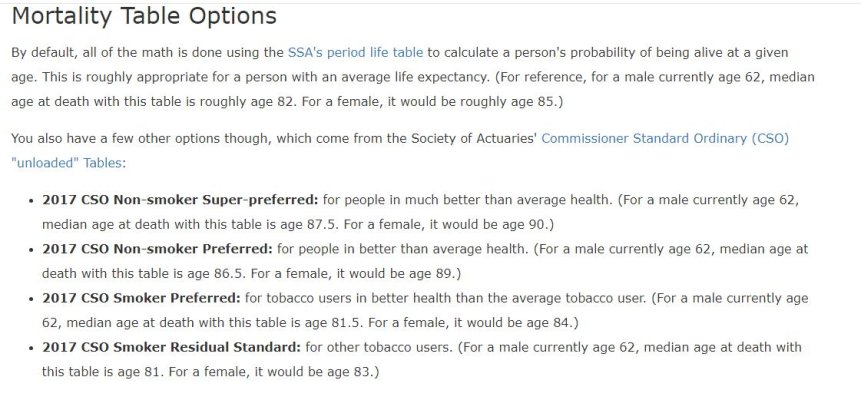

Schwab's ladder builder doesn't appear to work on Sundays

")

facepalm

, so I just cherry picked these from manual searches.

These are CDs. You can do the exact same thing with Treasuries.

I'm not suggesting these exact CDs, but it should give you an idea. The first two are callable but they are not many years so I don't think the risk is high. I chose non-callable for the later ones.

I'm also assuming this is in a tax deferred account and that you're looking for gross income. If you want $31,500 net of taxes, you'd need to increase the principle invested. Same thing if you want the $31,500 to grow to account for inflation.

2025 Income:

JPMorgan Chase & Co. OH 5.25% CD 12/12/2024 Callable

YTM 5.25% (Effectively 3.9% net as this matures in Dec.)

$30K invested -> $31,170 at maturity.

2026 Income:

Peoples Security Ban 4.6% CD 01/27/2026 Callable.

YTM 4.8%

$29K invested -> $31850 at maturity

2027 Income:

Discover Bank DE 2.8% CD 01/11/2027

YTM 4.4%

$28K invested -> $31860 at maturity

2028 Income:

UBS Bank USA UT 3.95% CD 01/10/2028

YTM 4.4%

$27K invested -> $32074

2029 Income:

Discover Bank DE 3.45% CD 01/16/2029

YTM 4.7%

$26000 invested -> $32711

Again, these are pre-tax amounts and inflation will chip away at the value. If you want $31,500 after-tax and to make an allowance for inflation, you will need to invest more.

I hope this is helpful.