SecondCor521

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Hi all.

52M, single, FIREd for 5 years. Doing the typical Roth conversions between now and age 72 when I plan to start RMDs. I plan to take SS at 70.

For the purposes of this post, please set aside any discussions of tax rates sunsetting in 2026, inflation, mortality concerns, surviving spouse issues, IRMAA, and the like. Please assume a huge ceteris paribus on everything except the issue below.

I understand the general idea of doing Roth conversions up to the point where my marginal rate today is around what it will be when I'm 72.

I also understand that there is a seesaw effect - the more I convert today, the higher my marginal rate today and the lower it will be when I'm 72, and vice versa.

I'm fairly certain I can assess my marginal rate today at age 52. I also have a spreadsheet that helps me assess my marginal rate when I'm 72.

That spreadsheet obviously has slots for what I Roth convert this year and every year through and past age 72 (up to 85, I think).

So my question:

When I am doing the marginal rate analysis on Roth conversions for the current year N, what should I assume or enter for Roth conversions for the year N+1 through 71?

A. I currently enter what I expect to be my plan for those years, which is roughly up to a FAFSA limit for the next two years, then 400% FPL through Medicare age, then 22% tax bracket for several years, then some IRMAA bracket cliffs, then the 24% tax bracket then the 32% bracket. In other words, I progressively max out monotonically increasing brackets over time. (*)

B. But I could enter $0 for those years.

C. I could also enter whatever Roth conversion number I'm planning on for current year N and just copy paste that number down that column in my spreadsheet.

Option A seems most reasonable because it's the most likely outcome. But it means that my current year Roth conversion doesn't really impact the age 72 marginal rate much, because my age 52 Roth conversion this year is only 1/20th or so of the total conversions before age 72. The current year conversion impact gets diluted by those other 20 conversions.

Option B seems silly.

Option C seems reasonable too, and would magnify the effect of changes in my Roth conversion amount, because changing my age 52 Roth conversion would also change the other 20 conversion numbers as well.

Anyone else thought of this, and how to address it?

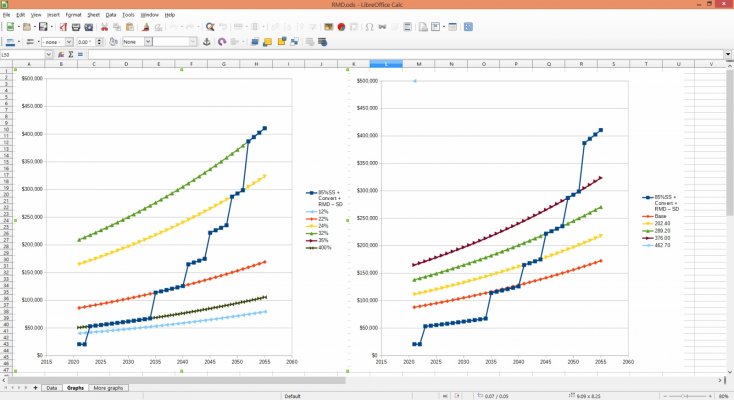

(*) I do this because the parameter I've chosen to maximize is the after tax cash flows with a discount rate of 3%, meaning that I value a spendable dollar when I'm 52 3% more than that same dollar at age 53. If I built my spreadsheet correctly, the way to optimize this seems to be as described above - generally maxxing out brackets until the underlying growth of the traditional IRA shoves me into the next bracket up, and then repeating the process. This is definitely different from just leveling my marginal rate over time. I've attached a screenshot showing my plan where the blue line is my planned withdrawals, marginal rates are the other curves on the left, and IRMAA brackets are the other curves on the right.

52M, single, FIREd for 5 years. Doing the typical Roth conversions between now and age 72 when I plan to start RMDs. I plan to take SS at 70.

For the purposes of this post, please set aside any discussions of tax rates sunsetting in 2026, inflation, mortality concerns, surviving spouse issues, IRMAA, and the like. Please assume a huge ceteris paribus on everything except the issue below.

I understand the general idea of doing Roth conversions up to the point where my marginal rate today is around what it will be when I'm 72.

I also understand that there is a seesaw effect - the more I convert today, the higher my marginal rate today and the lower it will be when I'm 72, and vice versa.

I'm fairly certain I can assess my marginal rate today at age 52. I also have a spreadsheet that helps me assess my marginal rate when I'm 72.

That spreadsheet obviously has slots for what I Roth convert this year and every year through and past age 72 (up to 85, I think).

So my question:

When I am doing the marginal rate analysis on Roth conversions for the current year N, what should I assume or enter for Roth conversions for the year N+1 through 71?

A. I currently enter what I expect to be my plan for those years, which is roughly up to a FAFSA limit for the next two years, then 400% FPL through Medicare age, then 22% tax bracket for several years, then some IRMAA bracket cliffs, then the 24% tax bracket then the 32% bracket. In other words, I progressively max out monotonically increasing brackets over time. (*)

B. But I could enter $0 for those years.

C. I could also enter whatever Roth conversion number I'm planning on for current year N and just copy paste that number down that column in my spreadsheet.

Option A seems most reasonable because it's the most likely outcome. But it means that my current year Roth conversion doesn't really impact the age 72 marginal rate much, because my age 52 Roth conversion this year is only 1/20th or so of the total conversions before age 72. The current year conversion impact gets diluted by those other 20 conversions.

Option B seems silly.

Option C seems reasonable too, and would magnify the effect of changes in my Roth conversion amount, because changing my age 52 Roth conversion would also change the other 20 conversion numbers as well.

Anyone else thought of this, and how to address it?

(*) I do this because the parameter I've chosen to maximize is the after tax cash flows with a discount rate of 3%, meaning that I value a spendable dollar when I'm 52 3% more than that same dollar at age 53. If I built my spreadsheet correctly, the way to optimize this seems to be as described above - generally maxxing out brackets until the underlying growth of the traditional IRA shoves me into the next bracket up, and then repeating the process. This is definitely different from just leveling my marginal rate over time. I've attached a screenshot showing my plan where the blue line is my planned withdrawals, marginal rates are the other curves on the left, and IRMAA brackets are the other curves on the right.