Independent

Thinks s/he gets paid by the post

- Joined

- Oct 28, 2006

- Messages

- 4,629

you might be surprised by your first payment.

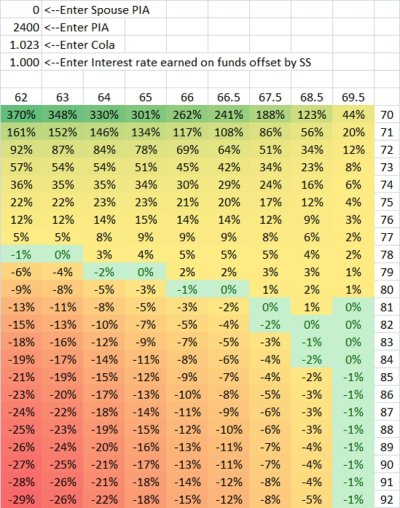

When I first read this thread http://www.early-retirement.org/forums/f28/odd-ss-payout-vs-retirement-age-graph-73457.html I said this can't be right. After all, for those of us born after 1942, we're supposed to "earn" another 2/3 of 1% of our PIA for each month that we defer. Retirement Planner: Delayed Retirement Credits

But, I was wrong. The fact that these Deferred Retirement Credits are "earned" doesn't mean that they will be in my first check. The initial payment only includes the months prior to the beginning of the calendar year in which I file for benefits.

Tadpole has an example where he files 12 months after eligibility, but only gets 2 months of DRCs. Or, if he files 24 months after eligibility, he only gets 14 months of DRCs.

As close as I can follow, the benefit is recalculated the next January, and benefits paid after that reflect all the earned DRCs. But, there is no retro-active lump sum payment for the benefits lost in the first year.

Here's a section of the Federal Register that seems to help (scroll down to "(c) When is the increase because of delayed retirement credits effective?")20 CFR 404.313 - What are delayed retirement credits and how do they increase my old-age benefit amount? | LII / Legal Information Institute

Apologies to people who posted on the earlier thread and seem to have this worked out. I was so surprised at the result that I wanted to repeat it in a thread with a more specific title.

And, thanks to a number of posters on the Bogleheads forum who provided some good information.

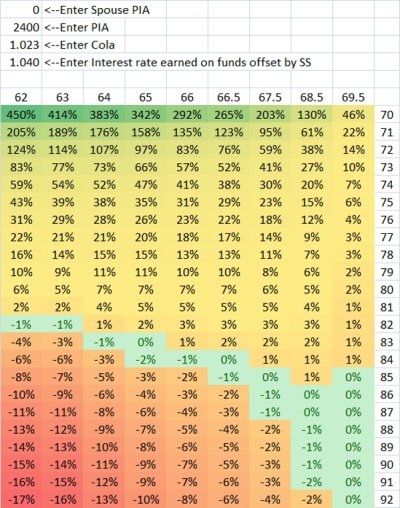

When I first read this thread http://www.early-retirement.org/forums/f28/odd-ss-payout-vs-retirement-age-graph-73457.html I said this can't be right. After all, for those of us born after 1942, we're supposed to "earn" another 2/3 of 1% of our PIA for each month that we defer. Retirement Planner: Delayed Retirement Credits

But, I was wrong. The fact that these Deferred Retirement Credits are "earned" doesn't mean that they will be in my first check. The initial payment only includes the months prior to the beginning of the calendar year in which I file for benefits.

Tadpole has an example where he files 12 months after eligibility, but only gets 2 months of DRCs. Or, if he files 24 months after eligibility, he only gets 14 months of DRCs.

As close as I can follow, the benefit is recalculated the next January, and benefits paid after that reflect all the earned DRCs. But, there is no retro-active lump sum payment for the benefits lost in the first year.

Here's a section of the Federal Register that seems to help (scroll down to "(c) When is the increase because of delayed retirement credits effective?")20 CFR 404.313 - What are delayed retirement credits and how do they increase my old-age benefit amount? | LII / Legal Information Institute

Apologies to people who posted on the earlier thread and seem to have this worked out. I was so surprised at the result that I wanted to repeat it in a thread with a more specific title.

And, thanks to a number of posters on the Bogleheads forum who provided some good information.