corn18

Thinks s/he gets paid by the post

- Joined

- Aug 30, 2015

- Messages

- 1,890

Highest it's been since Aug 2006. Not sure what it means other than the bond market is not convinced of the transitory hope for inflation.

Thank youThe 10 year breakeven rate serves as an indication of the markets' inflation expectations over the 10 year horizon. ... The spread or gap between 10 year Treasuries and TIPS will be lower if fixed income traders' inflation expectations are lower.

In the eye of the beholder, I guess. 2.64%/10 years, dollars have lost about 1/4 of their buying power/prices are up 30% in dollar terms. So I think it's "much" but certainly the central bankers do not.Even so, 2.64 pct is not much inflation. ...

In the eye of the beholder, I guess. 2.64%/10 years, dollars have lost about 1/4 of their buying power/prices are up 30% in dollar terms. So I think it's "much" but certainly the central bankers do not.

SecondAttempt,

Be careful using averages here. Sequence is critical.

Even so, 2.64 pct is not much inflation.

I think my interpretation would be that dispite current price spikes, the long-term inflation rate is currently only expected to be 2.64 percent, and that is up only modestly from recent history.

I'm seeing inflation for 10% or greater on most things.

I concur. I think inflation is 10%+, and will be for a few years before becoming more tame, but at elevated price levels.

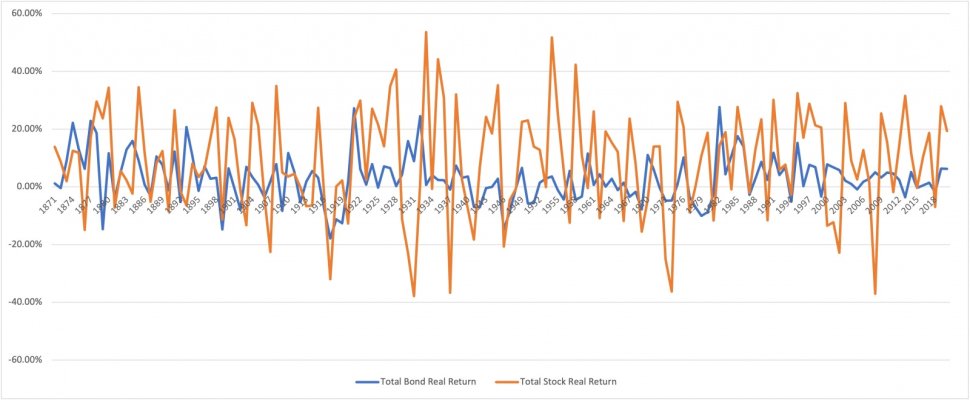

It kinda puts in prospective the 15% returns...which are actually less than 5 points ahead of the wave of inflation.

There are a lot of economists that argue that inflation around 2-3% is far better than zero or negative inflation. That range provides a cushion against a deflationary spiral which would be bad for almost everyone.

I don't see why 2.64% is scary. If we assume that 10 year US Treasuries return about 2% long term and stocks return 6% over 10 year US Treasuries, then it only takes about 10% exposure to stocks to achieve a 2.64% return to keep up with inflation.

I have no idea what the long term return of 10 year US Treasuries will be but the 6% equity risk premium has held up for a very long time so I personally think we can rely on that.

I am sanguine about how to think abou this. My entire working life inflation has been significantly higher than 2.64% so that figure seems good. But I have been working and getting regular salary increases that masked inflation from me. I realize it will be different when I retire.

On top of that, there are so many crazy things going on right now that I don't actually believe any data since about January 2020 should be used to make any projections. I personally think we have a few years of disruption ahead of us so I would not be surprised to see 4-ish % inflation for 3-4 more years. But I would not be worried about that.

My "prediction" is based on a general rule for complex systems that when there is a period of disruption it takes the system 2-3 of the same time period to stabilize again. With covid and associated market disruptions we had about 1.25 years of disruption so stabiliztaion should not be expected for 2.5 to 3.75 years from July 1, 2021 meaning end of 2023 to early 2025. It's just a S.W.A.G. but I am not going to get too worried about any inflation numbers before that time frame. The 4% inflation estimate over that period is nothing more than taking the 6% we've seen recently and the 2% I expect things to stabilize to (as it was prepandemic) and averaging. I will almost certainly be wrong about exact details but I'm a numbers guy and need some baseline from which to make decisions.

Edit: typos

I agree with MontecfoI think part of the good news here is that the market is comfortable that the Fed actions are sufficient to keep inflation in check for the long term. So current Fed path is probably good, sayeth the market.

This is good news for investors.

Respectfully, inflation is not 10 pct. If you believe it is, curious how you are investing to mitigate this?

Respectfully, inflation is not 10 pct. If you believe it is, curious how you are investing to mitigate this?

If you adjust CPI for where rent prices have actually increased to rather than the owner's equivalent rent - which is dumb since 99% of owners have no idea what their house would rent for - CPI would be close to 10%. It's over 1/3 of the index and right now is using ~2.5% increase in rents - when in reality rents are up ~15% y/y currently (housing prices same).