youbet

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Everyone who logs in here can do it with our advice as a starting point.

Or despite our advise............

Everyone who logs in here can do it with our advice as a starting point.

Is this it? There seem to be several but I liked this one.

Note: R-rated so perhaps NSFW - turn the volume down if you're at w*rk.

I fired my FA years ago when I asked him why he was't retired (he was in his late 60's). His reply was "I'm not debt free". The way he said it sounded like he was buried in debt. That sealed the deal.

Sent from my iPad using Early Retirement Forum

And for the honest ones, I've always wonder why they are still working for a living, if they are so financially gifted.

")

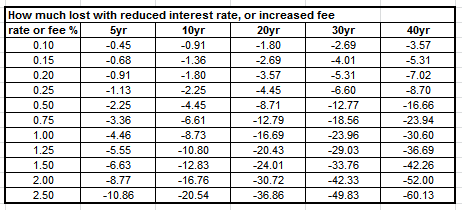

We save this much by not paying someone else to manage out investments.

That's one side of the coin. I look at return after expenses against benchmarks. If they're outperforming then the fees are well-spent. Would you choose a fund with a 0.5% expense ratio and a 5% average return after expenses over a fund with a 2% expense ratio (assuming similar investment objectives) and an average net return of 6%, just because the former has a lower expense ratio?

I'm pretty sure this thread is about showing the OP how a core of index funds is used, rather than guiding him towards higher expense funds.That's one side of the coin. I look at return after expenses against benchmarks. If they're outperforming then the fees are well-spent. Would you choose a fund with a 0.5% expense ratio and a 5% average return after expenses over a fund with a 2% expense ratio (assuming similar investment objectives) and an average net return of 6%, just because the former has a lower expense ratio?

Another thought on 401(k) vs rolling it out.

Some 401(k)'s offer a stable value fund. This is similar to a CD - pays interest... but usually at a higher rate than current CD rates. This is something that isn't available outside 401(k)s... so if you have one, you might want to keep at least some of your money in the 401(k)... but do it based on your asset allocation that you'll figure out after doing some research, reading, and/or consulting a fee-based FA.

Given two investments with equal risk, this scenario seems like a slam dunk. The problem is that I've never seem a convincing argument that the better performing managed investment can be chosen in advance. Looking backward, it happens, but only for the lucky........... If they're outperforming then the fees are well-spent. Would you choose a fund with a 0.5% expense ratio and a 5% average return after expenses over a fund with a 2% expense ratio (assuming similar investment objectives) and an average net return of 6%, just because the former has a lower expense ratio?

I am a financial advisor. Some people are perfectly capable of handling their own investments without the help of a financial advisor, some are not. The thing that makes managing your own investments difficult is that it isn't just money. Its your life savings, its your security and its the difference between working longer or retiring, and also living comfortably in retirement or not. It's a very emotional thing and it is hard for some people to make rational decisions about their money when the stakes regarding failure are so high. ...

Don't tell everyone they can do it alone- everyone can't!

Andy Sr, our experience has been the small fee's to our FA and CPA, are well worth it.

Given two investments with equal risk, this scenario seems like a slam dunk. The problem is that I've never seem a convincing argument that the better performing managed investment can be chosen in advance. Looking backward, it happens, but only for the lucky.

I am a financial advisor. Some people are perfectly capable of handling their own investments without the help of a financial advisor, some are not. The thing that makes managing your own investments difficult is that it isn't just money. Its your life savings, its your security and its the difference between working longer or retiring, and also living comfortably in retirement or not. It's a very emotional thing and it is hard for some people to make rational decisions about their money when the stakes regarding failure are so high. If you are not sure if you can stick with your plan if your portfolio declines in value by 25, 40 or 50%, you may want to hire some help. If you can stand the volatility, you will certainly get off cheaper doing it yourself. Financial Advisors, (like Doctors, Lawyers, Accountants, Engineers etc all have to earn a living)

Financial Advisors are accustomed to being "interviewed" by prospective clients. He/she should explain all of your options and all of the fees, and explain what you expect to get in return for your fees. Referrals are a great idea- one of the best indicators of a good financial advisor is when they advise you of something that is clearly not in their best interest- its in yours. Ask your friends which of their advisors have told them NOT to sell in a down market, have discouraged them from buying "hot stocks" they heard about on the golf course, and have steered them away from expensive products they don't need.

Y'all are a very self-sufficient bunch. Anyone who has the self-discipline to accumulate the assets you have requires intelligence and good decision-making skills. Recommending to EVERYONE that they invest on their own assumes that they have the same er, intestinal fortitude that you do- could be a mistake. Tons of investors sold out during 08-09 and will never recover from that loss. Don't tell everyone they can do it alone- everyone can't!

Was wondering what most people think of financial advisors versus leaving my money in my company 401K. There's a few people at work that are taking their funds from there 401K and transferring them over to personal financial advisors. Not sure how to find a good one. Not sure if it's a good move.

Sent from my iPad using Early Retirement Forum

I don't think so.. why do you say that?