This was an interesting topic, and I learned a good bit from the back and forth.

ERD50, is your portfolio (positions, not specific $ amounts) posted somewhere? I'd be curious as to where you are invested since you have obviously given this significant thought.

I give it less and less thought as time goes on. That's kind of my point. The market does what it will, sectors picks will rise and fall. No one knows. I don't see any point in over-thinking it. But I do kind of enjoy the discussions, you never know when something might trigger a thought to act on.

Off the top of my head (and I'll check in a minute to see how close my estimates are), I'm about 75/25 ~ 70/30 AA. A portion of the 75 is INTL, a European index fund and some in a SE Asia index fund, maybe 10% overall? Again, no big thought process on this, those are some individual IRAs, and that were the funds I chose years ago. So the percentage just 'happened', no big plan. Will probably review that when I do some consolidation in a few years after I'm done with ROTH conversions.

I'd put all my equities in VTI or other broad index if I was staring from scratch, but since I had used SPY for that for a while, I've broadened that with an index ETF with more small cap exposure. And some other variations are due to taxes, not investment per say. I hold some BRK and small cap index in my taxable account, because I don't want divs, in order to provide headroom for 0% LTCG harvesting, and/or ROTH conversions. A couple small holdings leftover from some previous ideas that I don't think are worth the minuscule effort to sell. For my ~ 25% fixed income, it's BND.

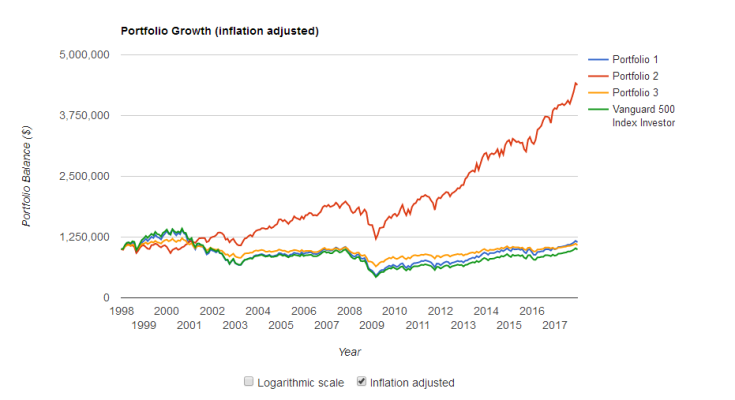

And I don't get hung up any rebalancing rules. It helps sometimes and hurts others, so I just stay lazy and do nothing, figuring that will average out. If you look at the success versus AA in FIRECalc, it's pretty similar results on anything from ~ 50/50 to 90/10. Ity's just not that sensitive, so I don't let it drive me. It's a real yawn. But looking at the 'Beat Boho" contest, you'll see that 'napper' nunnun is doing very well with the buy, hold and forget it approach.

OK, spreadsheet was updated end of OCT2017 - I was pretty close right in the middle of those ranges, with ~ 11% INTL, about 1% in cash, just for cash flow purposes.

Are you still awake?

More concisely, and probably more importantly- if someone was looking for a plan, I'd say to consider to just do whatever AA from 50/50 to 90/10 you decide on, and just go VTI/BND and call it a day. Throw in 10% INTL if you really want, throw in 5% REIT if you really want. Then forget about it. Let's go have a beer.

All the other tweaking might help, might hurt, who knows so why bother?

-ERD50