stephenson

Thinks s/he gets paid by the post

- Joined

- Jul 3, 2009

- Messages

- 1,610

Hi All,

Background - married, same age 66 1/2, both in good health, income more than sufficient from military and corporate pensions, dividends, and a few rental properties that are paid for - good shape and very happy we spent 40 years saving and planning for this time. Waiting until 70 for social security. Solid balances at Fidelity and Vanguard where we rolled components of the megacorp 401s, and where our personal IRAs were consolidated.

We purchased a new home in March 2020 - poor timing in some regards, but it’s done and we’re pretty happy in the new house and neighborhood - 15 year, VA at 3.125% with several thousand dollars or credits from the lender that made it a pretty good deal.

We’ve been considering options regarding the loan, including:

(1) refi (local or online)

(2) paying it off (sub options - from A. cash, or B. equity mutual fund sell off)

1. Refi option - local mortgage institutions are quoting 15 year VA refi at 2.25% but with about $8K in closing costs with only minor credit offsets. I know there are many online mortgage lenders, but not sure this would improve either the net rate, or provide credits sufficient to make sense to refi. The difference between 3.125 and 2.25 is about $150 a month = $1800 a year. Figure about four years payback. Unless I can obtain more credits/concessions from lenders, this doesn’t seem to be a great idea.

Question - I know some of you have refi’d online - anyone dealt with circumstances like these? Which of the lenders are sharp and quick with best rates?

2. Paying it off - more complicated as there are more options and sub options

A. pay off from cash

- uses about 70% of our buffer, and we would immediately start trying to build cash back up over time

B. pay off by selling mutual funds in which we invested over the years.

- Anyone who knows of the “Wayback Machine” will also remember the monthly Money magazine with pages of mutual fund ratings and annual growth data")

- Over many year we constantly reviewed mutual funds to see which were doing well over various periods of time, then tried to pick based on a non-statistical model (ie - kinda swagged it) to determine what to invest in THAT YEAR - I can hear the tittering about this approach, but we did save and invest - and, while we have liquidated a bit over the years as we needed cash for home medications, most of these fund holdings have simply grown. We did this across taxable money we had saved each year as well as IRAs. We were pretty ignorant, so the overlap is embarrassing, but it was money not spent on new cars, et al.

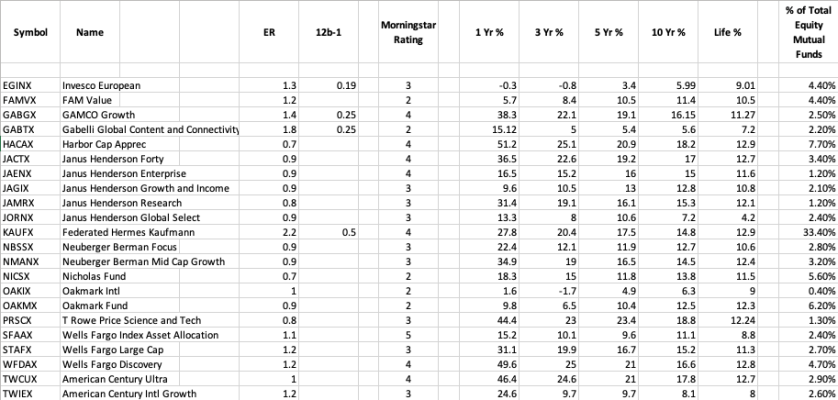

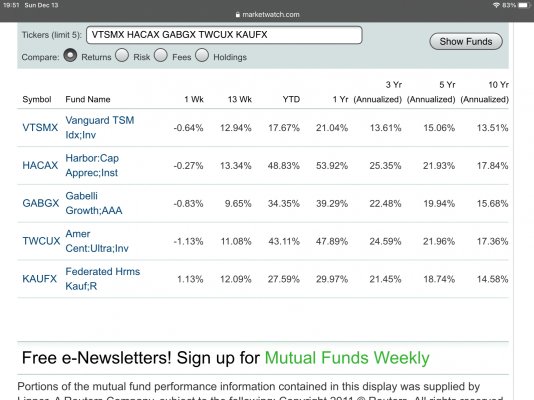

- IF we chose this option, I would continue my review of each of these 22 holdings (see attached) to determine basis and what capital gains we have paid over the years to determine how much taxes will bite when we sell.

Question - I would, in general want to sell equity funds that are: low performing, high cost, and on which we have paid capital gains over the years to minimize tax hit, right?

So, attached is a list of the funds we still have - I did NOT include individual stocks, or ETFs in the total - and, to be clear, all these are taxable status. Would appreciate pointed or broad thoughts on what you would do in like circumstances - I know there may not be a perfect or even clear answer. For instance what is it worth to NOT have a mortgage loan?

Tried to make this logical, but it still sounds confused ... sorry.

Thanks in advance!!

Background - married, same age 66 1/2, both in good health, income more than sufficient from military and corporate pensions, dividends, and a few rental properties that are paid for - good shape and very happy we spent 40 years saving and planning for this time. Waiting until 70 for social security. Solid balances at Fidelity and Vanguard where we rolled components of the megacorp 401s, and where our personal IRAs were consolidated.

We purchased a new home in March 2020 - poor timing in some regards, but it’s done and we’re pretty happy in the new house and neighborhood - 15 year, VA at 3.125% with several thousand dollars or credits from the lender that made it a pretty good deal.

We’ve been considering options regarding the loan, including:

(1) refi (local or online)

(2) paying it off (sub options - from A. cash, or B. equity mutual fund sell off)

1. Refi option - local mortgage institutions are quoting 15 year VA refi at 2.25% but with about $8K in closing costs with only minor credit offsets. I know there are many online mortgage lenders, but not sure this would improve either the net rate, or provide credits sufficient to make sense to refi. The difference between 3.125 and 2.25 is about $150 a month = $1800 a year. Figure about four years payback. Unless I can obtain more credits/concessions from lenders, this doesn’t seem to be a great idea.

Question - I know some of you have refi’d online - anyone dealt with circumstances like these? Which of the lenders are sharp and quick with best rates?

2. Paying it off - more complicated as there are more options and sub options

A. pay off from cash

- uses about 70% of our buffer, and we would immediately start trying to build cash back up over time

B. pay off by selling mutual funds in which we invested over the years.

- Anyone who knows of the “Wayback Machine” will also remember the monthly Money magazine with pages of mutual fund ratings and annual growth data

- Over many year we constantly reviewed mutual funds to see which were doing well over various periods of time, then tried to pick based on a non-statistical model (ie - kinda swagged it) to determine what to invest in THAT YEAR - I can hear the tittering about this approach, but we did save and invest - and, while we have liquidated a bit over the years as we needed cash for home medications, most of these fund holdings have simply grown. We did this across taxable money we had saved each year as well as IRAs. We were pretty ignorant, so the overlap is embarrassing, but it was money not spent on new cars, et al.

- IF we chose this option, I would continue my review of each of these 22 holdings (see attached) to determine basis and what capital gains we have paid over the years to determine how much taxes will bite when we sell.

Question - I would, in general want to sell equity funds that are: low performing, high cost, and on which we have paid capital gains over the years to minimize tax hit, right?

So, attached is a list of the funds we still have - I did NOT include individual stocks, or ETFs in the total - and, to be clear, all these are taxable status. Would appreciate pointed or broad thoughts on what you would do in like circumstances - I know there may not be a perfect or even clear answer. For instance what is it worth to NOT have a mortgage loan?

Tried to make this logical, but it still sounds confused ... sorry.

Thanks in advance!!