Sorry if I missed a thread on this... apparently there is a new study, The August 2011 issue of the Journal of Financial Planning included the paper, "Can We Predict the Sustainable Withdrawal Rate for New Retirees", by Wade D. Pfau, Ph.D., questioning 4-percent rule...

4-percent-withdrawal-rate-high-retirees-moneywatch: Personal Finance News from Yahoo! Finance:

4-percent-withdrawal-rate-high-retirees-moneywatch: Personal Finance News from Yahoo! Finance:

The paper goes on to predict safe withdrawal amounts for retirements beginning after 1980 (we won't know the safe withdrawal rate for 30-year retirements until the 30 years are up). The model described in this paper predicts safe withdrawal rates of 2.7 percent for retirements beginning in 2000, 1.5 percent for retirements beginning in 2008, and 1.8 percent for retirements beginning in 2010.

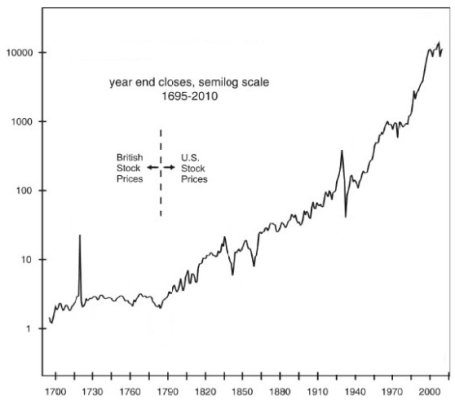

The paper then examined the periods for which low safe withdrawal rates were required, and found some patterns. The lowest safe withdrawal rates occurred for retirements beginning when interest rates on bonds were at historical lows, when dividend yields on stocks were below average, and price/earnings ratios on stocks were at or above historical averages. These three situations describe the current economic circumstances.

When you think about it, this only makes sense. Your retirement savings can generate only three types of retirement income: interest and dividends, appreciation in your retirement investments, and withdrawals of principal. If current economic conditions are such that the first two items are expected to be below historical averages, it only follows that your total retirement income will be below historical averages.

Last edited: