USGrant1962

Thinks s/he gets paid by the post

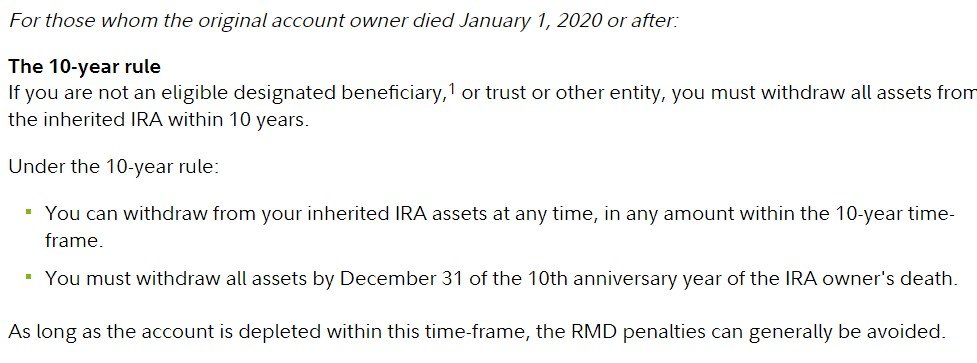

A newsletter pointed me to this. The new 2020 IRS Pub 590-B still requires non-spouse IRA beneficiaries to take RMDs, they've interpreted the SECURE Act 10-year rule as an "and". As in you must take RMDs and fully distribute the account in 10 years. From the pub:

and

I also looked at the SECURE Act law (PL 116-94) and it says nothing about suspending RMDs. I don't know where the "punt RMDs for 10 years" idea actually came from.

The newsletter suggests this came as a surprise to financial planners, and that IRS Publications are not regulations, so things could change. IRS has not yet issued its official regulations on the matter yet (26 CFR) and there is always tax court.

Hmmm.

Other designated beneficiary. Use the life expectancy listed in the table next to the beneficiary’s age as of his or her birthday in the year following the year of the owner’s death. Reduce the life expectancy by 1 for each year since the year following the owner’s death. However, if you are a designated beneficiary who is not an eligible designated beneficiary, the entire account balance must be fully distributed within 10 years after the owner's death.

and

Example. Your father died in 2020. You are the designated beneficiary of your father's traditional IRA. You are 53 years old in 2021, which is the year following your father's death. You use Table I and see that your life expectancy in 2021 is 31.4. If the IRA was worth $100,000 at the end of 2020, your required minimum distribution for 2021 would be $3,185 ($100,000 ÷ 31.4).

I also looked at the SECURE Act law (PL 116-94) and it says nothing about suspending RMDs. I don't know where the "punt RMDs for 10 years" idea actually came from.

The newsletter suggests this came as a surprise to financial planners, and that IRS Publications are not regulations, so things could change. IRS has not yet issued its official regulations on the matter yet (26 CFR) and there is always tax court.

Hmmm.

Last edited: