pb4uski

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Is the Roth conversion if over 59.5 all tax free immediately upon withdrawal (earnings included)?

Agreed... under 59-1/2 needs a different strategy.

Is the Roth conversion if over 59.5 all tax free immediately upon withdrawal (earnings included)?

Is the Roth conversion if over 59.5 all tax free immediately upon withdrawal (earnings included)?

From my understanding, Roth conversion withdrawals after the age of 59.5 do not have a 5 year waiting period unless your original Roth account is less than 5 years old. I asked this question a few years back and this was my conclusion.

Ok. This sounds like a strategy I could implement as well. So, exhaust your taxable account first, then do Roth conversions and live off the Roth conversion dollars. The taxes would be paid out of the Roth conversion dollars and not from a taxable account. Is that the strategy?

You can until RMD age. At the RMD age , the amount required cannot be for a roth conversion. After you have taken the RMD, then more can be withdrawn to do a Roth Conversion.

I think the law is this way to encourage folks to spend money, or at least be able to tax them the next year on the interest gained from the previous year(s) RMD withdrawal that is unspent.

+1 All Roth withdrawals after 59-1/2 are penalty-free as long as the Roth account is 5 years old or older. If the account is less than 5 years old then only withawal of contributions is penalty-free.

You can until RMD age. At the RMD age , the amount required cannot be for a roth conversion. After you have taken the RMD, then more can be withdrawn to do a Roth Conversion.

I think the law is this way to encourage folks to spend money, or at least be able to tax them the next year on the interest gained from the previous year(s) RMD withdrawal that is unspent.

You can until RMD age. At the RMD age , the amount required cannot be for a roth conversion. After you have taken the RMD, then more can be withdrawn to do a Roth Conversion.

I think the law is this way to encourage folks to spend money, or at least be able to tax them the next year on the interest gained from the previous year(s) RMD withdrawal that is unspent.

I think the law is this way to prevent tax deferred or non taxable accounts ad infinitum. Once you reach RMD age you are disallowed from moving the RMD into a Roth for additional tax-free growth. More than the RMD sure as you have met your required distribution.

Let me make sure I understand your statements. At age 75 (RMD age for me), if my RMD is $10,000, I cannot do a Roth conversion in that amount. However, I could do a Roth conversion for $10,001. That is more than my RMD amount by one dollar. Is that the tax law?

If your RMD is $10,000 you must withdraw $10,000 or do a $10,000 QCD. You can request the all or some of the $10,000 be withheld for federal taxes. Then you can withdraw additional money and send that additional money to a Roth (do a Roth conversion), but not any of the original $10,000.Let me make sure I understand your statements. At age 75 (RMD age for me), if my RMD is $10,000, I cannot do a Roth conversion in that amount. However, I could do a Roth conversion for $10,001. That is more than my RMD amount by one dollar. Is that the tax law?

So, my first Roth account was opened in 2022 to allow me to do backdoor Roth conversions. So, if I start doing regular Roth conversions (convert 401k dollars to Roth dollars) when I turn 59 1/2 on 01/2026, I will have to wait until 01/2027 to withdraw any Roth dollars from the regular Roth conversions that I started in 01/2026.

If your RMD is $10,000 you must withdraw $10,000 or do a $10,000 QCD. You can request the all or some of the $10,000 be withheld for federal taxes. Then you can withdraw additional money and send that additional money to a Roth (do a Roth conversion), but not any of the original $10,000.

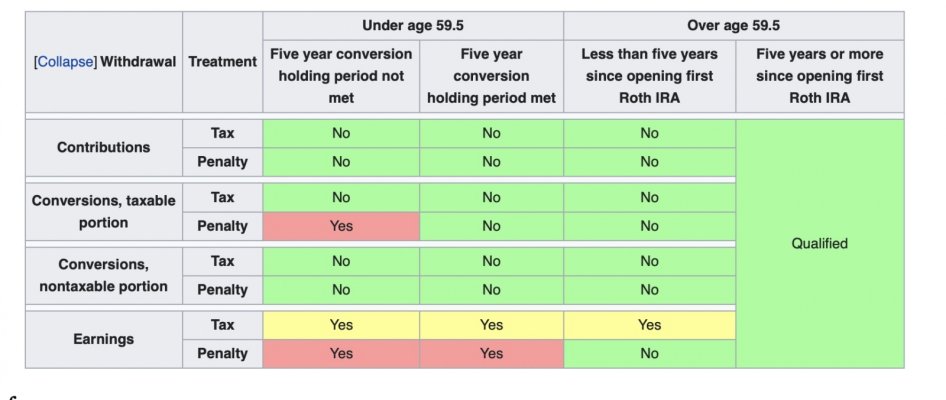

No, not quite correct. When you turn 59.5, you may withdraw ALL of the contributions and conversions from your Roth IRA(s), free of tax and penalties. However, if you withdraw enough to be withdrawing any earnings (i.e., funds in excess of your contributuions and conversions), then you will have to pay a tax (but not a penalty) on those amounts.

Again, see here: https://www.bogleheads.org/wiki/Roth_IRA#cite_note-23

This can get very complicated and confusing. My first Roth was opened in 2022 and I started contributing to my wife and I Roth IRA by doing backdoor Roth conversions. I will continue this approach through 2025. This year, I will be 58 and my wife will be 61. Can you help answer the following questions below based on my situation (wife and I):

2022 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty?

When are growth dollars (earnings) available to Withdraw without 10% penalty?

When are conversion dollars available to Withdraw without paying taxes?

When are growth dollars (earnings) available to Withdraw without paying taxes?

2023 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty?

When are growth dollars (earnings) available to Withdraw without 10% penalty?

When are conversion dollars available to Withdraw without paying taxes?

When are growth dollars (earnings) available to Withdraw without paying taxes?

2024 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty?

When are growth dollars (earnings) available to Withdraw without 10% penalty?

When are conversion dollars available to Withdraw without paying taxes?

When are growth dollars (earnings) available to Withdraw without paying taxes?

2025 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty?

When are growth dollars (earnings) available to Withdraw without 10% penalty?

When are conversion dollars available to Withdraw without paying taxes?

When are growth dollars (earnings) available to Withdraw without paying taxes?

Yes, I agree.So, I can use the RMDs to pay for my taxes at the end of the year. That seems to be a good use of the RMD dollars. Would you agree?

I agree it is confusing. However, it doesn't really work like the way you posed your questions. There are not "2022 dollars" and "2023 dollars," nor are there Conversion Dollars and Growth Dollars.

So, to answer your question, more information is needed. Have you made regular contributions to the IRA account? Have you made taxable conversions (where you paid tax on money that was in a tax-deferred account at the time of conversion)?

Before 59.5, at any point in time, you can withdraw the sum of all of your prior contributions and conversions that are > 5 years old without tax or penalty. This is true even if the your first Roth is less than 5 years old. But to say more, we would need to know more about whether you made taxable conversions.

I think you need to carefully read this section in the BH Wiki, then ask more questions: https://www.bogleheads.org/wiki/Roth_IRA#Distributions

Edited to add: And here is the description from the IRS in Publication 590-B. I think the BH version is clearer.

https://www.irs.gov/publications/p590b#en_US_2022_publink100089915

All of the dollars are non-deductible contributions (post-tax dollars) that goes first to a T-IRA and then are converted immediately to the Roth IRA. That is the only way I know how to do a backdoor Roth contribution/conversion based on the fact that I exceed the income requirements to directly contribute to the Roth IRA.

That is the only way I know how to do a backdoor Roth contribution/conversion based on the fact that I exceed the income requirements to directly contribute to the Roth IRA.

Yes, but you could have done "regular" conversions from a tax-deferred account in addition to the backdoor. It turns out to be helpful to you that you did not!

Understanding that I am just SGOTI, I believe that the answer to your questions are as follows. I am assuming that you will be 59.5 in 2025, although I don't think you said that explicityly. It could be that you turn 59.5 in 2026; if so, the "2025" dates below should be 2026.

2022 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty? NOW

When are growth dollars (earnings) available to Withdraw without 10% penalty? In 2025, when you are 59.5

When are conversion dollars available to Withdraw without paying taxes? NOW

When are growth dollars (earnings) available to Withdraw without paying taxes? In 2025, when you are 59.5.

2023 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty? NOW.

When are growth dollars (earnings) available to Withdraw without 10% penalty? In 2025, when you are 59.5

When are conversion dollars available to Withdraw without paying taxes? NOW.

When are growth dollars (earnings) available to Withdraw without paying taxes? In 2025, when you are 59.5

2024 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty? NOW, well, I mean after you actually make the conversion.

When are growth dollars (earnings) available to Withdraw without 10% penalty? In 2025, when you are 59.5

When are conversion dollars available to Withdraw without paying taxes?NOW, well, I mean after you actually make the conversion.

When are growth dollars (earnings) available to Withdraw without paying taxes? In 2025, when you are 59.5

2025 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty? After you make the conversion.

When are growth dollars (earnings) available to Withdraw without 10% penalty? When you turn 59.5

When are conversion dollars available to Withdraw without paying taxes? After you make the conversion.

When are growth dollars (earnings) available to Withdraw without paying taxes? When you turn 59.5

Note that the ordering rules imply that, say, the 2024 conversion amounts come out before the 2022 earnings, assuming that you will have not theretofore withdrawn more than your 2022 + 2023 conversions.

Understanding that I am just SGOTI, I believe that the answer to your questions are as follows. I am assuming that you will be 59.5 in 2025, although I don't think you said that explicityly. It could be that you turn 59.5 in 2026; if so, the "2025" dates below should be 2026.

2022 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty? NOW

When are growth dollars (earnings) available to Withdraw without 10% penalty? In 2025, when you are 59.5

When are conversion dollars available to Withdraw without paying taxes? NOW

When are growth dollars (earnings) available to Withdraw without paying taxes? In 2025, when you are 59.5.

2023 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty? NOW.

When are growth dollars (earnings) available to Withdraw without 10% penalty? In 2025, when you are 59.5

When are conversion dollars available to Withdraw without paying taxes? NOW.

When are growth dollars (earnings) available to Withdraw without paying taxes? In 2025, when you are 59.5

2024 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty? NOW, well, I mean after you actually make the conversion.

When are growth dollars (earnings) available to Withdraw without 10% penalty? In 2025, when you are 59.5

When are conversion dollars available to Withdraw without paying taxes?NOW, well, I mean after you actually make the conversion.

When are growth dollars (earnings) available to Withdraw without paying taxes? In 2025, when you are 59.5

2025 Backdoor Roth conversion

When are conversion dollars available to Withdraw without 10% penalty? After you make the conversion.

When are growth dollars (earnings) available to Withdraw without 10% penalty? When you turn 59.5

When are conversion dollars available to Withdraw without paying taxes? After you make the conversion.

When are growth dollars (earnings) available to Withdraw without paying taxes? When you turn 59.5

Note that the ordering rules imply that, say, the 2024 conversion amounts come out before the 2022 earnings, assuming that you will have not theretofore withdrawn more than your 2022 + 2023 conversions.

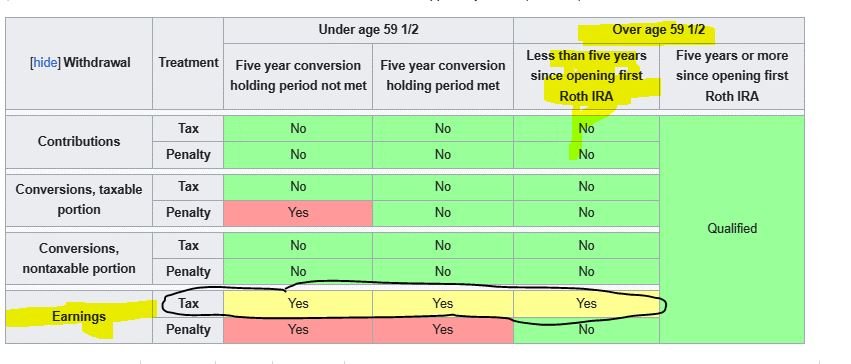

For your response to the question "When are growth dollars (earnings) available to Withdraw without paying taxes?", is the correct response "Over age 59 1/2 and five years or more since opening first Roth IRA".

Since my first Roth IRA was opened in 2022, would the answer be Jan 1, 2027? I would be over 59 1/2 and it would be 5 years since I opened my first Roth IRA.

Yes, I believe you are correct! The student has become the master!