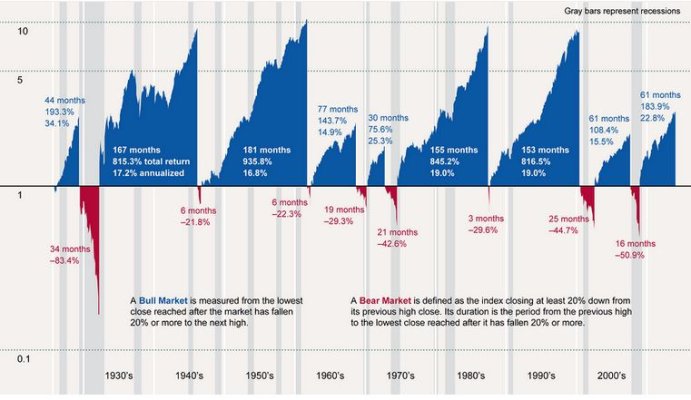

I don't have my spreadsheets in front of me, so this is just going from memory, but here's an estimate of the rough patches I've experienced...

1) Finished 2000, 2001, and 2002 in the red, for each year, although there were spikes during 2000 and 2001 that pushed me to new highs. I think I hit rock bottom around August or September 2002. Anyway, 2003 was a good recovery year, and I was probably made whole again sometime in 2004.

2) In 2006, I lost about 10% in the course of a month, around May-June. It sticks in my mind because, while 10% isn't a huge deal, by that time I had amassed about $300,000, so losing $30K seemed like a lot. Plus, I had other life-drama going on at the time, which only added to it. Anyway, I think it stayed down for a couple months, then started to rebound, but I was recovered later in the year.

3) During the "Great Recession", I lost a little more than half, from peak to trough. For me, that would be October 2007 to November 2008. Most of the loss was in just three short months...Sept/Oct/Nov '08. I had a pretty big bounce back in December, and into early '09, but then the official bottom hit in March '09. From there, it seemed to go nowhere but up, although I do remember a quick ~10-15% correction in early 2010. But, I'd say I was fully recovered sometime in 2010.

4) In 2011, I lost about 15% in just one month, between July and August. I got a little nervous, thinking it was going to be another market crash, but held tight. By this time, I think I had been up to around $650K which was a new record for me, and was down to $560K in one month. I ended up finishing the year with a slight loss of around $1-2K, which barely registers. I'd guess I was fully recovered from that 15% loss sometime in early 2012.

5) Supposedly, there was a 10% market correction since then, but I think it hit and then corrected so fast that it doesn't show up in any sort of data that only shows month-end to month-end. Late 2014, maybe? I do remember 2014 starting off as a good year, but peaking out over the summer and then sort of fizzing. I made about 5.6% that year.

Anyway, that's the biggest pullbacks I can remember, since I started getting serious about investing in late 1998. There may have been other hiccups here and there, but I guess they sorted themselves out pretty quickly, otherwise I'd remember them.