You can walk through the qualified dividends and capital gains worksheet to see all the steps.

Conceptually:

1. Income is totaled - ordinary income first, preferenced income on top.

2. Standard (or itemized deductions) is subtracted from the bottom.

3. Ordinary income brackets are applied to any remaining ordinary income.

4. Capital gains brackets are applied to any remaining preferenced income.

In your case:

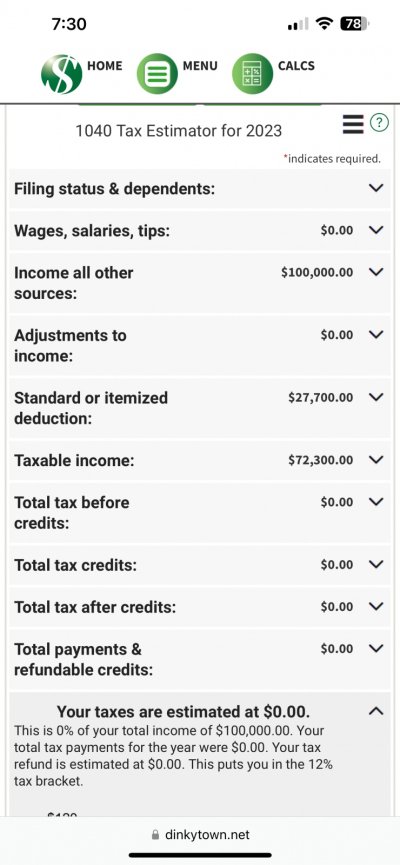

1. $25K of ordinary income as interest, $75K of preferenced income as qualified dividends.

2. $27.7K standard deduction is subtracted off the bottom. This erases all of the interest income and the first $2.7K of qualified dividends, leaving $72.3K.

3. Not applicable in this scenario because there is none remaining.

4. The remaining $72.3K all falls into the 0% bracket, so there would be $0 in federal income tax.

If there were more qualified dividends, some of them would fall into the 15% bracket. Like ordinary income brackets, only the portion of the qualified dividends that fell into the 15% bracket would be taxed at that rate and would end up on line 18 of the worksheet.

Here's a web page that outlines the worksheet in detail and what happens on it generally:

https://www.marottaonmoney.com/how-...lified-dividends-and-capital-gains-worksheet/

The couple would still have an AGI of $100K. AGI can affect things like state income taxes, ACA subsidies, and FAFSA. It also can affect eligibility for a large number of adjustments, deductions, and credits.