SecondCor521

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

I was referring to Gumby's post #18, not yours.

Ah, I see now. Thanks.

I was referring to Gumby's post #18, not yours.

MAGI is before standard deductions, not after!I'm not sure if IRMAA is a good reason to constrain... if we convert to the top of the 22% tax bracket in 2020 that is taxable income of $171,050 and assuming the standard deduction for 65 year olds of $27,400 that is income/MAGI of $198,450.

I agree with Midpack's premise of converting to the top of the tax bracket that you expect to be in once all your income streams have started.... mainly because of the factor that if one of you passes the surviving spouse will get thrown into a higher tax bracket.

If her marginal tax rate once SS and RMDs are applicable will be 12%, then arguably yes but the benefit is smaller.

I forget, do Roth conversions count toward this limit?

Added in red.In your OP example, are you saying convert now to the top of the 22% bracket if you expect to otherwise be consistently in the 22% bracket once you turn 70?

I'm not sure if IRMAA is a good reason to constrain... if we convert to the top of the 22% tax bracket in 2020 that is taxable income of $171,050 and assuming the standard deduction for 65 year olds of $27,400 that is income/MAGI of $198,450. ....

MAGI is before standard deductions, not after! ...

The surviving spouse since tax rate issue: I keep finding estate tax planning ways to handle that “problem”.

Okay, but concerning my first question when folks analyze the benefits of Roth conversions, why wouldn't one also consider future years of RMD rates and not just the 70.5 rate?

i.e. the 3.65% rate at 70.5 jumps to ~5% at 78 y.o., which is much more than just inflationary type increases and perhaps what works for 70.5 y.o. then falls short at 78 y.o.

I agree that subsequent years should be considered.... in our case the rise in RMDs isn't sufficient to kick us into a higher tax bracket... don't forget that the tax brackets increase with inflation too.

Looks like withdrawals, ignoring tIRA growth, increase 3.4% initially and grade up as one ages, with growth from 80-81 being a little over 5%.

If you're near to the top of a tax bracket when 70.5 then that is a valid concern, but if your near the bottom or middle of a tax bracket then much less so.

Good timing thread for me.

I was just going to ask about do folks look at tax rates at 70.5 relating to Roth conversion decisions now, or look ahead at later age dates when the RMD rates will be higher.

When I did my RMD tax spreadsheet, I ran it out to age 85.

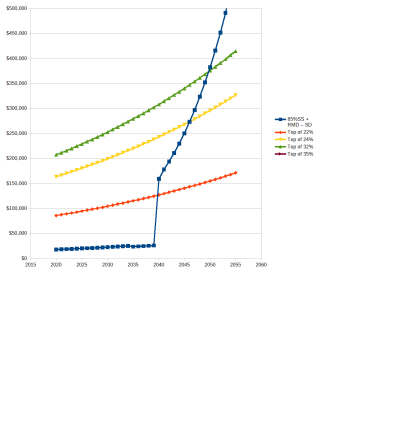

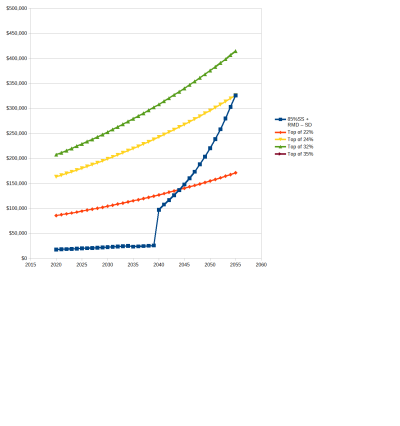

In my case, even with my planned conversions through 70.5 and RMD's from then on, it looks like I could have a sort of runaway situation on my hands: At age 70.5, my RMD (plus 85% SS minus standard deduction) will put me into the 24% bracket. About six years later, I'll be in the 32% bracket. Four years after that, I'll enter the 35% bracket.

Two comments:

1. As some Youtube financial guy pointed out to me (and @pb4uski mentioned here as well), there are differences that probably matter and differences that don't as much. 10% to 12% or 22% to 24%, meh. 12% to 22% or 24% to 32%, well I may pay attention to that a bit more.

2. From where I sit, it looks like I would have to approximately double my current conversion amount in order to get my age 85 bracket down to top of the 24% bracket. That's probably something I should look at in a few years once my FAFSA EFC era is over (I believe I have a large FAFSA cliff at $50K AGI for SNT).

So since one typically would not convert after 70.5, then if one takes into account future larger withdrawals into the RMD process and converts as such in their 60's, then one might be paying too much tax in their 60's as it relates to their 70's RMD situation, but might be correct for their 80's and beyond RMD situation.

Not sure that makes sense.

Don't you think the tax advantages of Roth conversions are misleading if they do not advise you to consider the amount of state taxes when making the decision? Like in Maryland, even though I am in 12% bracket, I must add on another 7.75% in state/local taxes. It does make converting less attractive because it is only 2.25% savings over a 22% bracket.

Or I am wrong?

Here are my projected numbers, from my nutso spreadsheet. Widowed, no direct heirs who I care about massaging taxes for. Working a couple more years, maxing Roth 401k/after-tax conversions, plus pensions, SS (survivor at 60, mine at 70), and a possible inheritance included, and a very generous yearly spend in my HCOL area without adjusting for slow-go and no-go years. About 85% of my money is in tax-deferred.

This includes RMDs, but not QCDs, and is assuming brackets will revert at the end of 2025. This means that while the top of the 24% bracket now is ~ $162k, the top of the 25% bracket will only be ~ $94k. All in today's numbers, and of course very very approximate. Assuming about 3% growth.

No conversions:

Now to age 70: ~ $280k in fed taxes paid overall

70 to 80: ~ $455k

80 to 90: ~$507k

Total to 90: ~$1.24m

Converting to the top of the 22% bracket and then 25%:

Now to age 70: ~ $360k

70 to 80: ~ $370k

80 to 90: ~ $735k

Total to 90: ~$1.23m

Converting to the top of the 24% bracket and then 25%:

Now to age 70: ~ $465k

70 to 80: ~ $310k

80 to 90: ~ $382k

Total to 90: ~$1.16m

It's sort of fascinating. There just isn't that much of a difference in the three scenarios--it's all about when I want to pay.

Though if I believe taxes are going to get higher (and I do), this could change a lot. But if I have the money to have to be paying high taxes when I'm older, then yay for me. (and probably yay for charities)

So, after being all "I'm maxing out conversions!" I'm now "no more conversions for me." Let old me deal with it.

There isn’t a free one that I know of other than one by a member on Bogleheads. I won’t provide a link because there’s no way to verify how accurate it is, it was revised 20 times IIRC (mostly not errors) and has some hidden and very difficult to follow calculations. I spent several sessions of several hours with it and decided I wasn’t satisfied.Can anyone direct me to a tax planning optimization spreadsheet similar to those referenced, please?

I have attempted one of my own ; however from this thread I see there are many complexities to consider.

For a single year, the best publicly available spreadsheets seem to be the case study spreadsheet and https://sites.google.com/site/excel1040/.Can anyone direct me to a tax planning optimization spreadsheet similar to those referenced, please?

I have attempted one of my own ; however from this thread I see there are many complexities to consider.

And remember that, if the conversion tax is paid from cash on hand, converting now in the 22% or higher federal brackets beats converting later, even if the marginal rate later is identical to the marginal rate now.

Removing the tax drag on the taxable funds is what breaks the tie.

). We are currently in the 22% bracket and will be in at least that same bracket at age 70.