Dtail

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Once again...thanks.

But in determining portfolio performance is simple or compound growth/interest the way to look at it?

Compound.

CAGR = Compound Annual Growth Rate

Once again...thanks.

But in determining portfolio performance is simple or compound growth/interest the way to look at it?

Once again...thanks.

But in determining portfolio performance is simple or compound growth/interest the way to look at it?

It depends on who you are trying to fool. Advisors sometimes use the method that gives a higher number.

After looking at my performance numbers, I do know that my 50-45-05 portfolio is showing the YTD performance of a 50-50 balanced fund, with the expense ratio added back in.I'm just trying to figure out how I'm doing with the truest analysis possible.

I'm just trying to figure out how I'm doing with the truest analysis possible.

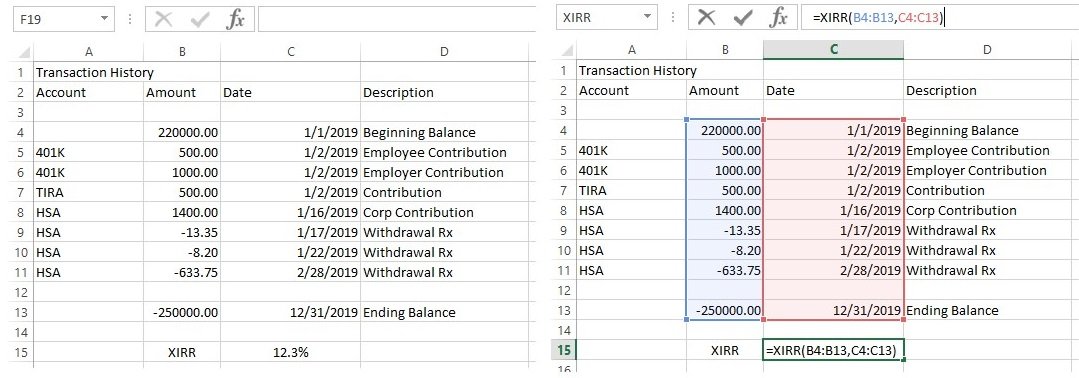

Then you want IRR... compounded. Simple is misleading which is why it is rarely used.

As of yesterday, I'm within 1.44% of my all-time high portfolio balance (which was at the end of January 2018).... and that is after withdrawals since January 2018.

I am over my all time high as well, and patting myself on the back for not starting another Wheee!!! thread about it. ....

OMG! W2R typed the dreaded W-word... we are DOOMED.

Well, but.... but.... !!I have my computer set up to automatically move everything to cash when she mentions the "w" word.OMG! W2R typed the dreaded W-word... we are DOOMED.

Well, but.... but.... !!

Everything sure seems to be coming up roses!

Has anyone studied the delay time between mentioning that word and markets going south?

Has anyone studied the delay time between mentioning that word and markets going south?