Gulp. This has got to be job 1 for you. If you don't know where it is going, how can you control it? Agree with slow but steady that you should divert $$ to investment right off the top (which the 401k does do for you), but you need to get a handle on your spending.

I've used quicken for many (too many!) years to track everything we spend outside of small cash expenditures--everything noteworthy is via credit card or direct from bank account, which makes it easy. Others swear by YNAB, various forms of envelope systems, and the old reliable spreadsheet. [and, duh, Mint.com] I don't think it makes any difference which method you use, but nail the outflow down.

With that income in Austin, you are in a fantastic position; you just need to figure out how to take advantage of it. This might be a very useful endeavor for you and your gal to do together so that you have a course charted before the wedding.

(AND, three cheers for your plans for Roth and 401k maxing--that is a very good thing.)

Edited to add....

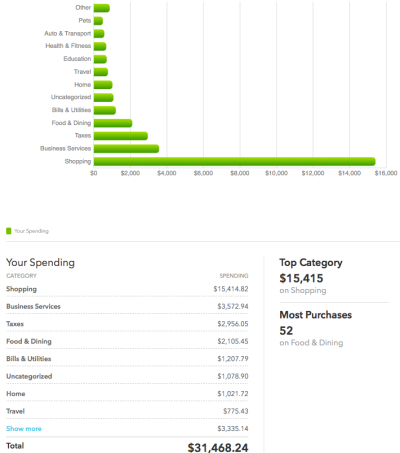

Setting up Mint today.

")