Running_Man

Thinks s/he gets paid by the post

- Joined

- Sep 25, 2006

- Messages

- 2,844

TLT has outperformed BRK since Oct 2008

Yes, one should be sure to include dividends when comparing stocks.

According to Morningstar, a $10K invested 5 years ago would grow to $17,130 in VFINX (Vanguard flagship S&P MF), and $17,253 in BRK. So they run neck-to-neck the last 5 years.

The Total Return is the rate of return representing the price appreciation of a stock with cash dividends reinvested on the ex-date for the most recent 1, 3 and 5 fiscal years.

This growth of $10,000 graph represents the growth of a hypothetical investment of $10,000. It assumes reinvestment of dividends on ex-date.

That chart doesn't look like it includes dividends. And that's a huge illusory advantage for non-dividend paying companies like Berkshire.

Total returns for Vanguard's 500 Index are 73% over the last five years instead of about 50% shown in the chart. BRK looks like it's up about 60% over 5 years, so trailing the S&P 500 total return.

I posted this on another thread, but active fund managers are handicapped by the very people who invest in them. I see it all the time at work. When the market goes down, people panic and shift out of stocks. When the market skyrockets, they go all in. They're basically forcing the managers to sell low and buy high.

Look how little the fund dropped during the recession of 2002-2003 and the Great Recession of 2008-2009, compared to the S&P. However, it has not grown as strong in the last few years.

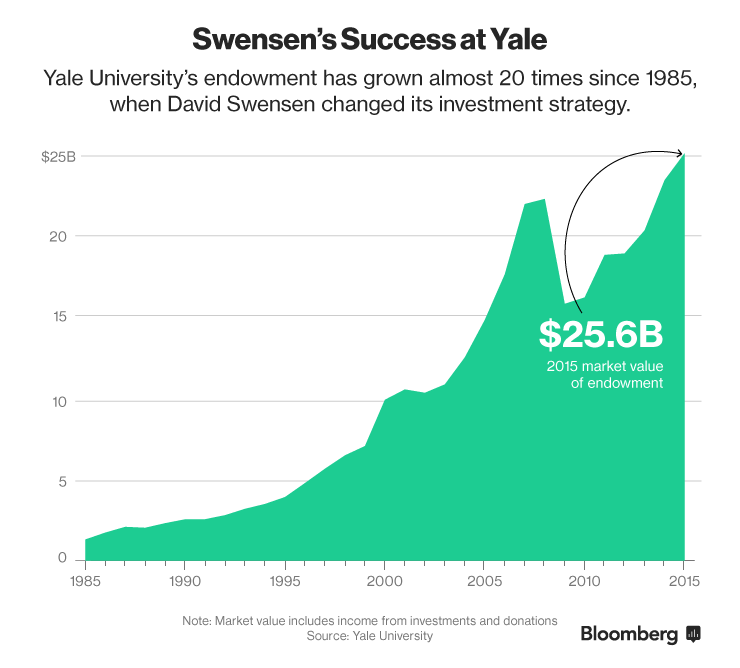

Is the data behind the graph even meaningful? I thought Yale had a huge portion of their endowment in illiquid assets that can't really be marked to market like a traditional stock/bond portfolio.

I used to have Swenson's book but I never read it. Maybe I would know the answer if I had.

Sent from my iPad using Early Retirement Forum

But then that begs the point: I have had two opportunities since 2000 to load up on cheap marked down stocks, and why am I not having a lot more money?

It is indeed difficult to go against the crowd, and when they panic you think perhaps they know something you don't.

If you are trying to beat the 'index', whatever that is, just buy the index. I buy S&P 500 shares through IVV at Fidelity. No cost to get in, or out.

I am near guaranteed to match the index. My dividends are ~2.25%, always reinvested. There are never any capital gains, only the qualified dividends. I do not have to re-balance and pay any capital gains.

")

So basically you always beat the index by 2.25% - not bad!

So basically you always beat the index by 2.25% - not bad!

In 2016, it should be easy for anyone to beat the S&P index, even fund managers.

The S&P index went down so fast, that any amount purchased in the first two months will beat the index if it winds up positive, or flat. That's a 66.67% chance of beating it.

By some measures, active managers got what they’ve been hoping for in 2016, at least on paper: correlated moves among equities unwound to the lowest levels since 2012 and breadth, or the number of stock advancing, came roaring back. Both are viewed favorably by anyone trying to beat an index.

Those gifts proved illusory as fund managers trailed benchmarks by one of the highest rates in two decades. The reason: stocks they avoided went up, and the ones they owned went down.

The above is an argument from the EMH proponents, more than from the indexers. The most ardent followers of EMH will say that there's really never any mania. When a tulip bulb is priced the same as a farm, the market says it should be so, and the market is always right.I'd add that massive market sell-offs are not always irrational or an indication of panic. The 2008/2009 drop was completely justified based on the distribution of potential outcomes. Buying at the bottom required more than just a contrary spirit or a calm assessment of the fundamentals, it required an act of faith.

The above is an argument from the EMH proponents, more than from the indexers.

Eh, indexing is the PC thing to safely say nowadays.

Plus, my index beats your index. And then, my rebalancing method is superior to yours.

Has anyone seen statistics on how individuals who own a variety index funds as opposed to only owning the S&P 500 do? How to folks who actively diversify their portfolios with a variety of index funds do vs. folks who stick to only owning the S&P 500 or the TSM?

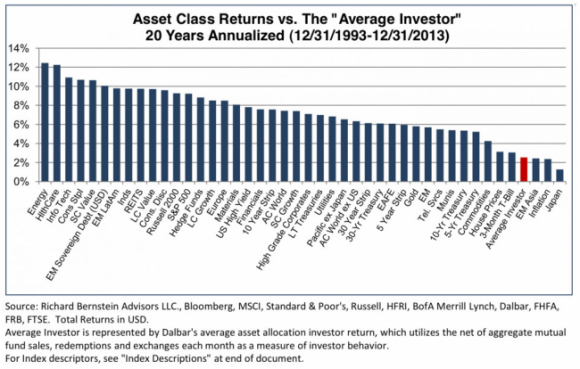

But we also know that most individual investors are horrible investors. In fact, a recent study by Richard Bernstein showed that the average investor generated a measly 2.1% return over the period from 1993-2013:

The discussion in this thread seems to equate "indexes" with "broad indexes." For example, many are comparing the performance of some actively managed MF with the S&P 500 index. Seems like a good idea.

But what about the folks who own 100% index funds but their portfolio includes a variety of more focused index funds? You know...... dom small cap value, various commodity indexes, regional international indexes, market segment indexes (I'm in the midst of getting burned owning an energy segment index etf right now!) and on and on.

You can be a 100% indexer and be totally out of whack with the S&P 500 index, or any of the many domestic large cap indexes and their corresponding index funds, right? Is anyone who owns anything other than SPY, VTI (or equivalent) doomed to under perform due to not just buying and holding the S&P 500 or the TSM?