Blue Collar Guy

Thinks s/he gets paid by the post

I hung out with all the beautiful people & none of it rubbed off.

they like when i hang out with them, i make them look a bunch better

I hung out with all the beautiful people & none of it rubbed off.

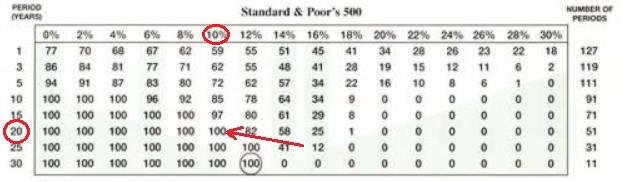

I have no idea (it looks like the DJ index value on a log scale - so probably neither). Midpack posted that chart.And is the chart inflation corrected? Does it include dividends?

....Retirement is fully funded at net return of zero. ...

The only bad question is the one that doesn't it asked. Welcome to the neighborhood. The banking fraud & watching the US Congress peeing on itself as they took orders from Goldman Sachs to pass TARP or watch the world as they know it disappear into oblivion would make anyone think twice about casting their pearls before the swine known as Wall st. But then again you got to ask yourself what are your alternatives.

I may be one of the "gamblers" who prefer to stay in the game. I would ask you the opposite question. "If one has enough resources to fund retirement using a safe return rate, WHY NOT continue with the bulk of one's assets in the stock market?"

If you can continue making above CD and bond rates, and the include the inevitable "big correction" or two or three in your plan, can still cover most of your expenses with non-investible incomes such as SS and pension incomes, can continue living in the same lifestyle you have up till now, why not continue with what brought you to this point? The various calculators all give the opportunity to change one's asset allocation for determining the likely hood of success. I use them.

What if you and your spouse plan to age 90, find a success rate that makes you comfortable, and then happen to live to age 105 or more, what then? You say you are not planning for LTC but what if you happen to need care? even though most don't, many do. Making historically higher returns on my equity investments only opens more security for us over the next 30+ years..... I know 30 years ago I didn't think of some expenses that I have now. Who knows what the next 10, 20, 30 years will bring?

But ours is not a set and forget plan. I can always adjust it any time I need to and probably will. I am continuing to increase my financial knowledge even at the age of 64. Who knows what my plan will look like in 10, or 20 years? So far - so good!

At least that is some of my thinking.

There was one point during the 2008/9 decline that I turned to DW and discussed whether to consider selling. Not selling out, but selling some.

Her comment was a strong no. She is conservative, not interested in finances, but has loads of common sense. Her reply...hell no-not only will they eventually go back up but is now is the time to buy in when when prices are low?

Followed that advice and lucked out. Now I wonder why I was a little apprehensive.

We do bond funds. But short term only. We absolutely stay away from the long term market.

A lot of people follow Mulligan's example. Proof is how happy people are when they "take a Mulligan". !!rimshot!!

From what I see there is a lot of agreement on index funds vs. managed funds . And even more negative agreement on Variable Indexed Partialy Recursive Limited Guarantee Reverse Payment Annuities with 65 pages of detailed legal jargon no buyer understands.

Other than the above two, I think we are all over the map. And sometimes the participants in a thread are using different maps!

It wouldn't be very soft, though. I like Northern TP much better.So I could in theory take my stash and convert it all into $1 bills and use as my permanent toilet tissue supply

There was one point during the 2008/9 decline that I turned to DW and discussed whether to consider selling. Not selling out, but selling some.

Her comment was a strong no. She is conservative, not interested in finances, but has loads of common sense. Her reply...hell no-not only will they eventually go back up but now seems to be the time to buy in when when prices are low.

Followed that advice and lucked out. Now I wonder why I was a little apprehensive.

We do bond funds. But short term only. We absolutely stay away from the long term market.

it was looking ugly, i had already stopped looking at the monthly statements, it was the first time i had heard the term ultra-short mutual funds, i was frozen in fear to be honest, but i remember being an idiot in my late 20's in 1987 and sold . i held firm in 2000 mainly because i had a major death in the family (my sister), and money was the last thing on my mind. i only learned of my paper loss when i went to the tax preparer and he opened a few of the statements and was howling about how much i lost. it was about that time things started to turn around. when the next tsunami comes, ill stop looking at the statements again , and ill watch cartoons on tv and not the financial networks.

The right thing to do in early 2009 was the wrong thing to do in early 1931. As one gets older, this becomes much more important.There was one point during the 2008/9 decline that I turned to DW and discussed whether to consider selling. Not selling out, but selling some.

Her comment was a strong no. She is conservative, not interested in finances, but has loads of common sense. Her reply...hell no-not only will they eventually go back up but now seems to be the time to buy in when when prices are low.

Followed that advice and lucked out. Now I wonder why I was a little apprehensive.

...