio.

Sent from my SM-T510 using Early Retirement Forum mobile app

Keep in mind if you have a gain, the yield has dropped anyway.

I don't want to go out 10 years when I can get very similar yields at 1-2 years.Help me understand what I’m looking at --- I see a non-callable agency note (Federal Home Loan Banks). The coupon rate isn’t comparable to other current options but it’s not callable and I’m curious what the downside would be in purchasing the issue outside of its lengthy maturity schedule. Thanks for any responses!

CUSIP: 3130ATHY6

Coupon: 4.25%

Maturity: 9-10-2032

Last trade price today: $96.95

YTM: 4.635%

")

well I'm no expert and there are people on here much more versed on these things than me. Hopefully you'll get some more responses/ideas.Thanks, finnski1. Yep, I'm looking at trying to lock in on some longer term issues with feasible yields but as you stated it's probably not the time for that right now.

With bonds/notes, if my capital gain exceeds or is close to the remaining coupon payment, it's going to be sold.