Way too young for an SPIA. And way too much money.

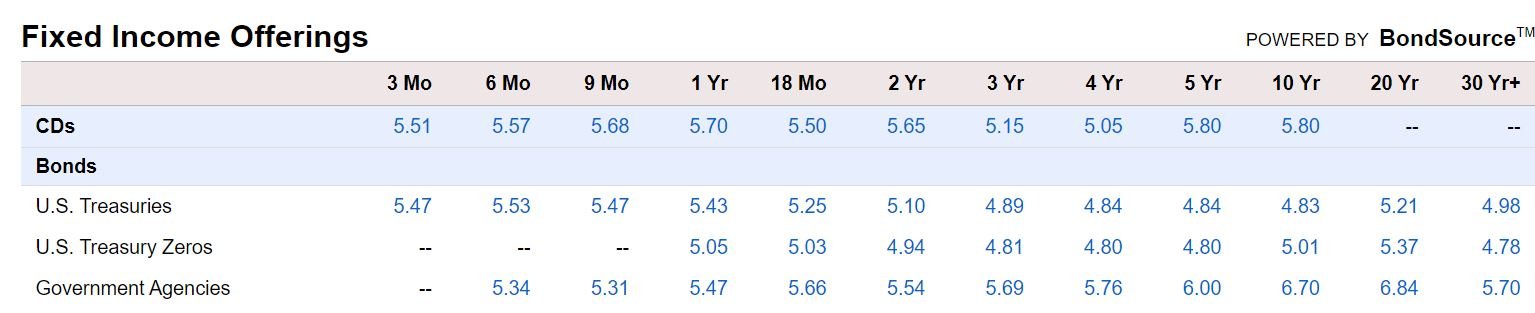

Fidelity does have some decent Deferred Fixed Annuities (MYGA) with some highly rated companies - 5 year at 5.2%. So, you could defer some interest for a few years and get a decent return, if that interests you. Oh, and you get your money back in the end. I've done one before and it worked out fine. I should note, you can find higher rates elsewhere, but usually at lower rated insurance companies. Fidelity only uses highly rated companies.

I have a meeting set up with my Fidelity advisor next week. First meeting since opening the account several years ago. I'll see if he tries to push annuities on me. Last time he didn't try to sell me anything.

Fidelity does have some decent Deferred Fixed Annuities (MYGA) with some highly rated companies - 5 year at 5.2%. So, you could defer some interest for a few years and get a decent return, if that interests you. Oh, and you get your money back in the end. I've done one before and it worked out fine. I should note, you can find higher rates elsewhere, but usually at lower rated insurance companies. Fidelity only uses highly rated companies.

I have a meeting set up with my Fidelity advisor next week. First meeting since opening the account several years ago. I'll see if he tries to push annuities on me. Last time he didn't try to sell me anything.